Zenith believes private markets are in their late cycle stage, pointing to the proliferation of product as evidence.

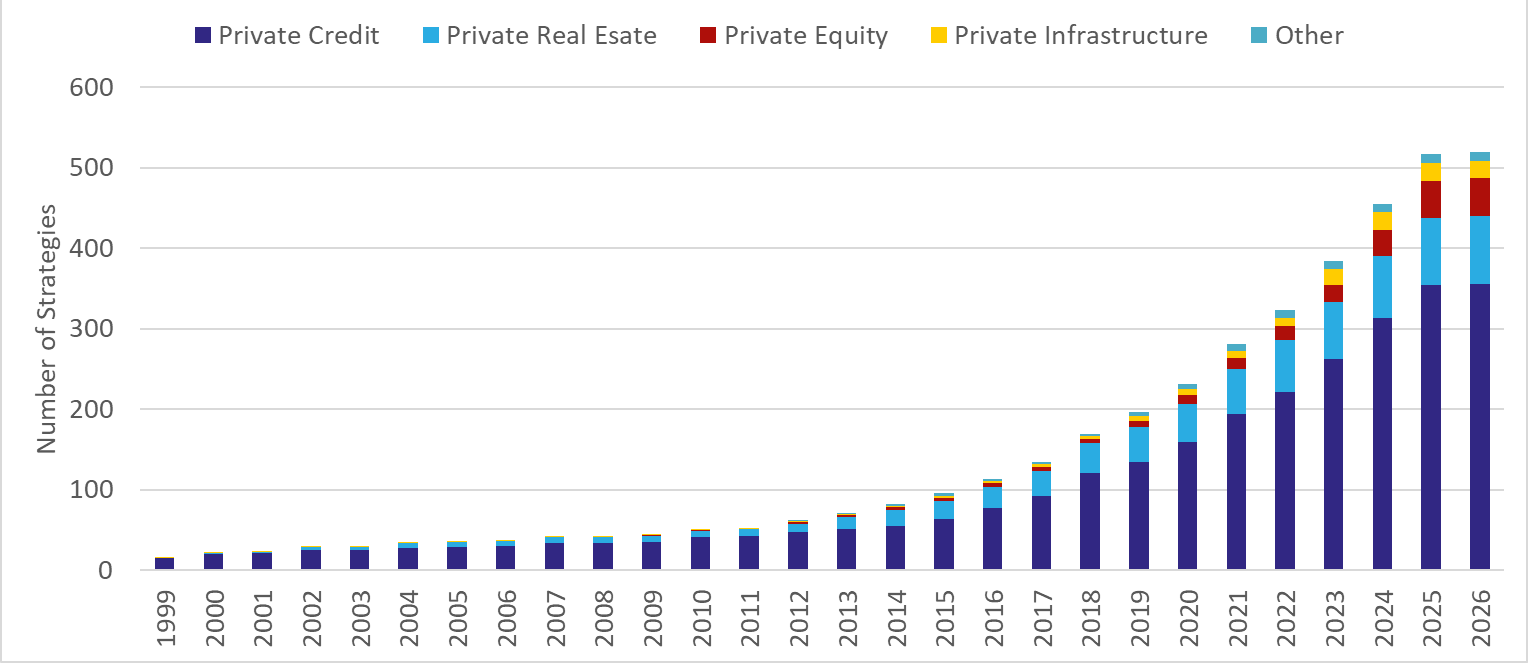

The researcher’s head of responsible investment and real assets Dugald Higgins told a media roundtable in Sydney there are 500 private markets strategies now available to investors.

“What are we seeing? Product proliferation is always, as we all know here, a late-cycle thing,” Higgins said.

Higgins said it is difficult to tell how much money is in those funds, but he estimated “north” of $100 billion.

“There’s definitely about $25 billion in real estate, probably another $60 billion to $80 billion in credit; infrastructure and private equity are much smaller,” Higgins said.

Number of Australian domiciled evergreen private market strategies

Higgins said to expect fee compression to hit private market managers, which are currently the “last bastion” of high fee products.

“They don’t have the pressures of public markets [with] index-based products squeezing their market share,” Higgins said.

“We do see a lot of fee behaviour, particularly around performance fees, that is perhaps a bit egregious. They will have a fee hurdle set epicly lower than their performance target, like saying you have a performance target of 10 [per cent] and a fee hurdle of 5 [per cent] and I think that’s rubbish, personally.”

Higgins said when markets are good investors tend to be more forgiving of high fees, but it’s when markets turn sour that pushback happens.

“We’ll probably start see pressure, if not on base fees but how performance fees are shared,” Higgins said.

Public scrutiny on private markets

ASIC is currently reviewing adviser distribution of private credit funds following a discussion paper it released a year ago into private markets and a subsequent check of some of the products on the market.

The regulator placed temporary stop orders on a few private credit products, including from La Trobe Financial, over concerns the target market determinations suggested an “inappropriate level of portfolio allocation”, according to the regulator.

Numerous private credit funds in the United States and Europe have started restricting or denying redemptions, although the loan concerns there centre on software companies as opposed to real estate.

In late February, Blue Owl began freezing redemptions for one of its top debt funds, while Cliffwater has also started freezing redemptions.

Blue Owl global head of institutional capital James Clarke appeared on the Top1000Funds Fiduciary Investors Series podcast, presented by Professional Planner’s global pension fund focused sister publication, earlier this month to assuage concerns about the asset class.

“What was really interesting in my mind is it’s gone from the golden age of private credit to an insect I really don’t want to talk about anymore by Jamie Dimon and it’s just like that nomenclature all of a sudden pulled the trap door on the asset class,” Clarke said, referring to now infamous comments by the JPMorgan CEO.

Dimon compared the sector to cockroaches in that there is often more than one around, an allusion to the collapses of First Brands and Tricolor with the implication that more will occur.

“Here’s what I can tell you: over that period, the asset class has consistently met its objectives and mitigated downside risk,” Clarke said.

Amusing/irritating/frustrating

Higgins said the current stage of the cycle was “simultaneously amusing, irritating or frustrating… depending on how long you’ve been around for”.

“I’ve been around a long time so I’m finding aspects of all of those,” he said.

“We find ourselves at an interesting time where globally, the advent of more non-institutional access to private markets has exploded, but people seem to be very unwilling to understand that in Australia we’ve had them for nearly 40 years.”

Higgins said he “I often kind of roll my eyes” at some of the “panic mongering” thrown around on social media in the United States and Europe about private credit.

“Firstly, what did you think was going to happen and [secondly], this is a normal state of affairs,” Higgins said.

“We’ve had these things in Australia here for a very long time now, it doesn’t mean that new waves of investors don’t come in and find themselves marooned but this is the way it always works.”

Higgins said there isn’t an issue with retail clients holding private market products, and it is in fact a strong portfolio diversifier, but the caveats that come with the products need to be acknowledged.

“Because that’s one of the biggest things that tends to drive the real backlash on these things,” he said.

“It’s because, naturally, people are more used to dealing with a liquid asset that when that market starts to sell off or they want to rotate, they want to be able to do it at will. If that is the attitude you want to operate under these are not the assets for you. If you want liquidity on your terms, not somebody else’s terms, well you should go and buy equities.”

Higgins said the criticism that inflows shouldn’t be used for redemptions was also unfair.

“Even the regulators didn’t really understand this, they were thinking about saying that funds shouldn’t be allowed to use inflows to meet redemptions,” Higgins said.

“That’s the whole managed funds industry even in liquid markets. You have to be willing to accept inflows are one of the very big pots that drive the availability of liquidity.”