Standard 12 has received less coverage in trade press, submissions and debate as other parts of the Code of Ethics, and this may have resulted in some misconceptions.

According to the Code, Standard 12 states: “Individually and in cooperation with peers, you must uphold and promote the ethical standards of the profession and hold each other accountable for the protection of the public interest.”

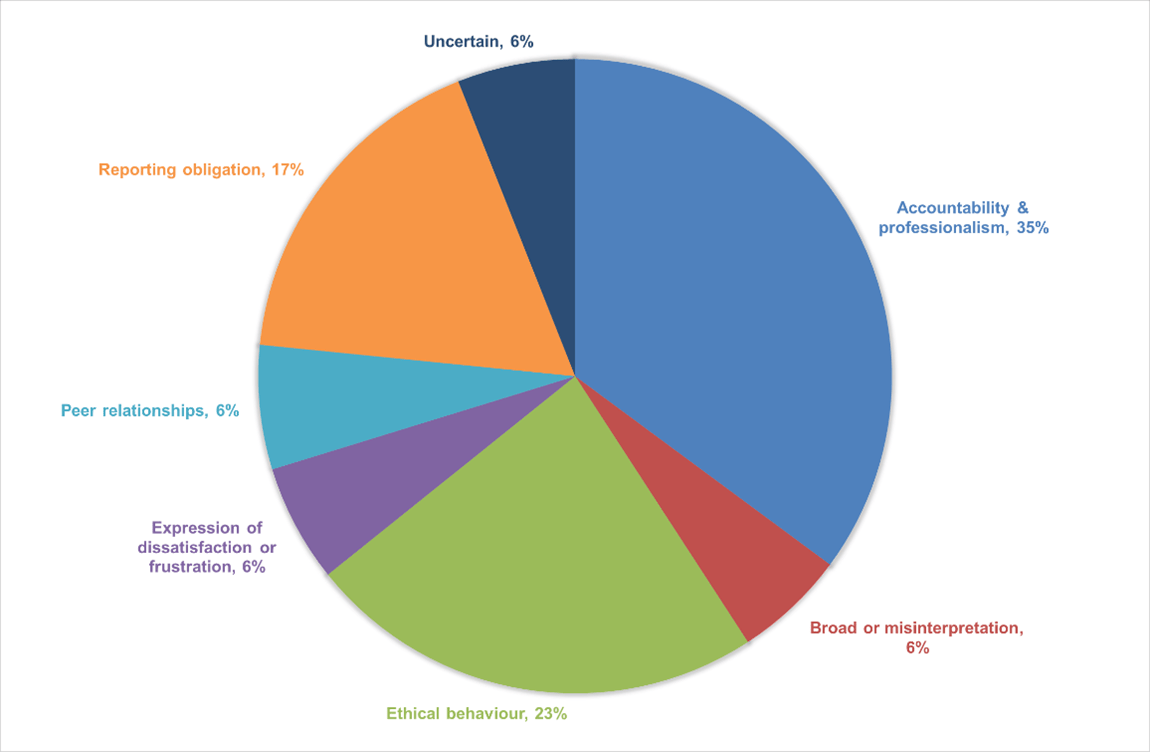

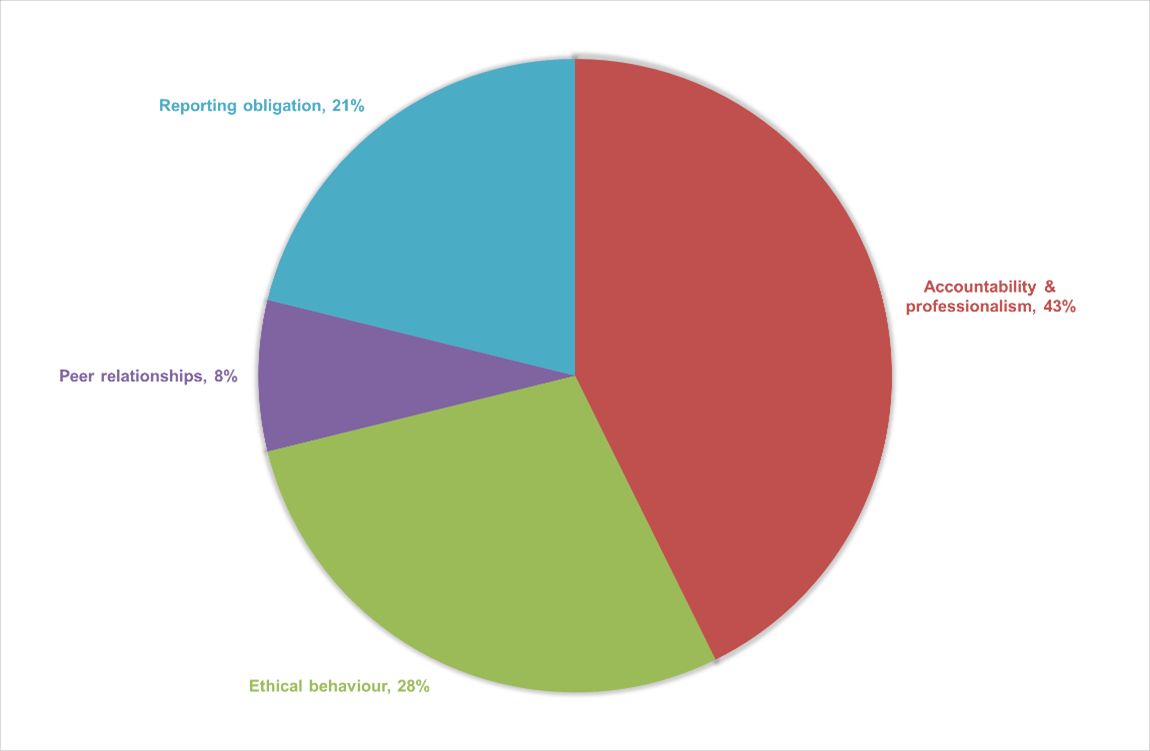

Participants in the Financial Advice Association’s roadshow that took place in ten venues across Australia earlier this year were asked to describe their initial impression of the standard. These results were grouped into categories, with the results as follows:

After removing those categories where the responses were exceptionally broad, a general expression of frustration about FASEA, or uncertain, the responses were divided into:

- Accountability & professionalism: 43 per cent

- Ethical behaviour: 28 per cent

- Peer relationships: 8 per cent

- Reporting obligation: 21 per cent

Standard 12 represents far broader concepts of professional accountability than initial discussions and impressions suggest. The standard can be broken into three components:

- Upholding and promoting the ethical standards of the profession;

- Holding each other accountable; and

- Protecting the public interest.

While Standard 12 and the code may be relatively new to financial planning as a profession, these components are commonly expressed in academic exploration of professionalism and accountability, and lessons can be drawn from the application of these concepts in other disciplines.

With the body responsible for creating the standards, FASEA, having been wound down, the opportunity for the financial planning profession to develop and integrate the standards is substantial. Existing financial planners have the experience of working with clients where standards must be applied to real client experiences.

Background

The perception of Standard 12 may in part be driven less by what was actually said, and more by two events that occurred in quick succession:

- The release of the final report from the Hayne royal commission, which included a recommendation for a Single Disciplinary Body for financial planning, in place of the code monitoring bodies that had been previously provided for; and

- The making of the Financial Planners and Advisers Code of Ethics 2019 legislative instrument on 8 February 2019.

The explanatory statement for the Code of Ethics did not have a strong focus on reporting or discipline at all.

“This Standard deals with relevant providers’ professional relationships with each other, emphasising that they need to be supportive and aligned to the profession as a whole—being, and being seen to be, a profession that acts ethically and professionally,” it stated in ‘The Values and Standards’ section for Standard 12.

