The Compensation Scheme of Last Resort will obliterate the $20 million subsector levy for financial advice, forcing the government to launch a review of the troubled scheme.

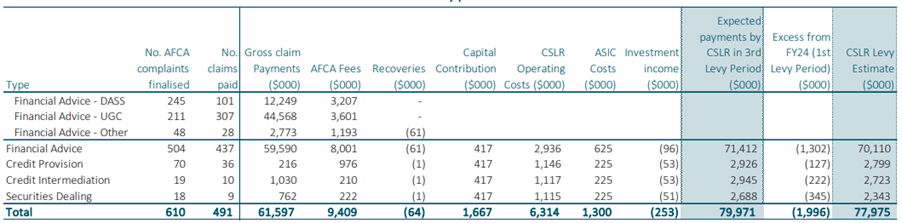

In figures released on Thursday morning, the scheme’s actuarial services provider Finity Consulting determined an initial levy estimate of $77.78 million for FY26, with $70.11 million of the total attributed to financial advice.

The estimate for financial advice is more than $50 million over the subsector cap of $20 million and, by law, a special levy will be necessary to raise the excess funding of the levy.

The other three sectors will only be required to cover $2 million to $3 million, including operating costs for the scheme.

“[I’m] disappointed it’s so high,” CSLR chief executive David Berry tells Professional Planner. He had previously foreshadowed the next levy period would surpass the subsector cap.

“But I can’t move away from the task that we’ve been given: to estimate what we see as the compensation payments that we’ll need to pay next year.”

Recommended initial levy estimate for FY26

Source: CSLR

The CSLR will register a legislative instrument next week for the full $78 million. ASIC can only levy up to the subsector cap of $20 million, although Berry is unable to confirm at this time what claims will be prioritised and covered.

From 1 July, the CSLR can notify the minister if there is a requirement for a special levy, but this will be proceeded by a revised estimate to confirm the figures.

With the impending retirement of Minister for Financial Services Stephen Jones, the burden of addressing the special levy will fall onto a new minister regardless of who wins the next federal election.

The next minister could ask the scheme to slow down compensation payments, pay in instalments, or levy other subsectors.

Once the minister has made the decision as to which of those options – or combinations of options – they want to pursue, it will then be lodged with Parliament and wait for approval by both houses.

The announcement of the excessively high estimate drew a swift rebuke from the financial advice industry.

Financial Advice Association Australia CEO Sarah Abood tells Professional Planner the estimate was “very surprising”, but noted the association’s general manager for policy, Phil Anderson, had predicted the levy estimate could be over $50 million last year.

The news also drew criticism from the Financial Services Council, Stockbrokers and Investment Advisers Association, the SMSF Association and CPA Australia.

Scope of the review

The same morning the CSLR reported its initial levy estimate, Treasury announced a comprehensive “post-implementation review” of the scheme.

The consultation period for the review closes on 28 February and aims to “improve understanding of the scheme’s operation and the outcomes it is delivering”.

The review will consider how the scheme is delivering on its intended objectives, how the scheme’s funding model is formulated – including its potential impacts on businesses who fund the industry levy, the current scope of the scheme and how the powers of the CSLR operator interact with delivery of the scheme.

The review is in addition to the Senate’s inquiry into Dixon Advisory, announced in September 2024.

Minister for Financial Services Stephen Jones said in a media statement on Thursday that ensuring the scheme is sustainably funded will be an important focus of the review.

“While industry has provided broad support for the CSLR, it’s important that there is confidence that the scheme is meeting its objective in a way that is sustainable for both companies and consumers,” Jones said.

The FSC said the review should reconsider whether the scheme should continue to compensate consumers who have received capital gains and instead focus on consumers who have incurred a loss.

The council is referring to the ‘but for’ provision in AFCA determinations which factors in where a client would be if they received good advice, as opposed to if there was capital loss suffered.

Shadow Minister for Financial Services Luke Howarth, who has been highly critical of the government’s handling of the scheme, said the CSLR has become a “disaster” under Albanese’s watch.

“The eleventh hour announcement of a review is too little, too late and urgent action is needed to get its costs down now,” Howarth said in a press statement.

“Changes are needed now and it is disappointing that the Albanese government isn’t ready to act.”

The CSLR was legislated in mid-2023 after the previous Coalition government failed to pass a bill before the 2022 election, despite support from Labor.

The scheme was a recommendation of the 2017 Ramsay Review and the Hayne royal commission.

The first levy advisers were required to pay (FY25) totalled $18.5 million – just short of the subsector cap – which came to $1286 per adviser, which came after the government fell short of its commitment to cover the costs of the first year of the scheme.

UGC surpasses Dixon

The highest number of claims to be paid by the CSLR is not those against Dixon Advisory but in fact claims made against Melbourne-based liquidated financial services business United Global Capital.

With a total of 307 claims estimated to be paid by the CSLR, complaints against UGC represent 70 per cent of the total expected compensation payments to be made during the FY26 levy period. The number of UGC claims is triple the number of those against Dixon Advisory, which is estimated to be 101.

“As you go through the report there are some big assumptions in there, particularly around UGC on the number of claims that will be paid and the size of the claims,” Berry says.

“Those have been done under the basis of actuarial principles. There’s not been much of an evidence base other than the information we’ve been able to get from ASIC and AFCA which is very preliminary.”

UGC entered voluntary administration in July 2024 having held an AFSL since 2017, following ASIC’s concern that UGC and its representatives gave conflicted personal advice.

Clients were advised to establish an SMSF and invest in risky investments which had connections to UGC’s sole director Joel James Hewish, despite advisers telling clients they were not receiving personal product advice.

The group relied on a client onboarding process that ASIC described as having “lured” people into investing into UGC products via phone calls from a third-party website operating offering a free superannuation “health check” – an issue the regulator has flagged as a growing concern and part of its ongoing enforcement activity for this year.

But Abood says the FAAA considers UGC a product failure which ties into their broader criticism of the CSLR, suggesting there is “huge incentive” to define these type of product failures as advice failures.

“Products failing are almost always the root cause of advice failures, and yet, because products are not part of the scope of the scheme, product failure isn’t compensated,” Abood says.

Dixon Advisory and UGC combined make up 92 per cent of claims paid by the CSLR.

Berry says that while UGC and Dixon are similar failures, the difference between the two is how the work is being prioritised by AFCA.

The complaints authority is working through pre-CSLR Dixon claims – which will fall under the $241 million levy covered by the 10 largest financial institutions – and this is why Dixon features less heavily the next levy period, Berry says.

“That pre-CSLR [levy] should be completed close to next year,” Berry says.

“We’re expecting by June 2026, they’re winding up all those complaints then they’re focusing on all the ones which were received after September 2022.”

The CSLR levy estimate report found there was no allowance for a failure like UGC in the first two levy periods (FY24 and FY25) as the firm had “not failed” at the time.

Leave a Comment

You must be logged in to post a comment.