Earlier this year IOOF commissioned CoreData Research on a project designed to really get to grips with how clients of financial advisers experience advice and their perceptions of its benefits. IOOF aimed to explore whether individuals who do not currently receive financial advice have, in fact, any of the same needs that advice has met for those who’ve received it. And it sought to address the barriers that prevent more people from seeking advice.

It was an ambitious project. In the end, a survey underpinning the research received more than 11,600 responses from advised clients – an unheard-of number – and more than 1000 responses from unadvised individuals.

The scale of the response is testament to how enthusiastically advisers right across IOOF’s advice networks embraced the exercise, and it’s good for more than just bragging rights. At a practical level, such a large number of responses allows deep analysis and segmentation of the respondents to produce detailed and reliable insights into what the clients of financial advisers really think.

The resulting True Value of Advice research paints a detailed picture of a financial advice industry delivering clear tangible and intangible benefits for clients, and delivering outstanding value for money; and of financial advice that has clear value and benefits for a much wider cross-section of the community than currently receive it.

At a high level, 90 per cent of advised clients say that accessing financial advice has left them in a better position financially, and 89 per cent report that receiving advice has allowed them to lead their desired lifestyle. Ninety per cent of advised clients agree that their financial adviser is a critical partner in their financial success, and 93 per cent rate their adviser as good or very good with respect to the value of their services.

The report leaves little doubt that advice would have considerable value for more people, if only they were to receive it. The report identifies the needs that financial advice has met for those who have received it and the goals it has helped them to achieve, and shows that unadvised individuals have many of the same needs and goals. It shows that the barriers preventing more people from seeking advice are therefore often perceived rather than real.

The return on an investment in advice

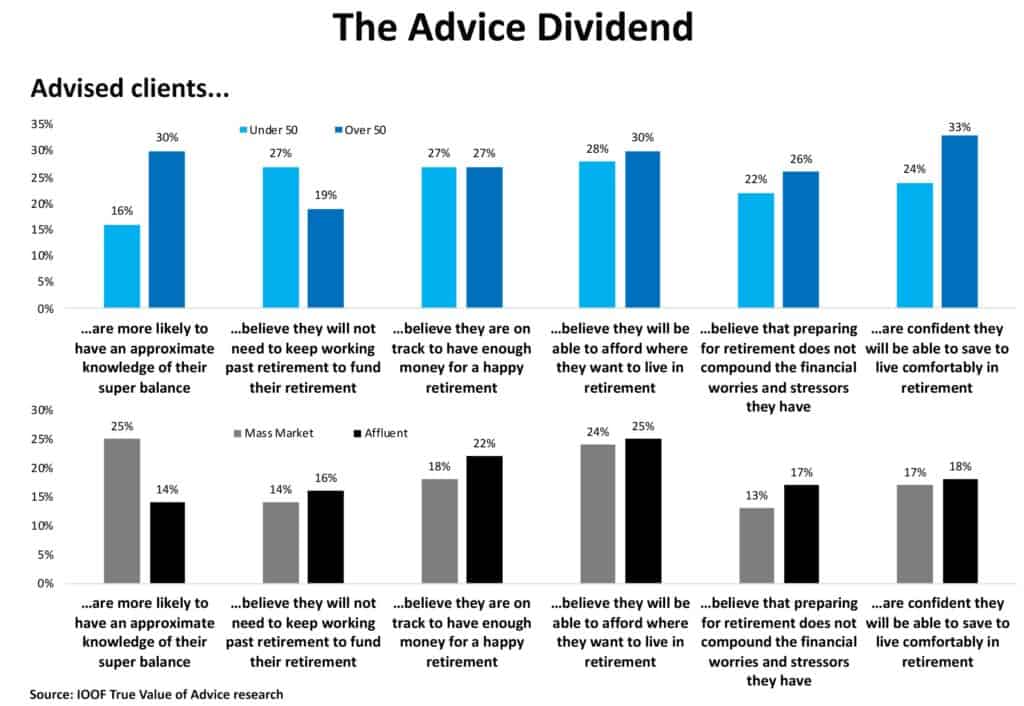

The Future Value of Advice report introduces the concept of the Advice Dividend. This can be thought of as the return advised clients receive for the investment they make in seeking professional financial advice.

Put simply, the advice dividend shows how much better off people who receive financial advice are than people who have not received advice. It is calculated by comparing the proportion of advised clients responding to a particular question with the proportion of unadvised individuals who respond to the same question the same way.

The size of the survey sample means we were able to segment the responses and still draw significant conclusions, and for the first time it is possible to say with a high level of confidence that the value of advice transcends age, wealth and gender.

In other words, the research has proved that financial advice has value – that it leaves people better off – whether that individual is older (over 50) or younger (under 50), relatively wealthy (affluent) or relatively less wealthy (mass market). This debunks the common misconception that advice is a service with greatest value for older, wealthier people.

In fact, the advice dividend is greater on some measures for younger individuals than it is for older individuals and it is greater on some measures for relatively less-wealthy individuals than it is for relatively wealthy individuals.

Furthermore, an advice dividend exists for financial and non-financial (tangible and intangible) measures. For example, an advice dividend exists for advised clients by being less likely than unadvised individuals the believe they will not need to work past retirement age to fund their retirement. But the advice dividend for advised clients aged under 50 is 27 percentage points, while for advised clients aged over 50 the advice dividend is 19 percentage points. The advice dividend is greater for the younger cohort than for the older; advised clients aged over 50 are 27 percentage points more likely than unadvised individuals to believe they won’t need to work past retirement.

The IOOF True Value of Advice research has produced a wealth of insights, which IOOF will be sharing with its own advisers and with the advice community more broadly.

The IOOF True Value of Advice research has produced a wealth of insights, which IOOF will be sharing with its own advisers and with the advice community more broadly.

The research demonstrates empirically that advice has value for a much broader segment of the Australian population than was previously supposed, and that many of the barriers that put people off seeking advice are perceived, rather than real.

Both of these issues assume great significance as ASIC consults with stakeholders on how to make financial advice more accessible and affordable for more people. We now have the evidence to show that if the industry can be unshackled to deliver the advice the research tells us people need, the take-up could be truly astronomical.

Simon Hoyle is head of market insight for CoreData Research

Leave a Comment

You must be logged in to post a comment.