The number of listed financial advisers has declined precipitously since its peak of 28,000 in late 2018. Depending on who you ask, the number now is closer to 18,000.

As painful as the experience has been for advisers, the impact on consumers amounts to about 1.2 million unadvised with not much hope of being reabsorbed into the advice ecosystem.

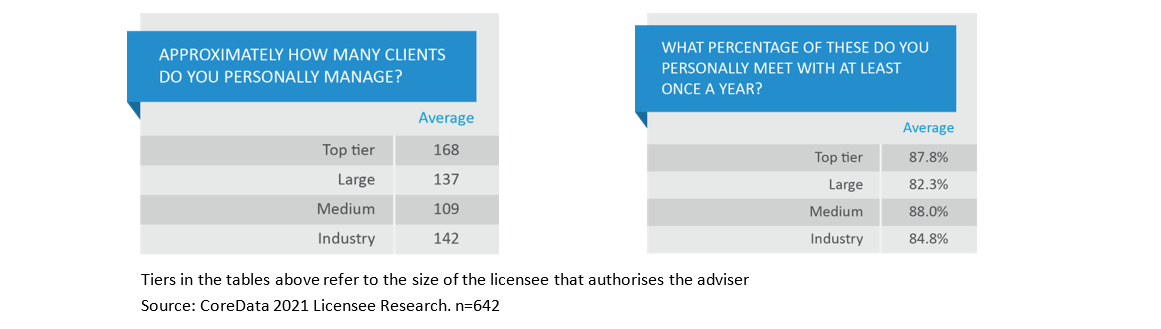

CoreData research shows consistently that the average number of clients per adviser is something in the order of about 140. That’s supported anecdotally in conversations with licensees, who tell us that in cases where the figure is materially higher than this, advisers are actively taking steps to cut numbers back.

There are always outliers – one adviser has tried more than once to tell us he has 1,500 active clients and meets them all once a year, which means he’s conducing more than 30 client meetings a week for 48 weeks of the year, or six a day every working day of the week. We consider that to be unlikely.

In addition, our research tells us that on average, advisers meet with about 85 per cent of their clients (roughly 120 clients) at least annually.

It’s almost impossible to say with certainty how many clients have been left newly unadvised in the two-year adviser exodus but based on what we see in the Licensee Research and what we also see in our quarterly Adviser Pulse Check surveys, we can take an educated guess.

It’s almost impossible to say with certainty how many clients have been left newly unadvised in the two-year adviser exodus but based on what we see in the Licensee Research and what we also see in our quarterly Adviser Pulse Check surveys, we can take an educated guess.

If we assume each adviser has 120 active clients (those they meet with once a year) and approximately 10,000 advisers have left the industry, that’s theoretically around 1.2 million individuals whose advisers have left the industry and who may not now be receiving financial advice.

(It should be stressed that we’re dealing with averages here, and we don’t really know how many clients each of the departed advisers had nor how many of those clients found a new home. It’s a ballpark figure, but a reasonable one.)

While advisers continue to leave the industry, those who remain tell us consistently that business growth in the next 12 months will primarily come from acquiring new clients. Regardless of the survey we look at, around 90 per cent of advisers say new clients will be the engine of growth.

We took this question a step further in a recent Pulse Check survey when we asked how many more clients advisers thought they could take on to reach “full capacity”. What we assume here is that “full capacity” is the industry-average figure of 120, and the percentage increase nominated by an adviser will bring them up to that figure.

In other words, when an adviser says they could increase client numbers by 10 per cent to reach “full capacity”, we assume they mean they could put on 11 new clients. That is, they currently have 109 clients and could put on 11 new clients to reach 120.

For example, around 10 per cent of advisers say they could put on 10 new clients. If we apply that across the industry, assuming 18,000 advisers remain in the profession, then 1,800 advisers could put on 11 new clients each, and that would total 19,800 new clients.

When we add all of these up, we find around 13,500 advisers with capacity to put on an estimated 313,700 new clients.

| Approximately what percentage increase in the number of clients you serve would it take for you to be at “full capacity”? |

||||

| Potential % client increase | % of total advisers | New clients per adviser |

No. advisers | Aggregate no. of new clients |

| Up to 10 per cent | 10.0% | 11 | 1,800 | 19,800 |

| 11 to 20 per cent | 23.4% | 20 | 4,212 | 84,240 |

| 21 to 30 per cent | 23.9% | 28 | 4,302 | 120,456 |

| More than 30 per cent | 17.7% | 28 | 3,186 | 89,208 |

| I am at full capacity now | 15.3% | 0 | 2,754 | 0 |

| Seeking to reduce clients | 9.6% | ? | 1,728 | ? |

| 313,704 | ||||

| Source: CoreData Adviser Pulse Check Survey Q3 2021. n=209 | ||||

What we broadly conclude – and we can argue about the exact numbers – is that with the best will in the world, the financial advice profession as it exists today cannot hope to mop up all newly unadvised clients.

If fact, in an absolute best-case scenario it could absorb roughly only a quarter of them – and that’s assuming advisers take on no new clients other than those who’ve recently lost their adviser. It just cannot happen.

It’s important to reinforce that there are a number of assumptions built into all of this, and this article is not meant to be a definitive analysis of the numbers. Rather, it is an attempt to describe the magnitude of the problem that has been created and to highlight the urgency of finding alternative ways of looking after individuals whose advisers have departed the profession.

Advisers will continue to grow their businesses by attracting new clients and providing invaluable advice and guidance. These individuals are likely to have their lives significantly improved by the advice experience. Unfortunately there appears to be a significant number of people for whom that opportunity may be lost.

Leave a Comment

You must be logged in to post a comment.