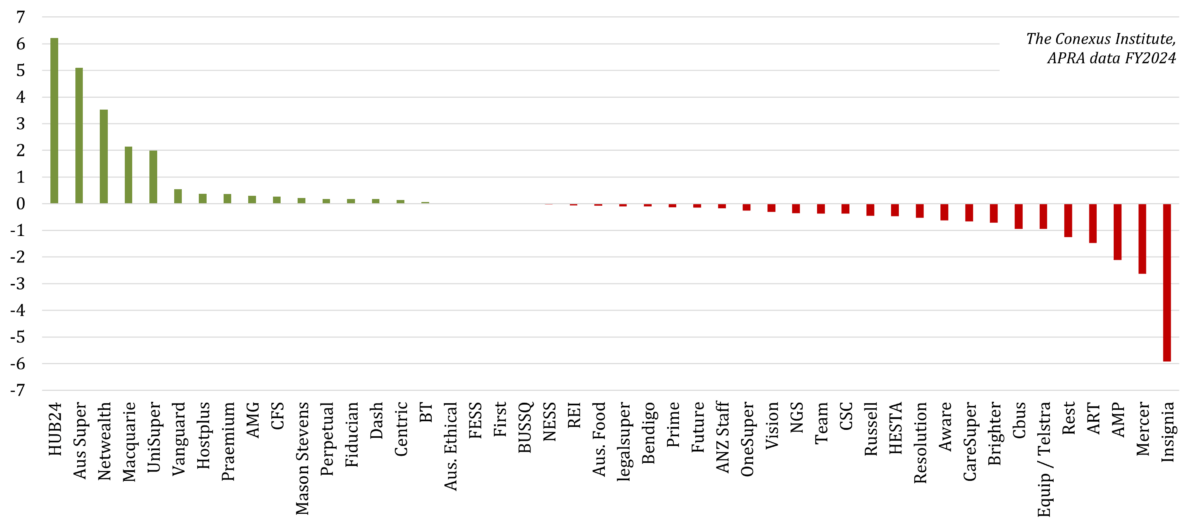

When it comes to driving competitive superannuation flows, advisers are the kingmakers and HUB24 and Netwealth are wearing the crown.

The annual State of Super report from The Conexus Institute*, which will be released publicly next week, found HUB24 ($6.2 billion) has even replaced AustralianSuper ($5.1 billion) as the leading fund in terms of competitive flows.

“Three years ago, I wouldn’t bet against AustralianSuper being number one on competitive flows,” the institute’s executive director David Bell said, who co-authored the report with research fellow Geoff Warren.

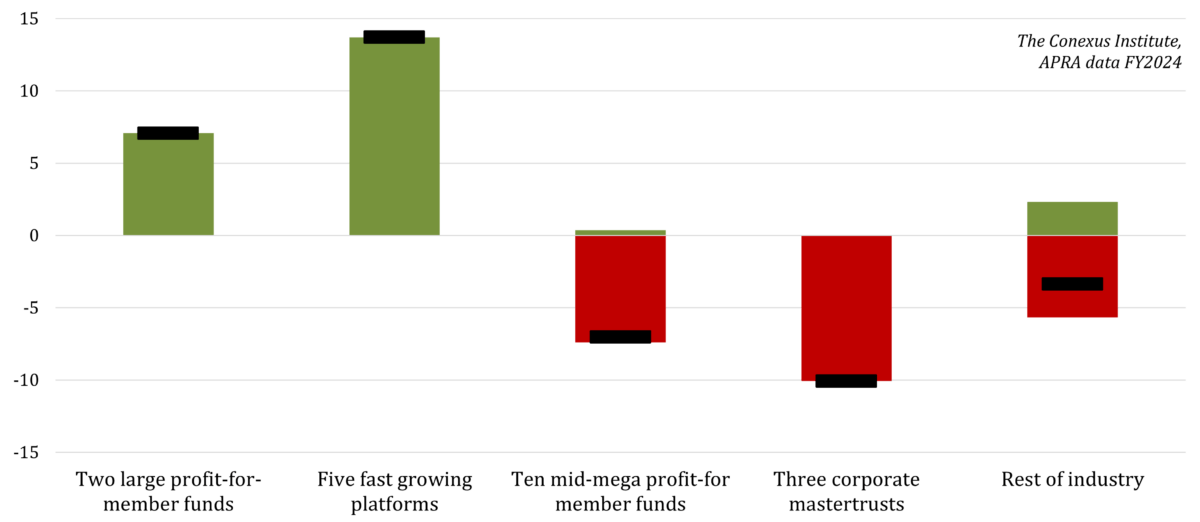

It’s a different story across different parts of the industry. Only two of the largest industry funds – AustralianSuper and UniSuper – have large competitive net inflows.

“AustralianSuper still has a strong position in terms of competitive flows, but this has deteriorated significantly over the last two years,” the report said.

The $365 billion fund experienced competitive flows of $15.4 billion in FY22, which declined to $9 billion in FY23 and then $5.1 billion in FY24.

