Produced in partnership with Betashares.

As “Liberation Day” rocked global share markets, gold has continued to offer investors a safe haven in a time of heightened uncertainty. The magnitude of the tariffs announced and a somewhat shambolic approach to determining reciprocal tariff rates has done little to clear the air.

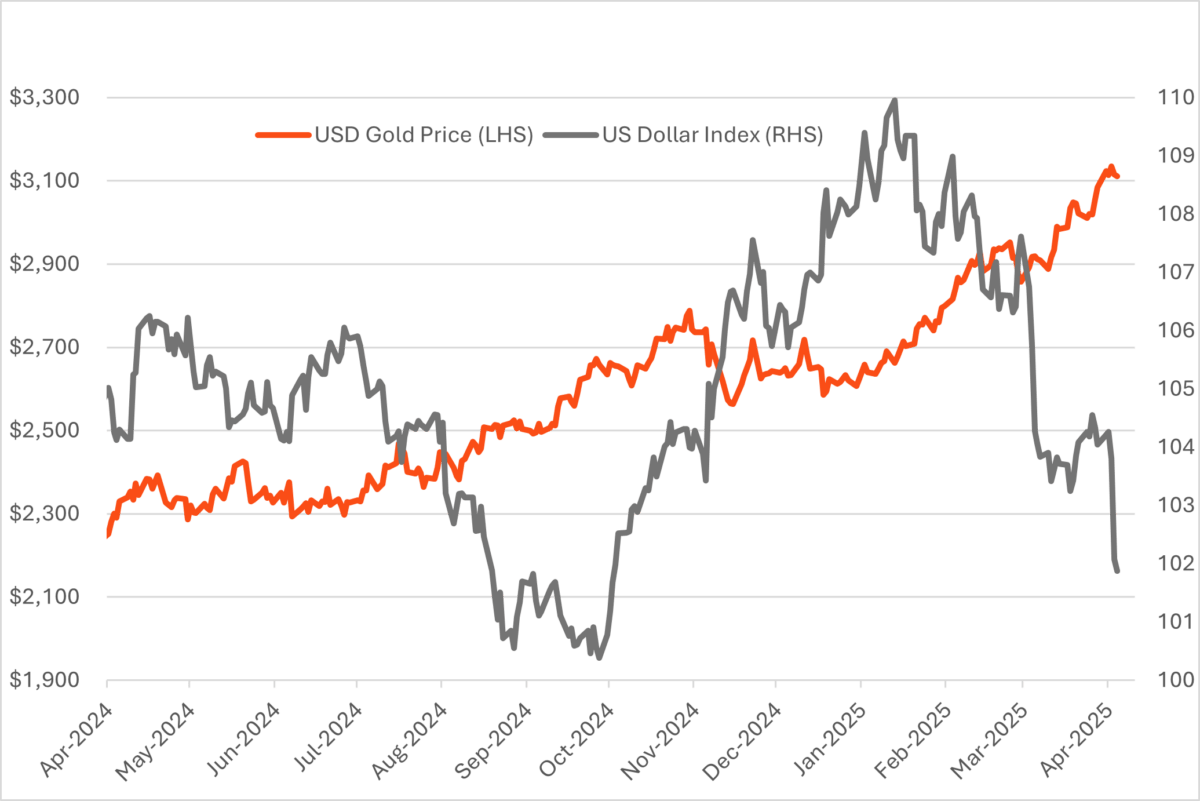

Risk sentiment ebbed and flowed since Trump was re-elected in November last year, but gold has been one of the best performing assets throughout, breaking through US$3000 ($5040) an ounce last month. As pressure mounts on the US exceptionalism narrative, and by extension the US Dollar, I don’t see a reason why gold can’t continue to grind higher from here.

Gold has continued its strong run in 2025 as the US Dollar has fallen

Source: Bloomberg, as at 4 April 2025. The US Dollar Index measures the performance of the dollar against a basket of other currencies. Past performance is not an indicator of future performance.

