Superannuation funds continue to fall short on delivering retirement income solutions for members, with the corporate and prudential regulators once again taking them to task over an underwhelming response to the Retirement Income Covenant.

In a joint statement on Tuesday morning, almost a full year after warning funds to do better on meeting their obligations, APRA and ASIC said significant gaps remain in funds’ responses, based on a new survey of 48 funds.

In July last year the regulators said super funds had “made a good start, but overall there has been a lack of progress and insufficient urgency”, in developing retirement income strategies after reviewing progress made by 15 funds.

A year later – and two years since the Retirement Income Covenant commenced – the latest survey, included in the Pulse check on retirement income covenant implementation report, has found 27 of the 48 funds surveyed cited uncertainty around the financial advice regulatory framework and potential law reform as an encumbrance to effectively implementing the covenant.

Exactly half of the funds cited the depth and availability of existing member data as an issue; as well as privacy, security and cost concerns surrounding the need to collect more data to better understand and support members’ needs, while 21 funds cited a general lack of member engagement and financial literacy relating to superannuation and retirement.

But despite these challenges, the report noted funds are pushing ahead with improvements, citing examples including undertaking research on member advice needs and expanding availability to advice, completing data gap analysis, and developing member journeys with tailored communications to promote engagement up to and through retirement.

In a media release accompanying the report, APRA deputy chair Margaret Cole said the most “concerning” finding of the survey was the lack of progress being made by funds in tracking the success of their strategies, “especially as this was highlighted as one of the key areas in need of improvement in the thematic review report”.

“Without effective success metrics, how can trustees know that their strategies are working?” Cole said. “Members deserve better.”

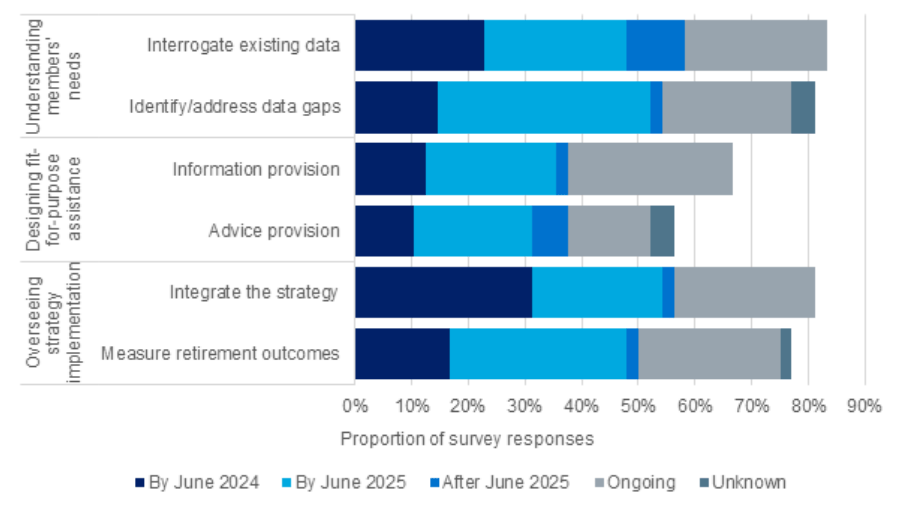

While “many” trustees had taken steps to better understand the retirement needs of their members, only one in five planned improvements were expected to be completed by mid-2024.

The Conexus Institute* executive director David Bell said the dispersion between funds on addressing the data gap is “astonishing and highly concerning”.

“The whole data piece is foundational to informing the overarching strategy formation, but the majority of funds won’t have that completed within the next year,” Bell said.

“We also have concerns that the data focus is on member characteristics, such as home ownership, partner status, etc.”

However, Bell said it’s just as important that funds focus on understanding how members wish to engage with their fund as they approach retirement.

“Are they self-directed, or will they seek a financial adviser, or would they appreciate some form of recommendation directly from their fund?” Bell said.

“Funds also need to focus on understanding member preferences around what they want in retirement and the trade-offs they are prepared to make. This data is more difficult to obtain but highly important.”

Areas of improvements identified by funds and estimated completion timeframe

Source: ASIC and APRA

When it comes to “designing fit-for-purpose assistance” for members as they move into retirement, Bell noted the focus is on only two categories – “information provision” and “advice provision” – despite there being a large area in the middle which is trustee guidance.

“An example is calculators with a concierge – this area will likely expand if qualified advisers become part of the scene,” Bell said, referring to the government’s Quality of Advice Review response that will create a second tier of adviser available to funds, insurers and banks.

“We’d encourage future surveys by APRA and ASIC to be a little more nuanced in this area.”

But given the lacklustre progress made by the industry, Bell said perhaps the covenant might not be the best vehicle to create an adequate retirement system.

“More prescription might be appropriate while creating a mechanism which ensures minimum baseline outcomes for retirees, no matter which fund they retire into,” Bell said.

He pointed the Institute’s submission to the Superannuation in Retirement Review which proposed the idea of a retirement licensing regime.

“When we see results like this, especially the dispersion between where funds are at,we feel even more convicted that this is an idea which warrants the consideration of policymakers,” Bell said.

Research from CoreData, presented at the Group Insurance Dialogue last year, found members were increasingly likely to switch funds due to poor service.

ASIC Commissioner Simone Constant said trustees are expected to use the report to assess gaps in their offering and “accelerate progress”.

“Trustees have a pivotal role to play in improving retirement outcomes for their members, with approximately three million Australians expected to join the six million already eligible to access their superannuation savings over the coming decade,” Constant said.

*Editor’s note: The Conexus Institute is a retirement-focused thinktank philanthropically funded by Conexus Financial, publisher of Professional Planner and Investment Magazine.

Leave a Comment

You must be logged in to post a comment.