We have commenced one of the busiest weeks in reporting season and JB Hi-Fi and Kogan have both hit the ball out of the park. Back on 11 June JBH gave a trading update suggesting total sales for FY20 ending 30 June, would amount to A$7.86 billion and net profits $300 to $305 million. Instead the company reported sales of $7.9 billion and profits of $332 million, indicating less price discounting, favourable mix shift and an acceleration of consumer spending ahead of the end of the tax year.

Perhaps more importantly, trading conditions for JB Hi-Fi in July reveal further acceleration:

- Total sales growth for JB HI-FI Australia was 42.1per cent (July 2019:4.1per cent) with comparable sales growth of 44.2per cent (July 2019:3.2per cent)

- Total sales growth for JB HI-FI New Zealand was 9.1per cent (July 2019:-0.4per cent) with comparable sales growth of 9.1per cent (July 2019:-0.3per cent)

- Total sales growth for The Good Guys was 40.4per cent (July 2019:-2.1per cent) with comparable sales growth of 40.4per cent (July 2019:-3.4per cent)

And for August, the company noted: “The Group has seen a significant acceleration in online sales in Victoria in the first 11 days following the stage 4 temporary store closures. This, combined with continuing sales momentum across the rest of Australia, has resulted in the Group achieving strong sales growth in August to date.”

It all looks incredibly positive and explains JBH’s share price surge to new all-time highs.

But the company also noted; “While we are pleased with our start to FY21 and current trading, in view of the uncertainty arising from Covid-19, we do not currently consider it appropriate to provide FY21 sales guidance.”

One of the great uncertainties of course relates to the level of government fiscal support, upon which a great deal of the current consumer prosperity relies.

Federal government support for workers, households and business totals more than $260 billion or 13 per cent of GDP. It is also the case that at the time of writing, $31 billion has been withdrawn from superannuation under emergency access provisions.

There is little doubt that the combination of support and stimulus measures has helped the economy by maintaining consumption and spending and therefore jobs for employees, and dividends for shareholders – many of whom are retired and reliant on dividend income to fund their own spending.

Less certain however is whether the current level of fiscal support will continue and that probably explains the qualifications offered by JB Hi-Fi and others.

It is worth noting JobKeeper 2.0 and the tapering of other measures proposed by government is expected to result in a significant moderation of stimulus.

According to ANZ Senior Economist, Cherelle Murphy, government stimulus measures injected $64 billion into the economy in the third quarter but tapering will reduce fourth quarter stimulus by $50 billion. In other words the outlook, in the absence of further stimulus, is ugly.

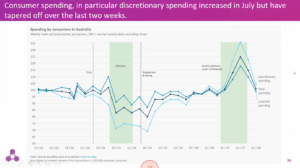

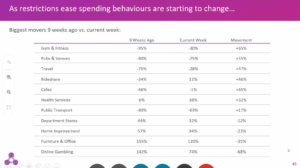

This view was also reflected in a data presented by Accenture/Illion & Alphabeta (below) in mid August, seen in the mean reversion of growth rates.

Source: Illion & Alphabeta (part of Accenture)

The above table, for example, shows that nine weeks ago spending on furniture and office equipment was up 155 per cent versus a normal November week pre-Covid. In the week beginning 10 August however, sales were up 120 per cent compared to that ‘normal’ week. In other words, while spending is still higher than a normal week, the rate of growth is moderating. One can only imagine that tapering of stimulus will dampen spending further. That sentiment prompted the Illion presenter to comment towards the end of the webinar; “We’re in a halcyon period before turning to custard”.

And keep in mind even the government’s own forecasts for employment aren’t confidence inspiring. The government forecasts 200,000 jobs will be created in the next year but about 600,000 jobs have been lost in Australia thus far. In other words, the government’s own forecasts for employment conditions, which include the impact of stimulus, are quite soft.

Some investors and commentators are taking comfort in the forecast that GDP growth will be strongly positive in coming quarters but the changes are coming off an absolute level that has rebased much lower. The absolute level of Australian GDP is not expected to reach 2019 levels until 2022 or even 2023. That renders quarterly growth rates and traditional definitions of recession as somewhat redundant.

All of this suggests that large government budget deficits will not be a barrier to the government further stimulating rather than waiting for the private sector to take up the slack.

Yes, these programs will result in huge debt burdens that will need to be cleaned up in the future – through higher taxes, inflation or financial repression but they will be necessary for the economy to survive.

The challenge for investors is to decide to what extent further government stimulus, which looks almost guaranteed, provides a positive catalyst for share prices sufficient to offset the many risks.

Leave a Comment

You must be logged in to post a comment.