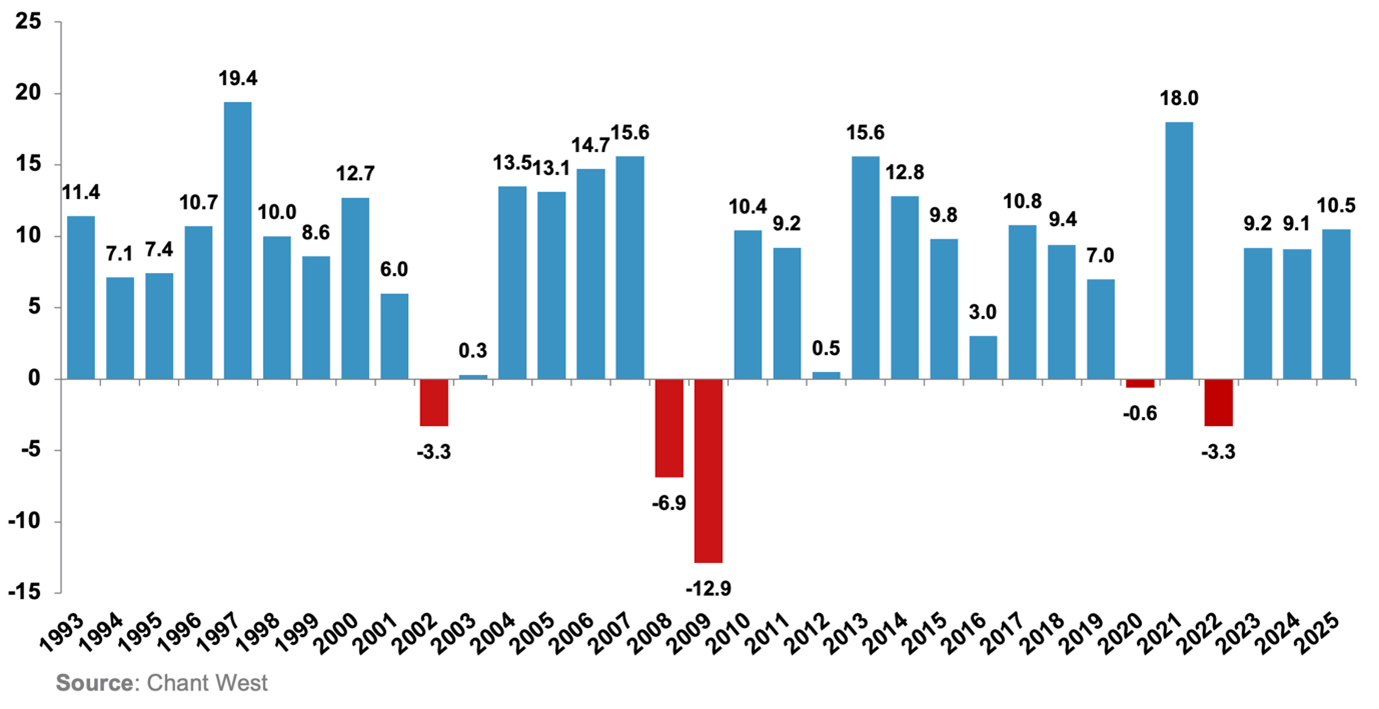

In the past 33 financial years there have been only five when the median growth super fund produced a negative return. Data produced by research firm Chant West shows that over the more-than-three-decade period, the median fund return has exceeded a long-term investment objective of CPI +3.5 per cent.

Those long-term returns have been well supported in the 12 months to 30 June 2025, with the median growth fund – which Chant West defines as funds invested 61 to 80 per cent in growth assets – returning 10.5 per cent.

The researcher notes that typically “a growth fund would aim to post no more than one negative return in five years on average”.

“This objective would translate to no more than six negative years over the 33 financial years shown. As it turns out, there have only been five negative years, so the risk objective has been met as well as the performance objective.”