“Looking deeper, we see a continuing trend towards falling rates of roll-ins and a sizable increase in roll-outs,” the report said.

On the retail side, the five fastest growing platforms – AMP North ($1.3 billion), CFS FirstWrap ($515 million), HUB24, Macquarie Super ($2.1 billion) and Netwealth ($3.5 billion) – also dominate competitive net inflows, largely due to a relationship with the advice sector which the institute cited as being the “strongest thematic” driving competitive flows during FY24.

CFS (across its aggregated super fund entities) and BT ($66 million) both experienced significant improvements in competitive flows to record modestly positive inflows during FY24, the culmination of a multi-year turnaround from FY22 when both experienced negative competitive flows of -$2.3 billion for CFS and -$3.1 billion for BT.

The report noted retail platforms that serve financial advisers require new members to offset their aging member profiles.

“While financial adviser numbers have fallen and are growing slowly, the objective of many platforms is to increase adviser efficiency thus enabling them to take on more clients,” the report said.

“Funds thus have…commercial incentives to improve their retirement offerings to buffer member numbers.”

Overall, in FY24, there was a total $74 billion in flows as a result of member fund-switching activity, amounting to just less than 3 per cent of total assets.

The report estimates $34.5 billion (47.5 per cent) involves a financial adviser, while the remaining $39.5 billion is an individual member decision.

Competitive flows for sub-groups of APRA-regulated super funds by value ($b)

Source: The Conexus Institute, APRA.

Source: The Conexus Institute, APRA.

But the story changes for the next ten “mid-mega” industry funds – Australian Retirement Trust, Aware Super, Brighter Super, CareSuper, Cbus, Equip/Telstra Super, Hesta, Hostplus, Rest and Vision Super – they’ve also suffered from competitive net outflows. The exception is Hostplus.

ART, the country’s second largest super fund, saw competitive flows drop by around $1 billion, with the fund encountering net outflows of $1.5 billion during FY24.

“It is unclear to what degree the change for ART may be related to member activity during merger transitioning,” the report said, referring to multiple mergers undertaken by the fund including Commonwealth Bank Group Super, AvSuper, Alcoa Super, along with members from Woolworths Group and Endeavour Group.

Troubled industry fund Cbus, which had a disastrous 2024 calendar year due to service issues along with scrutiny over its connection to the CMFEU union, experienced a sizable decrease in its competitive flow position to around -$0.9 billion. The data only captured FY24 so excludes the second half of the calendar year.

Additionally, the three corporate master trusts – AMP Super, Mercer Super and MLC Super – all had large competitive net outflows.

While the report found AMP North is in good health, with positive flows and comp flows, AMP Super had a tougher year.

“AMP’s competitive outflows of -$2.1 billion reflects the balance of two stories, with AMP North attracting net inflows of $1.3 billion that were more than offset by outflows of -3.4 billion from AMP Super,” the report said.

Insignia encountered a “meaningful deterioration” in competitive flows in FY24 by nearly $2 billion to net outflows of nearly $6 billion, “leaving them as a clear laggard in terms of competitive flows,” the report said.

APRA-regulated super fund sample ranked by competitive flows by value ($b)

Source: The Conexus Institute, APRA.

Source: The Conexus Institute, APRA.

Vanguard, which joined the superannuation sector in late 2022 experienced “strong” competitive inflows of $540 million in FY24, the sixth highest, but was a fall from the $720 million won in FY23.

Two years ago, the Institute reported there were 14 funds that controlled 80 per cent of APRA-regulated assets, but the addition of Care Super and the soon-to-be merged Equip/TelstraSuper combo will mean 16 large funds (over $50 billion in assets) control 87 per cent.

Spend to defend

Industry funds have faced mounting criticism for advertising spend, but the report shows as marketing spend has gone up, switching activity has gone down.

The institute suggests the marketing dollars have created a “spend to defend” strategy whereby funds use branding power to keep members in their fund.

But while that motivation is strong and justifiable at a fund-level, it may result in poor system level outcomes.

“There are arguments that marketing represents poor value for money because switching activity is falling,” the paper said. “However, there is also a possibility that marketing may reduce switching.”

The paper also noted the $481 million in overall spending activity may seem “headline grabbing” but represents only 0.02 per cent of assets in the system.

The paper posited that marketing can be directed at attracting new members and protecting the membership base from the marketing activities of other funds, and raised the question whether “spend to defend” activities could reduce member rollover.

“A member may be reassured by the marketing activities of their own fund, offsetting any impulse to explore other offers,” the report said.

“We imagine it is quite difficult to measure the member retention impact that results from fund marketing, especially at a system level.”

But the paper also questions whether a “spend to defend” strategy works if switching activity is driven by financial advisers.

*The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Professional Planner. To receive a copy of the full State of Super 2025 report, subscribe to The Conexus Institute’s Independent Perspectives newsletter.

Leave a Comment

You must be logged in to post a comment.