Embracing Standard 12 of the Code of Ethics and implementing it into our practice starts with recognising that although reporting is one component of accountability, it is not the only part, and there are a range of actions that are available.

In my previous column, I discussed the background on Standard 12 and how of a sample of advisers at the Financial Advice Association Roadshow earlier this year interpret the meaning of the standard.

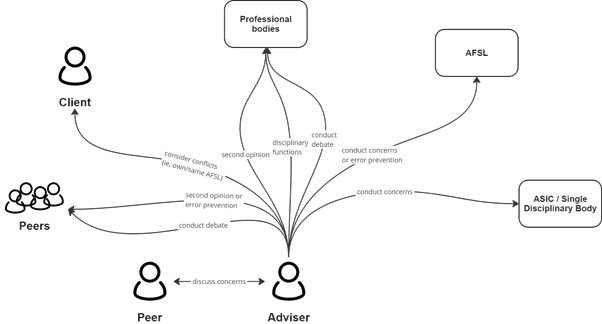

The range of accountability forums that exist for an adviser who has concerns is outlined below, along with the varied methods and functions that they may employ.

Attendees at the FAAA roadshow were presented with three scenarios that represented potential for poor conduct or advice. These were:

- Superannuation advice provided via a cold call marketing agency, to rollover existing funds on the basis of back-tested portfolio outperformance;

- Promotion of investment options with misleading portrayal of risks and potential returns; and

- Insurance replacement advice that ignored client concerns and contained important errors.

Attendees were surveyed on the options they would consider in each of these scenarios. For the first scenario, attendees were surveyed both at the start of the roadshow, and after being presented with the expanded view of accountability and Standard 12 found in the preceding two articles.

| Scenario 1 (start of Roadshow) | Scenario 1 (end of Roadshow) | Scenario 2 (end of Roadshow) | Scenario 3 (end of Roadshow) | |

| Discuss with the client | 32% | 24% | 27% | 29% |

| Discuss with the adviser | 10% | 21% | 26% | 25% |

| Peer discussion | 12% | 22% | 16% | 14% |

| Discuss with / report to AFSL | 25% | 20% | 20% | 23% |

| Report to professional body / ASIC | 20% | 13% | 11% | 9% |

| None of the above | 1% | 0% | 1% | 0% |

This survey demonstrated that once a wider view of accountability is taken, there was a far greater uptake in the option to discuss a concern with the adviser concerned, or another peer for feedback. It also showed that participants in the session considered that a wide range of options would be suitable, with some variation in responses driven by the facts of the scenario.

In raising concerns with any third party, the concern for the safety of our financial planning system can be paired with an appreciation that we rarely know the full facts of a situation. By understanding that we may know only part of the circumstances, we are able to approach a discussion with a peer with a spirit of curiosity over one of accusation.

This wider concept of accountability is also consistent with the aspect of Standard 12 that was included in the explanatory statement, and has seen less focus: “This Standard deals with relevant providers’ professional relationships with each other, emphasising that they need to be supportive and aligned to the profession as a whole—being, and being seen to be, a profession that acts ethically and professionally.

“One element of this duty affects relevant providers who are acting as supervisors for provisional relevant providers undertaking the professional year (see the Corporations (Provisional Relevant Providers Professional Year Standard) Determination 2018). This Standard requires that you must provide supervision that is in the best interest of the provisional relevant provider, that is, supervision that actively assists him or her in getting the full benefit of the professional year.”

The second paragraph of this explanation highlights the important role that teaching financial planning and ethical principles to new entrants to the profession plays.

Although it may not be immediately obvious, this can be linked to accountability and the prevention of errors in financial planning as discussed in ‘Analysing and Assessing Public Accountability: A Conceptual Framework’:

“Accountability forces administrators to trace connections between past, present and future.

“…accountability is not only about control, it is also about prevention. Norms are (re)produced, internalised, and, where necessary, adjusted through accountability.

“A profession’s ideology comprises its set of principles and teachings and also its myths and symbols. It is the whole set of conscious and unconscious beliefs and connotations which are invoked when a person says: ‘I am a professional’.”

Standard 12 exhorts us not just to hold ourselves and each other accountable for our conduct, but to impress the experience and standards of the profession into new entrants through training, coaching and debate.

Accountability literature supports this process as a key to greater levels of self-regulation for our profession, by highlighting that the judgment of a professional is necessary in determining the difference between what is right and wrong in the conduct of that profession:

“Only other members of the profession, once armed with all the facts of the case, can say whether the solution adopted was the correct one…

“…there can still be a role for judgment in cases which do not fit the exact scenarios of the prescriptive standards…”

In recent times, we have an example of a missed opportunity for self-regulation. The emergency measures as part of the initial Covid-19 response allowed the early release of superannuation and the controls on that release were extremely weak, potentially in response to the need for the early release to be delivered quickly to those in need, when Covid-19 and a rapid shift to work from home had reduced the administrative capacity of many superannuation funds.

There was some debate on industry forums about whether the ability to withdraw superannuation in conjunction with tax deductible contributions back into superannuation was something that ought to be permitted.

There are many circumstances where I would argue that taking advantage of this regulatory arbitrage, created by extraordinary circumstances, was not consistent with any sort of value system that is either set out in the profession, or that many individual practitioners would hold themselves. Yet there are circumstances where it may in fact have been appropriate to advise an individual to both withdraw using the Covid-19 early release scheme, and at a later point in time, following a change in circumstances, re-contribute those funds.

While there was a small level of debate within the profession, it was ultimately left to a regulator (the Australian Taxation Office) to instead release its own guidance, threatening the imposition of Part IVA on these transactions. While an effective deterrent, it is yet another example of standards being imposed from outside the profession, where there could have been opportunity to debate and decide for ourselves.

These articles have covered considerable ground in relation to the breadth of Standard 12 and accountability. It can seem overwhelming, but it is important to consider that each small step is incremental progress. If building greater accountability into our practice improves the outcomes for our clients, or takes a step towards the profession determining its own standards, that progress will compound over time.

Leave a Comment

You must be logged in to post a comment.