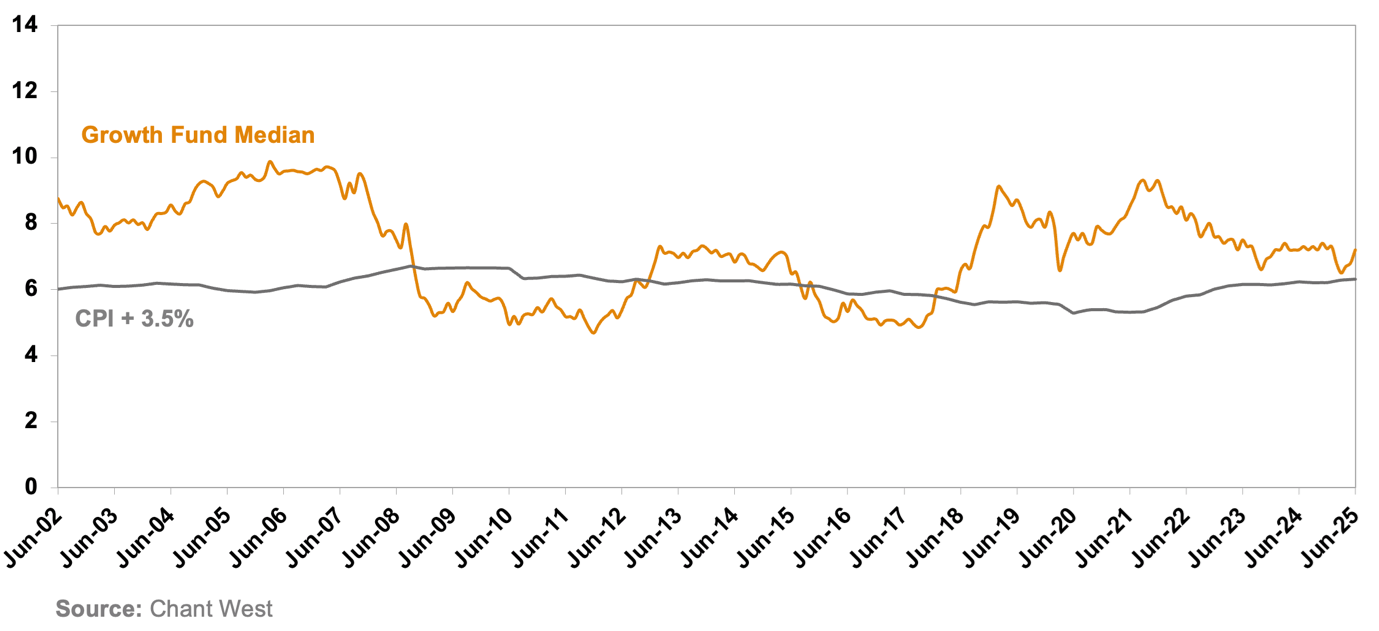

This series of short-term returns has added up to a strong run over three decades to produce a median growth fund return of 7.2 per cent ay year over 10 years, and 8 per cent a year over 15 years – all, as the Chant West data shows, while producing negative returns in only five financial years.

Growth funds financial-year returns (per cent)

Growth funds rolling 10-year performance (per cent, per annum)

Growth funds rolling 10-year performance (per cent, per annum)

While short-term returns are clearly influenced by short-term market conditions and tactical moves by investors, a fund’s strategic asset allocation remains the primary determinant of long-term performance.

While short-term returns are clearly influenced by short-term market conditions and tactical moves by investors, a fund’s strategic asset allocation remains the primary determinant of long-term performance.

Chant West senior investment researcher Mano Mohankumar tells Professional Planner that for growth funds this has primarily meant an exposure to listed shares averaging about 55 per cent.

But he adds that strong equities performance has been supported by diversification and “increasing exposure to private markets”.

He says over the past 10 years diversification has been shown to “capture a big chunk of the uptick when share markets do well, but at the same time, during periods of market volatility, it cushions the blow”.

“Focusing on the growth category…55 per cent on average, is allocated to listed shares, but that does mean that there’s a meaningful 45 per cent that’s allocated to other asset classes – that’s across the spectrum of your traditional defensives and alternative and unlisted assets,” Mohankumar says.

Mohankumar says private markets have become central to how funds generate returns and manage member outcomes.

“It’s important to also remember that the private markets portfolios have played a critical role in super fund portfolios for a very long time, providing the illiquidity premium over the long term but also contributing to that smoother return journey for members over time.”

Mohankumar says that over the past decade allocations to unlisted infrastructure, in particular, have increased across all funds.

“Private equity has gone up a little bit,” he says. “That increase in unlisted assets is not just not-for-profit funds. Retail funds have also increased their exposures to unlisted over time as well.”

Best performers shine through

Andrew Lill, interim chief investment officer at legalsuper, says the fund has maintained exposure to private markets, unlisted exposures and cash and fixed income through the 12 months.

“We haven’t, for instance, just thrown our conviction on the global equity market that performed the best,” he says.

