The advice footprints of industry funds with active inhouse advice strategies have remained static at best and in some cases have stagnated in the last 12 months, the Licensee Owners List 2020 reveals.

Industry funds – sometimes touted as the great hope to get advice to a broader number of Australians, but other times touted as problematic for their potential structural conflicts as well as awkward governance fit – have seen their efforts to build advice networks stall against the backdrop of a shrinking advice industry.

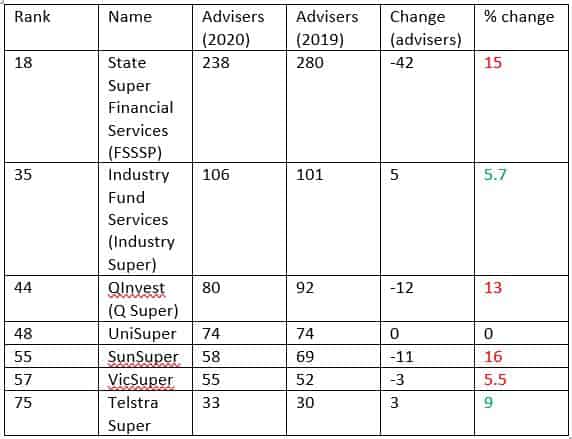

At the top of the list of largest industry fund-owned advice networks is First State Super’s advice network, which has lost 15 per cent of its advisers in the last 12 months. This follows the $1.1 billion deal three years ago for StatePlus, a financial planning asset the Australian Financial Review has since revealed has been written down by $400 million.

Less talked about in the coverage of the Fist State Super deal was the governance concerns that lay beneath this type of structure in which member funds are used to acquire services that are then provided back to members.

This point was highlighted by Tony Lally, former SunSuper CEO and current chair of Equity Trustees Superannuation’s board, when he noted that while the use of members’ retirement funds to acquire or invest in businesses which are for the provision of services to members may not breach the members best interests test, it is questionable under good governance. He noted this in response to an article on the StatePlus asset write down.

“When the members are both the owners and customers of a service an obvious conflict arises,” Lalley noted.

Aside from First State Super, other industry funds with existing inhouse advice businesses have continued to maintain and in most cases seen a reduction in adviser numbers, with UniSuper and Industry Fund Services holding ground.

UniSuper provided a look inside its intra-fund advice model in March, which led to a series of comments from advisers raising an issue with conflicts of interest in a post Hayne and post FASEA Code of Ethics world.

‘Intra-fund’ refers to the type of advice a superannuation trustee can provide to members where the cost of the advice is borne by all members, but it excludes personal advice and a series of other advice scenarios as outlined in the SIS act.

Intra-fund advice became a contentious area for many advisers, particularly in light of Hayne’s recommendations and Treasurer Josh Frydenberg’s subsequent plan to ban the deduction of any fee from a MySuper account other than for intra fund advice.

The industry’s practice of deducting fees from super as part of the broader fee-for-no-service scandal highlighted by Hayne has brought into sharp focus the rules around intra-fund advice outlined in section 99F of the Superannuation Industry (Supervision) Act 1993 and the subsequent ASIC regulatory guidance relating to intra-fund advice.

Industry funds either tend to offer their products on recommended lists and within the mix of model portfolios through the broader independent financial adviser market – such as Australian Super and other funds, which are experiencing strong inflows from advisers – or the focus their products on their own membership through digital portholes and salaried-advice channels.

Leave a Comment

You must be logged in to post a comment.