Produced in partnership with Betashares.

The US dollar Index fell another 7.0 per cent in the second quarter of 2025 taking its cycle drawdown to 11.9 per cent – reaching the lowest level in three years. This marks the worst first half of a calendar year since the 1970s for the dollar.

Further weakness came despite the resurgence in US stocks singling out the dollar’s decline from a broader “sell-US trade”. A weaker US dollar is an explicit goal of the Trump administration. And while there is no direct policy to force the dollar weaker, a combination of trade policy and expectations of a US growth slowdown are doing the job.

Currently, the scope for continued USD weakness looks likely. Positioning in the greenback remains elevated, and on most fundamental currency metrics like purchasing power parity the USD is still considered overvalued.

The AUD has also lagged against other currencies in its appreciation against the USD and has room to catch up.

These developments could catalyse a dramatic mean reversion in the Aussie dollar which remains 13 per cent below its long-term average of US$0.75 ($1.16) at time of writing. This would have significant impacts on Australian investor returns at a time they are more exposed to the USD than ever.

Source: Betashares, Bloomberg. As at 30 June 2025.

The case for tactical currency hedging

Most global equities and global equity ETFs held by Australian investors are unhedged. In addition, self-directed investors tend to hedge significantly less than professionally managed model portfolios or superannuation funds, where hedge ratios are typically closer to 50 per cent (as reflected in APRA’s Simple Reference Portfolio benchmark).

This “under hedging” is occurring despite US equities, and by extension the US dollar, now comprising over 70 per cent of developed market benchmarks such as the MSCI World Index, still around the highest levels on record.

With US equities comprising most of the global benchmark, movements in the AUD/USD exchange rate have a major impact on unhedged returns. Over the past decade, being unhedged has provided a tailwind, but this dynamic can reverse – and there are clear historical precedents for extended AUD strength and relatively poor unhedged US and global equity returns.

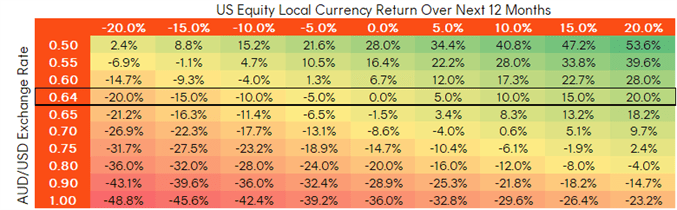

Since the Australian dollar was floated in 1983, the AUD/USD has averaged around $0.75, and even in the past decade has touched $0.80 on multiple occasions. The table below illustrates different exchange rate and US equity local return scenarios, showing their impact on unhedged AUD returns. For instance, if the AUD were to return to US$0.80, it would reduce the local return on US equities by approximately 20 per cent.

Projected AUD unhedged returns for US equities under various local market return and currency scenarios.

Source: Bloomberg. As at 30 April 2025. Assumes starting point of AUD/USD = 0.64

Considering a long-term approach to currency hedging

For Australian investors, leaving a portion of your global equities exposure unhedged can lower portfolio volatility and drawdowns in periods of strong equity market drawdowns.

This is because the AUD is seen as a “risk on” currency, whereas the US dollar is often regarded as “safe haven” currency which historically has tended to appreciate in periods of market sell-offs.