“And that really goes also to the evidence of the 10-year numbers, because over the 10-year period there has been a lot of different factors at play, and we have maintained a relatively long-term strategic approach to both unlisted and listed markets.”

Lill says it’s still very much the case that strategic asset allocation remains the primary determinant of a fund’s long-term performance.

“The first five years of the previous decade was really very good for private markets, unlisted markets; and so far, this decade has been very good for more listed markets,” he says.

“If you were, for instance, moving from listed to unlisted in the 2020s you were going the wrong way, but by keeping the right mix of listed and unlisted through that, through the last decade into this decade, you’ve tended to deliver.”

Mohankumar says the very long-term returns from funds is impressive in light of the challenges that they’ve faced over the period, but even financial events such the Covid-19 induced market crash or the Global Financial Crisis only had temporary impacts, and disciplined investing and a long-term perspective usually saw funds bounce back.

Funds also faced operational challenges, such as the government’s early access scheme in 2020.

“Super funds do rigorous liquidity testing, as you know…but certainly, at the time, that was something new, where Australians who needed their money could actually access it,” he says.

NGS Super chief investment officer Ben Squires says international equities were a standout performer, but the fund’s results were the product of broader balance across asset classes.

“International equities primarily performed strongly [and] from our perspective, it was the second highest performing asset class across the sectors we invest in,” Squires says.

“Our fixed income portfolios, our infrastructure across the spectrum, they all landed in the sweet spot of what we expect over the long term to deliver.”

Squires also points to NGS’s distinctive exposure to commodities as a factor, and as a significant differentiator between it and most other funds.

“The top performing asset class over 2025 was commodities, precious metals,” he says.

“And we’re probably one of the only funds in the market, other than the Future Fund, I believe, that for multiple years has had an exposure in that space. That was quite advantageous for us this year and also last year.”

Lill says the fund’s 12-month return was the result of targeted active management decisions rather than a blanket increase in portfolio risk.

“Over 12 months, in common with many funds, we’ve taken some decisions to reduce active risk in certain parts of the portfolio and but at the same time, maintained high conviction active management in certain chosen areas,” he says.

These included “benchmark-unaware, mid-cap, global-tech exposure; Australian small -cap; and a combination of unlisted and listed infrastructure”.

“I’d also say that active management of global fixed income through the very turbulent March and April period yielded outsize alpha,” he says.

“We haven’t upped the risk of the portfolio. I would say that over the 12-month period, through a combination of skill and luck, our positions for active management have generally been positive, and we’ve avoided underperformance, effectively, because we’ve reduced risk in some areas, and so in in actual fact, total portfolio the overall risk is lower, but where we’ve maintained the risk, it’s yielded good 12-month returns.”

Managing risk

Squires says what sets NGS apart is strong risk-adjusted returns.

“I think when we finally see all the stats coming out, we’ll have the highest Sharpe ratio of any of the funds,” he says. “We take far less risk to generate excess returns.”

Squires notes that the fund “thinks about the Sharpe ratio” and “information ratio” in portfolio construction.

“We’re trying to kind of optimise our portfolio to get rewarded for the risk that we’re taking,” he says.

“You can observe that there’s been a number of funds that have had long-term strong results, [and] you have to assign some of that not just to taking excess risk – because you can just have a high beta portfolio and you would have done well – but also you have to assign some of that to skill. That’s an important thing to recognise.”

Squires says identifying skill over luck requires more than just a cursory perusal of raw performance numbers.

“What I would look for is…not only the return, but the level of risk that’s been taken to generate that return,” he says, and skill is evident in “how much risk have you borne” and how a fund is protected during downturns.

Squires says NGS also approaches equities differently from peers.

“We restructured our portfolio back in late 2022 to immunise it from the more active variances you can get from a more active strategy,” he says.

“We reduced the degree of tracking error just to stabilise that part, and then allocated that active risk elsewhere, where we thought we could harvest more premium.”

Lill likewise stresses the importance of knowing where to take risk and where not to.

“A couple of areas where you should be fairly strategically fixed is agree and understand where you can best add value,” he says.

“That might mean that you think carefully about your size as a fund. Obviously, we are a relatively smaller fund by current standards. We have not gone down the path of internalisation. We have maintained an approach to utilising external managers, so we haven’t deviated from that.

“We’ve been willing to be patient in the manager strategies and areas that we feel are truly unique advantages for legalsuper. That’s a long-winded way of saying don’t do what everyone else is doing; but don’t hold on to things that you really don’t have any advantage in.”