“One element of this duty affects relevant providers who are acting as supervisors for provisional relevant providers undertaking the professional year (see the Corporations (Provisional Relevant Providers Professional Year Standard) Determination 2018). This Standard requires that you must provide supervision that is in the best interest of the provisional relevant provider, that is, supervision that actively assists him or her in getting the full benefit of the professional year.”

This emphasised that professionalism was important in promoting the ethical standards, and hints that this standard is as much about relationships between professional financial planners, as it is with their clients.

The second aspect of the explanatory statement points to how the duty to uphold ethical standards is particularly relevant in the professional year process that seeks to introduce a new entrant into the profession.

Some reporting aspects are introduced in the 2019 guidance with an example of a financial planner who has identified that advice previously provided to a client of his firm was inappropriate, and speaks to the requirement to get independent assistance with any claim for compensation.

The 2020 guidance then introduces some stronger language around accountability, including that holding each other accountable includes “demonstrating a willingness to challenge others who are not upholding the values and standards.” The first reference to third-party reporting is introduced in an example of concerns about advice provided by another planner, and references a professional obligation to report for further investigation.

In considering this background and the examples offered, a planner might consider whether they are much more than a logical application of the five values that also reside in the Code of Ethics:

- Trustworthiness

- Competence

- Honesty

- Fairness

- Diligence

Exploring complimentary professions and research

If we can accept that our initial impressions of Standard 12 may be narrower than the text of the standard suggests, that it includes, but is not limited to, reporting and sanctions, where can we look to understand more?

Two areas that we can explore are:

- How similar provisions operate in other professions; and

- Research into the concepts of professionalism and accountability.

While exploring the research may seem overly academic, it provides us with the language or taxonomy of professionalism, so that we’re better equipped to discuss what these issues mean, and advocate for the importance of our experience and ability to define our own future.

In ‘Analysing and Assessing Accountability: A Conceptual Framework’ by Utrecht University School of Governance Professor Bovens, he offers a definition of accountability that is useful to explore: “The most concise description of accountability would be: ‘the obligation to explain and justify conduct’.

“This implies a relationship between an actor, the accountor, and a forum, the account-holder, or accountee (Pollitt 2003, 89). Explanations and justifications are not made in a void, but vis-à-vis a significant other. This usually involves not just the provision of information about performance, but also the possibility of debate, of questions by the forum and answers by the actor, and eventually of judgment of the actor by the forum.”

