*This article is produced in partnership with J.P. Morgan Asset Management Australia

Global demand for exchange-traded funds (ETFs) has grown rapidly in recent years, and has been accompanied by the development of more sophisticated smart beta and active strategies1.

ETFs present relatively attractive features such as flexible intraday trading, efficient market access and potentially lower costs. While passive strategies continue to dominate flows into ETFs, investors are increasingly realising the ETF ecosystem also presents actively managed strategies.

The active opportunity

Actively managed ETF strategies present investors with the opportunity2 to seek alpha on their investments while tapping into some of the relatively attractive features of the overall ETF vehicle.

- Active ETFs allow investors to target specific outcomes. For example, an active equity ETF can seek excess returns above a chosen index, driven by fundamental stock selection.

- In active strategies, the sector weighting and stock selection methodologies are at the discretion of the portfolio manager. Active fixed income ETFs, for example, have the ability to assess the creditworthiness of individual issuers and deviate from the weighting methodology of traditional benchmarks.

- Active strategies can be used to gain exposure to certain investment themes, such as securities with environmental, social and governance characteristics.

- Active ETFs can rebalance portfolios outside of the systematic and typical rebalancing periods used in passive strategies. This, for example, can provide active ETF managers with the flexibility to react to market events.

Demystifying myths on ETF liquidity

As investors warm up to actively managed ETF strategies, one of the most important ETF features – their liquidity – is also one of the most widely misunderstood3.

Liquidity refers to the ability to buy or sell a security quickly, easily and at a reasonable price. ETFs and individual stocks both trade on a stock exchange, leading investors to believe the factors that determine the liquidity of the two securities must also be similar. They are not. ETF liquidity can often be greater than investors assume.

Another common misconception is that funds with low daily trading volumes or with small amounts of assets under management will be difficult or expensive to trade. This is not the case.

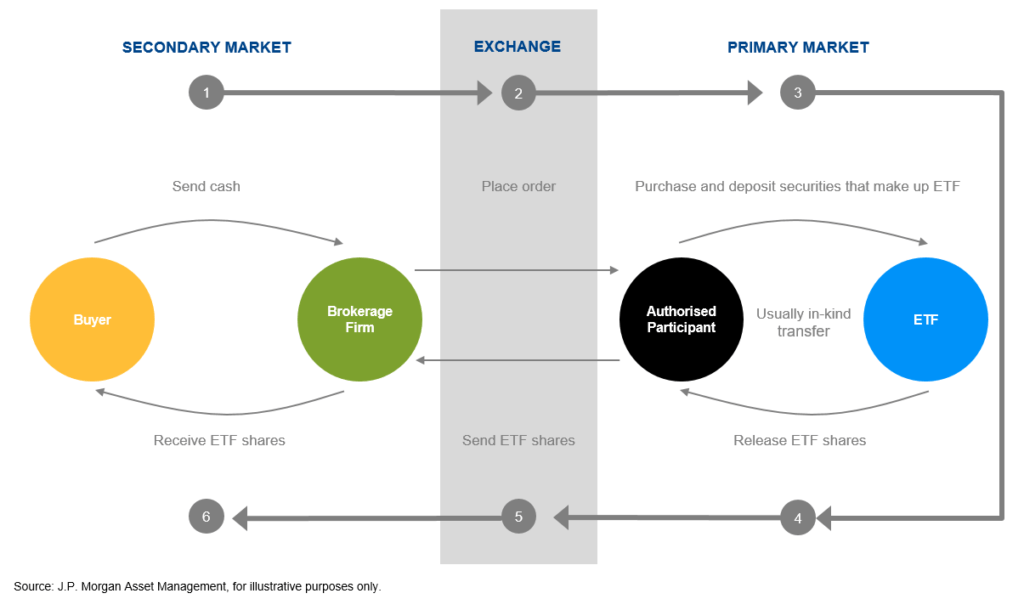

The ETF ecosystem: investor trading occurs in the secondary market with creation and redemption in the primary market

Source: J.P. Morgan Asset Management, for illustrative purposes only.

Source: J.P. Morgan Asset Management, for illustrative purposes only.

ETFs operate in a fundamentally different ecosystem to other instruments that trade on stock exchanges, such as individual stocks or closed-end funds. Whereas these securities have a fixed supply of units in circulation, ETFs tend to be open-ended investment vehicles with the ability to issue or withdraw units on the secondary market according to investor supply and demand.

This unique creation and redemption mechanism means that ETF liquidity is deeper and more dynamic than stock liquidity. An ETF’s liquidity is predominantly determined by the liquidity of its underlying individual securities ability to issue or withdraw units when needed, rather than by the size of its assets or by on-screen trading volumes.

Some dos & don’ts when assessing ETF liquidity

- Don’t use trading volumes or fund size as a guide. Due to the ETF creation and redemption mechanism, small- or low-trading-volume ETFs can absorb large buy or sell orders while continuing to trade at prices that remain close to the net asset value of their underlying securities.

- Do look at total ETF liquidity in the secondary and primary markets. Investors may find that secondary market liquidity is higher than on-screen indicators suggest because market makers, who maintain continuous two-way (buy & sell) ETF orders, typically display only a small fraction of the volume they are willing to trade. Investors with large trades can tap into primary market liquidity by working with the Capital Markets team at the issuer to take advantage of creating or redeeming transactions directly with the fund company.

- Do work with a financial adviser or ETF provider. Most providers have capital markets desks whose role is to work with portfolio managers, authorised participants, market makers and stock exchanges to help uncover true ETF liquidity and assist investors with trade execution.

Conclusion

As demand for active strategies grows and more active ETFs are launched, it is important for investors to have a full understanding of the role they can play in overall portfolios, and to pay close attention to the investment strategy.

Disclaimer:

Provided for information only based on market conditions as of date of publication, not to be construed as offer, research or investment advice. Forecasts, projections and other forward looking statements are based upon current beliefs and expectations, may or may not come to pass. They are for illustrative purposes only and serve as an indication of what may occur. Given the inherent uncertainties and risks associated with forecast, projections or other forward statements, actual events, results or performance may differ materially from those reflected or contemplated.

Diversification does not guarantee investment return and does not eliminate the risk of loss.

- Source: “Evaluating active ETFs”, J.P. Morgan Asset Management, 2022

- For illustrative purposes only based on current market conditions, subject to change from time to time. Not all investments are suitable for all investors. Exact allocation of portfolio depends on each individual’s circumstance and market conditions.

- Source: “True ETF liquidity”, J.P. Morgan Asset Management, 12.09.2022.

AU disclaimer for external

Source – JPMorgan Asset Management (Australia) Limited ABN 55 143 832 080, AFSL No. 376919

All investments contain risk and may lose value. The information provided on this article is general in nature only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information on this website you should consider the appropriateness of the information having regard to your objectives, financial situation and needs. Before making any decision, it is important for you to consider the appropriateness of the information and seek appropriate legal, tax, and other professional advice. Prior to making an investment decision, investors should read the relevant Product Disclosure Statement and Target Market Determination, which have been issued by Perpetual Trust Services Limited, ABN 48 000 142 049, AFSL 236648, as the responsible entity of the fund available on https://am.jpmorgan.com/au.

Leave a Comment

You must be logged in to post a comment.