Gold is enjoying strong structural and cyclical demand, but it also provides investors holding equities with a very valuable hedge against escalating trade wars, geopolitical conflict and fears relating to US government debt and central bank independence.

Central bank buying

As geopolitical tensions have escalated over the last few years central banks have gone on a gold buying spree.

As a reliable store of value, gold is highly attractive for central banks seeking to diversify their reserves beyond foreign currencies like the USD and US Treasuries. In the wake of the invasion of Ukraine, the US showed they were not afraid to ‘weaponise’ the dollar-centric global financial system by imposing crippling sanctions on another nation state. As the world’s reserve currency, the USD gives the United States enormous leverage on the world stage.

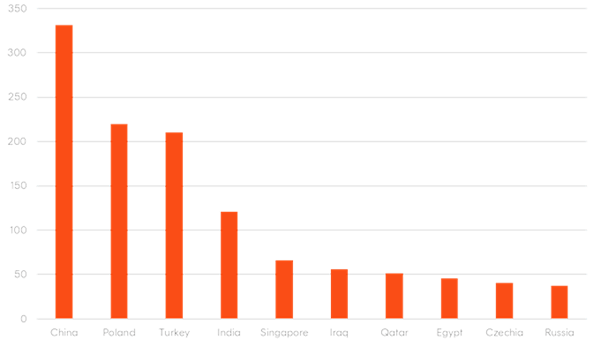

In response to this threat, the central banks of countries that wish to remain non-aligned or independent of the US have become huge buyers of gold in recent years. Since February 2022, total reported central bank buying has ramped up significantly, led by emerging market countries like China, India, Poland, Turkey and Egypt.

Largest central bank gold purchasers since 2022 invasion of Ukraine (in tonnes)

Source: World Gold Council. Net purchases and sales from 1 February 2022 to 31 December 2024.

Goldman Sachs also reported that central bank buying at the end of 2024 came in significantly higher than its expectations, particularly from China.

Cyclical support – consumers and investors

China and India are currently the world’s largest gold markets. Asia makes up more than 60 per cent of annual demand (excluding central banks), so these consumers and investors provide significant support for higher gold prices, according to data from the World Gold Council. China has seen a boom in demand for gold jewellery with millennials and Gen Z consumers driving this demand. In the second half of 2024, Indian demand jumped, thanks to strong economic growth and the reduction of customs duty on gold imports.

In addition, global investor appetite for gold ETFs finally turned around in 2024 and has then accelerated in 2025 with strong inflows into US and Australian gold ETFs.

Trump, tariffs and a rising US budget deficit

Gold has traditionally performed strongly in periods of uncertainty and when the economic outlook deteriorates.

While the initial reaction to Trump’s tariff announcements centered on the risk of inflation, fears have now spread to the implications for economic growth.

Any threat to US exceptionalism means global investors will shift capital out of the US to other regions – a net negative for the USD and net positive for gold. On a purchasing power parity basis, the USD remains above its long-term average and, given the level of volatility in currency markets, it may not take much for gold to rally strongly in USD terms.

In fact, if China offers stimulus to support its domestic economy from the headwinds of tariffs, we may see the USD fall in Australian dollar terms and gold rally in USD terms.

Furthermore, if the US deficit widens further under the new administration, concerns around the serviceability of US government debt may dampen investor appetite for Treasury bonds and weaken the USD. Historically, there has been a strong correlation between rising US budget deficits and gold prices. In this climate, currency hedging your gold exposure is an important consideration.

Investment implementation

In a period of escalating geopolitical tension and policy uncertainty, gold provides unique characteristics to diversify risk embedded in other asset classes. As such, adding some exposure to the USD gold price may improve diversification for traditional multi asset portfolios.

Cameron Gleeson is senior investment strategist for Betashares.

Leave a Comment

You must be logged in to post a comment.