Superannuants riding the gravy train of strong returns and taking more than the mandated minimum from their fund during the decade-long bull market will need to check their habits in the event of a market correction, warns HLB Mann Judd wealth management partner Jonathan Philpot.

If the market takes a serious and sustained downturn, the government may even repeat its post-GFC contingency measure and temporarily reduce the minimums, he says.

The wealth manager isn’t predicting another global financial crisis. Philpot expects equity returns to pull back from their record-breaking 2019 highs to “7 or 8 per cent” over the next five years, while low-risk investments will max out at 3 per cent due to a persistently low-rate environment.

But even this moderate correction will have a noticeable impact on portfolios. For a typical ‘balanced’ investor with a 70/30 profile, it would mean a sharp reversion from a return of between 10 and 20 per cent to a much more modest 5.5 per cent to 6.5 per cent.

“For retirees drawing out their minimum 5 per cent who wants to have their earnings match what they’re drawing out, 5 or 6 per cent is OK and they’re meeting their goals,” Philpot says.

“But if they’ve been drawing down at 8 to ten per cent rate over the last few years, largely because returns have been good and they feel a little bit wealthier… they’re going to struggle in this sort of environment if they still wish to preserve what they’ve got in super.”

Cutting back on income, however, often involves sacrifices for retirees. Philpot reckons a reduction in holiday travel will be the change to spending patterns that advisers will most commonly see.

“Most people’s living costs are pretty consistent, but I find it’s more the holidays [that change],” he explains. “One year they need $30,000 because they’re going to Europe, the next year they aren’t travelling and that could be because there’s been a 10 per cent pullback in the market.”

As an alternative, Philpot says superannuants could take on more risk and dial back the 30 per cent of their portfolio that is wedded to low-rate returns. The client would need the right disposition, however, to cope with volatility in the market – especially in the event of a significant downturn.

“While a 15 per cent short-term market correction on a higher proportion of an investor’s portfolio may be a difficult pill to swallow… it may be necessary to achieve a longer lasting superannuation balance,” he says.

In the event of a serious and sustained correction similar to the 2008 GFC, Philpot reckons the government could once again give pensioners a reprieve on minimum payments and ease the drain on superannuation balances.

“They’ve done it before,” he says. ‘I don’t see why they wouldn’t consider it again.”

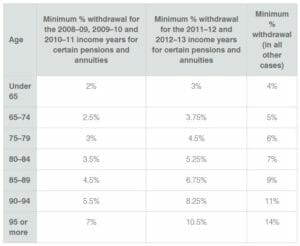

In the wake of the GFC – which saw the benchmark ASX200 lose 16 per cent in one week – the Rudd government halved account-based pension minimum payments for 2008/09, 2009/10 and 2010/11, and reduced them by 25 per cent for 2011/12 and 2012/13.

“It did work,” Philpot says. “In real dark periods people become very cautious and try and preserve what they’ve got.”

Leave a Comment

You must be logged in to post a comment.