Specialised insurance advisers are becoming increasingly rare, with the number of ‘risk specialists’ dropping from 34 per cent five years ago to just 15 per cent today according to recent data from researcher Investment Trends.

The decline of risk specialists – defined as those who derive over 50 per cent of their total practice revenue from providing risk advice – is being attributed primarily to remuneration erosion and the mounting compliance burden.

The squeeze on remuneration started with the 2017 Life Insurance Framework (LIF) laws, which capped upfront commissions at 60 per cent and ongoing commissions at 20 per cent. This was compounded when Hayne delivered his royal commission recommendation that ASIC should consider further reducing the cap on life insurance commissions.

“Unless there is a clear justification for retaining those commissions, the cap should ultimately be reduced to zero,” Hayne stated.

After the federal government promised to enact all of Hayne’s recommendations, finance minister Mathias Cormann told attendees at the Professional Planner Risk Summit in September it was willing to wait and see how the LIF reforms played out before letting ASIC check those reforms have been “bedded down” in its government-mandated 2021 review. At that stage, he said, “further adjustments” may be required.

“The admin burden of compliance and paperwork, coupled with an uncertain regulatory landscape, are the top challenges that prevent financial planners from growing their insurance advice,” says Investment Trends’ Senior Analyst, King Choi. “As more planners seek to diversify their advice proposition and focus more on holistic advice, the risk specialist planner has become an industry niche.”

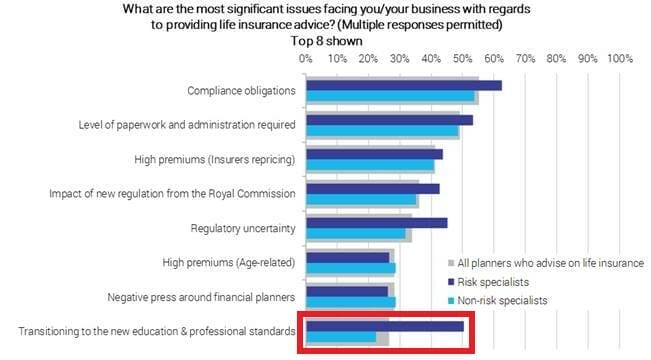

Risk specialists must also meet the same set of education standards as holistic financial advisers, which puts them at a disadvantage. More than twice as many risk specialists as non-risk specialists cited “transitioning to the new education and professional standards” as one of the most significant issues with providing insurance advice, according to Investment Trends (see below).

Abandon ship

Abandon ship

Another headwind for insurance advisers – again stemming from a Hayne royal commission recommendation – is possible legislation that will require advice practices that provide insurance advice to actively disclose to clients that they accept conflicted remuneration, or in Hayne’s words to explain “simply and concisely why the adviser is not independent, impartial and unbiased”.

Currently, advice practices are only required under section 923A of the Corporations Act (2001) to refrain from using the terms independent, impartial and unbiased. To force even holistic advice providers to call essentially call themselves conflicted may result in large swathes of full-service advice providers abandon holistic practice in favour of scaled advice sans insurance.

According to Daniel Brammall, president of the Profession of Independent Financial Advisers (PIFA), advisers reconsidering insurance advice in light of the incoming legislation is “to be entirely expected”.

Kris Mason, a Partner at MBS Insurance, says the trend of advisers abandoning the insurance space has already started.

“A lot of them will want to get out of the insurance space to keep that clean model,” Mason says. “Post royal commission, they’re sticking to fundamental financial planning and not doing the peripheral financial services.”

Leave a Comment

You must be logged in to post a comment.