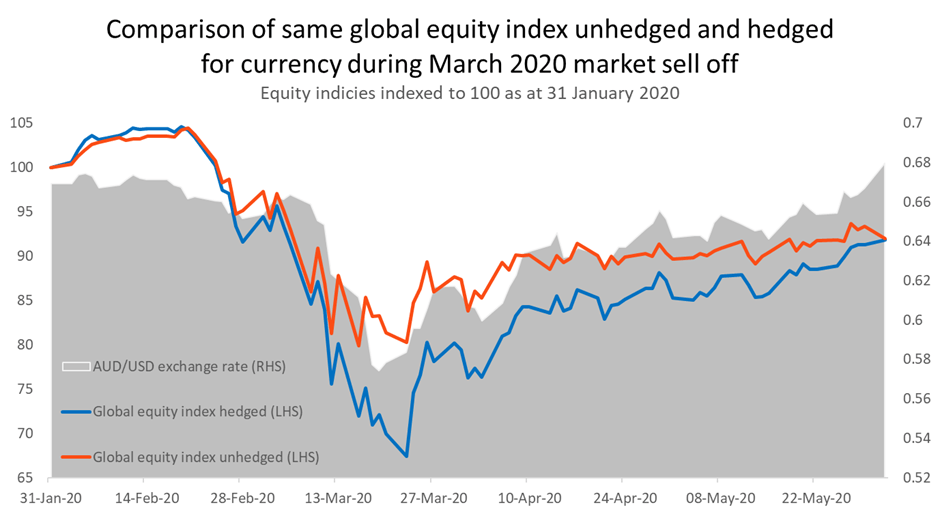

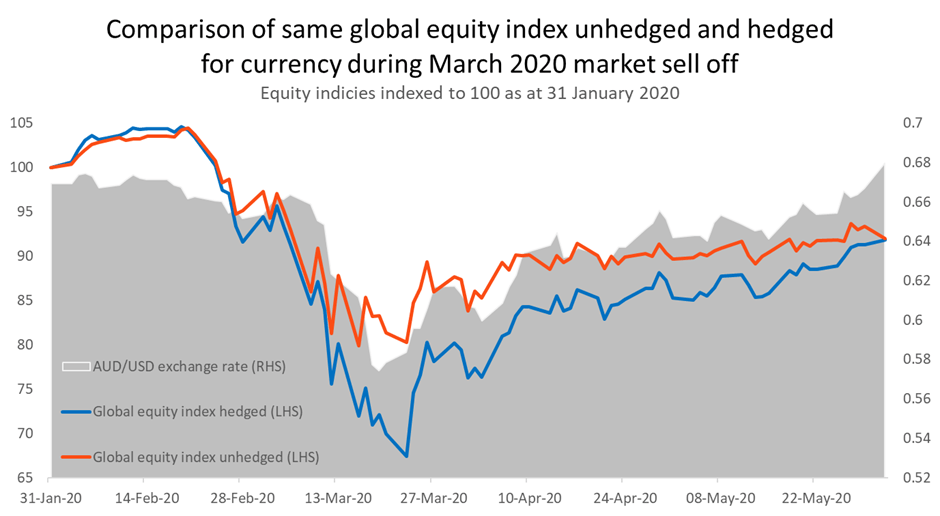

We see evidence of this in the chart below. During the Covid-19 pandemic market sell off in March 2020, an unhedged global equities index experienced a smaller drawdown (-20 per cent) compared to a hedged index (-33 per cent).

Source: Bloomberg. 31 January 2020 to 1 June 2020. Global equity index hedged represented by Solactive GBS Developed Markets ex Australia Large & Mid Cap Index AUD Hedged. Global equity index unhedged represented by Solactive GBS Developed Markets ex Australia Large & Mid Cap Index. You cannot invest directly in an index. Past performance is not an indication of future performance of any index or ETF.

Trend can be your friend, or foe

If remaining unhedged or having a lower level of currency hedging is better from a drawdown and risk standpoint, what about portfolio returns?

Over the 35-year return period that we have analysed, the Australian dollar started and finished around US$0.70, and as a result the historic portfolio returns at all levels of currency hedging were approximately the same.

However, within this multi decade period, we witnessed a number of 5-to-10-year periods where the AUD/USD trended strongly, both higher and lower.

For example, the AUD rallied significantly from US$0.50 in December 2001 to nearly US$0.90 in December 2007. Over that time period, the S&P 500 Index returned 42 per cent in USD terms, but if an Australian investor held the S&P 500 Index unhedged, their return would have been -17 per cent in AUD terms.

This illustrates the potential ‘destruction’ of investor capital that currency can wreak – a point often forgotten, given the last decade has witnessed twin tailwinds of strong global equity performance and a weakening AUD.

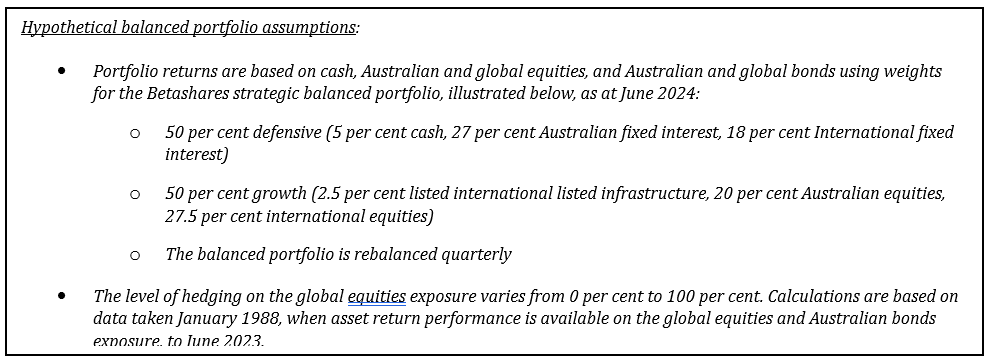

We considered the return implications of currency hedging over different five year-time frames going back to 1988, where AUD appreciation or depreciation could have had a significant impact on overall outcomes for a hypothetical diversified portfolio.

Historically, we found that being completely unhedged or 100 per cent hedged increased the return outcome uncertainty. Where the level of currency hedging employed was between 30 per cent – 80 per cent, there was far lower variability between the minimum and maximum five-year return outcomes.

So, to hedge or not to hedge?

Investors with a view that the AUD is set to appreciate as the USD undergoes a fundamental challenge to its decade long dominance can choose to express a tactical view by increasing the hedged portion of their global equities portfolio.

For those not wishing to express a tactical view on currency, our analysis suggests an approach of currency hedging a portion of a global equities allocation could reduce the variability of long-term return outcomes making hedging still worthwhile.

Review your current hedge ratio and ask: are you prepared for an AUD rebound?

Tom Wickenden works as an investment strategist in Betashares investment strategy and research team.