APRA has clarified that managed accounts can be included as Trustee Directed Products in the Your Future Your Super performance test but it’s likely most will be exempted.

The YFYS performance test aims to set a benchmark for default products, starting with 76 of the 80 MySuper products in August 2021. In 2023 the test was expanded to include more than 800 choice products, a subset of TDPs, which are often advised.

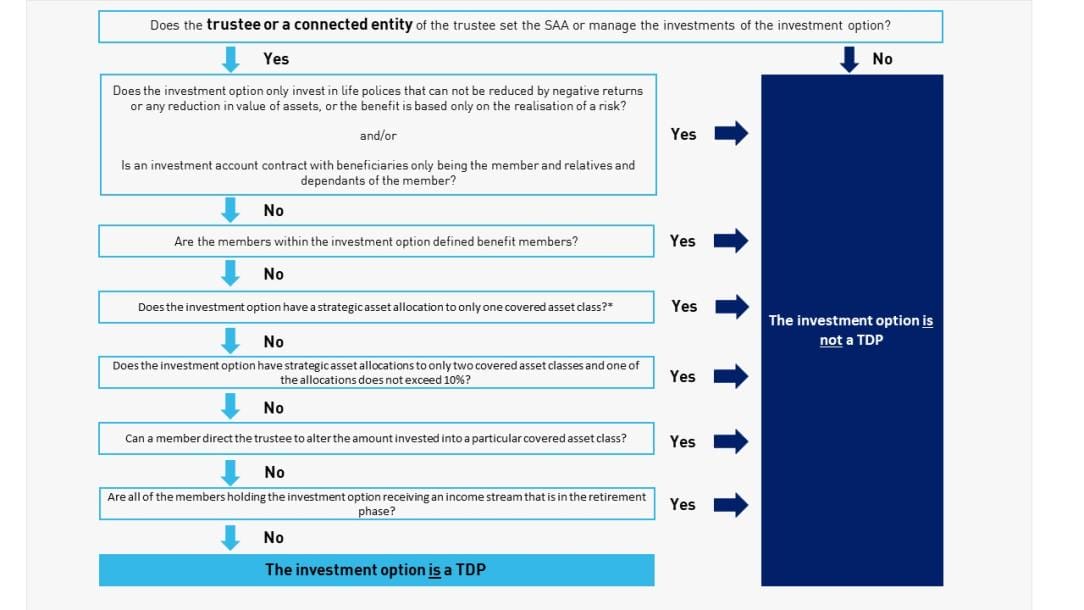

APRA published updated FAQs on Friday morning that say “SMAs and other managed accounts” can be TDPs, but this is determined by the ability of the “beneficiary to alter the strategic asset allocation of a particular covered asset class”.

“Per SIS Regulation 9AB.2(2)(c) of the SIS Regulations, if a beneficiary of the fund cannot require the trustee of the fund to alter an amount attributable to the beneficiary to be invested in a particular covered asset class in an investment option, then that product satisfies the TDP definition,” the guidance says.

“Conversely if a beneficiary can require the trustee of the fund to alter the covered asset class amount of the investment option then it cannot be a TDP.”

Financial Advice Association head of policy Phil Anderson tells Professional Planner the intention of the test hasn’t changed, but that trustees are being encouraged to consider whether SMAs might be caught under the test.

However, he notes that SMAs have specific and different features, and many of them allow the member to choose what’s included, which means it isn’t a standard product.

“There are a range of reasons why a significant proportion of SMAs will not be caught by this but ultimately it will come down to the make-up of it. Whether it’s a related party is the first key criteria, [then] whether it’s invested in a single asset class, and then whether the member has the ability to direct the trustee to vary allocation to investments,” Anderson says.

At this stage, Anderson says, it’s not something that advisers need to be concerned about.

“In most cases advisers will not be a stakeholder in this,” Anderson says.

“Ultimately, it’s the trustee who is responsible for determining whether it’s a Trustee Directed Product or not and therefore needing to go through the performance testing regime.

“Advisers will ultimately find out if the product fails and if the client gets a failure notification.”

APRA’s guidance also lays out the conditions that would determine whether the investment option should be covered by the test.

“Where it’s a separate product – for example, if it’s a completely different investment manager and some of the separately managed accounts are managed by a completely different entity – they would be excluded,” Anderson says.

How trustees can determine if their investment option is a TDP for the performance test

For example, if an SMA was designed by an asset manager and offered on a platform, asset manager and platform are completely different entities and wouldn’t be caught in the testing regime.

“It will [also] depend on the make-up of the SMA. If there’s more than one asset class in it, then there’s a risk [it will be included],” Anderson says.

“There’s a separate exclusion if there’s two asset classes but one of them makes up less than 10 per cent [of the allocation] and then there’s also the exclusion if a member can direct a trustee to alter the amount invested into a particular covered asset class.”

Anderson says it’s common for SMAs to allow clients to exclude certain investment options.

“It plays into that ethical investing line. You could choose to exclude resources companies, for example,” Anderson says.

“It’s very specific to the makeup of the SMA and how it fits and what it invests in and what powers the trustee has.”

At the Professional Planner Researcher Forum in March 2022, AMP group executive for advice Matt Lawler suggested the advice industry stay a step of the head of the regulators by implementing a managed account benchmark similar to YFYS.

The government has since reviewed the test, asking the broader financial services industry for feedback on the methodology of the test and whether retirement products should be tested.

Leave a Comment

You must be logged in to post a comment.