The first aspect of this definition talks to accountability being an aspect of relationships. If there is not a relationship there is no need for accountability.

The second useful definition that it introduces is that of an accountability forum, that is a place where accountability occurs.

The third nuance from this quote is the highlight that accountability is not a one‑way process, and is not solely comprised of a judgment and/or sanction. It highlights that accountability may involve a process of debate and discovery, because there is a great deal of uncertainty, or things that we don’t know, in accountability.

A wonderful example of this role of relationships and debates in accountabilities can be found in the Actuaries Institute Code of Conduct. This code requires that where a member believes that another member may have acted inconsistently with their ethical obligations, that the first course of action ought to be “taking reasonable steps to discuss with the member.”

Contrast this with the initial impressions of Standard 12 that touched on the language of reporting and misconduct, where one in five responses highlighted the role of reporting, but less than one in ten referred to peer relationships.

Remember that the standards in the Code of Ethics are divided into four categories:

- Ethical Behaviour (standards 1 – 3)

- Client Care (standards 4 – 6)

- Quality Process (standards 7 – 9)

- Professional Commitment (standards 10 – 12)

There is a very direct accountability in an adviser/client relationship, and the primacy of this accountability is reflected in the first three categories being directly focussed on that relationship between planner and client, and the work you do for them.

The professional commitment category in contrast is about the relationship that you have with others. Your profession, your peers, and regulators.

One step at a time

The actuaries’ approach of first discussing your concerns with the peer you may be concerned about could be a challenging concept – it takes a large dose of courage to raise this with a fellow financial planner where you may have no pre-existing relationship.

Accountability may not need to start with strangers, but rather from considering who are the peers you currently know and have developed a relationship of trust that would support this type of conversation.

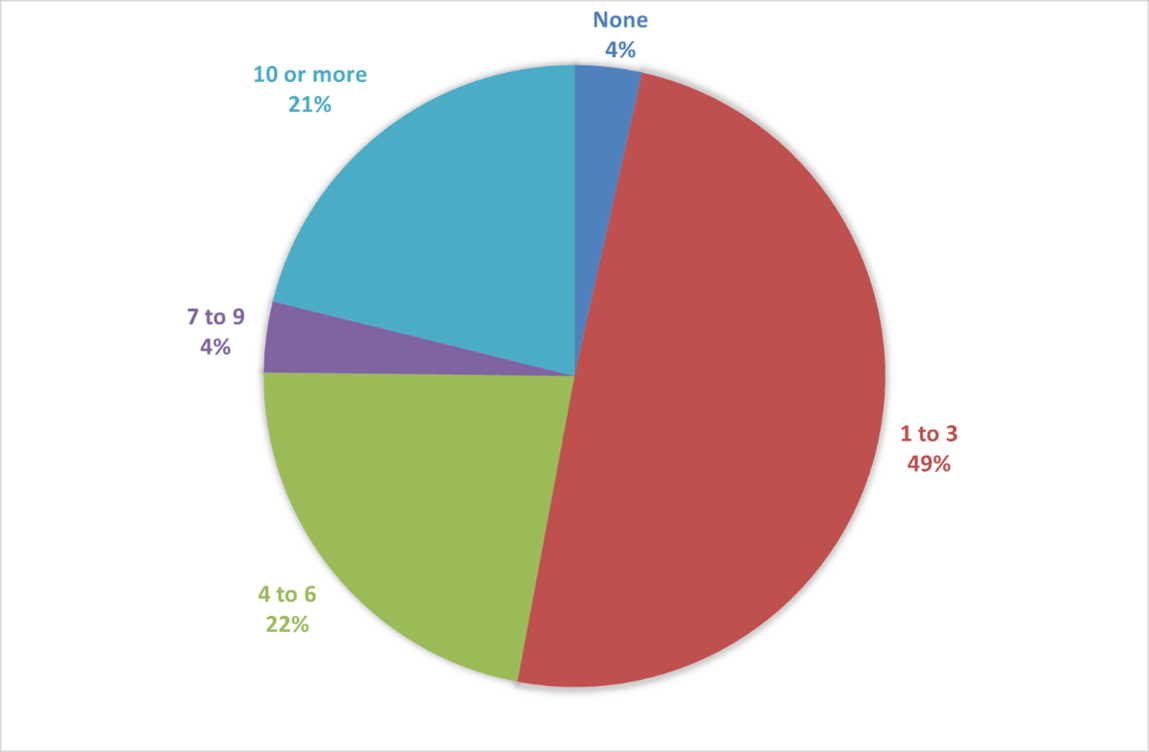

Attendees at the FAAA roadshow were asked: “How many of your colleagues would you be comfortable having an accountability discussion with?”

The results to this question showed that very few had no colleagues that they would feel comfortable discussing a question or concern about professional conduct with. Nearly half of respondents had at least one to three close colleagues, with a further 47 per cent of respondents having four or more colleagues they would be comfortable approaching.

Professional association and other networking events also have a role to play in building and extending that network further, in turn increasing the scope for high quality discussions amongst practitioners about professionalism and accountability.

Michael Miller is a Certified Financial Planner and director at Capital Advisory.

Leave a Comment

You must be logged in to post a comment.