Over the next 25 years, as the Baby Boomer generation transitions into retirement, CoreData estimates that $3.9 trillion of wealth will be transferred into the hands of younger generations.

It’s a transfer of wealth unprecedented in the history of mankind. And perhaps for that very reason, those set to inherit this wealth are likely to generate unprecedented demand for financial advice services.

But lest the financial advice profession becomes complacent in the face of this boom, it’s worth noting that for the foreseeable future, at least, customers won’t just walk through the doors of advice firms looking for help. There remains a level of mistrust and apprehension about the motivation and professionalism of financial advice that consumers have yet to overcome.

Advisers will still need to win business by demonstrating value, conducting themselves professionally and proving they are worthy of trust and respect. But for those that succeed, and who navigate the next four-and-a-bit years through new education, professional and ethical standards, the future looks very bright indeed.

As the industry adjusts to new standards and while customer demand for advice at the very least holds up, new models of advice will need to develop to support the delivery of services in a professional and client-focused way. There is unlikely to be a single new model of advice that emerges – our analysis of the market suggests there will be a number of basic versions of advice business structures, with variations around those themes.

As the industry adjusts to new standards and while customer demand for advice at the very least holds up, new models of advice will need to develop to support the delivery of services in a professional and client-focused way. There is unlikely to be a single new model of advice that emerges – our analysis of the market suggests there will be a number of basic versions of advice business structures, with variations around those themes.

The ultimate structure of any businesses will reflect the nature of the services it offers, and the profile of the clients it serves, but be built on the delivery of transparent, professional services. And the structures will need to be built so that advice can be priced and delivered to reflect the value that clients perceive in the services they receive.

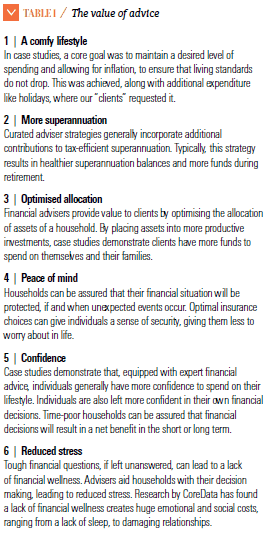

Individuals who seek competent and professional advice, and who act on it, can be shown to be happier and wealthier. CoreData has undertaken numerous studies – a combination of case studies and quantitative research – that show the benefits of advice extend well beyond financial issues (see table 1).

It’s worth noting that only two of the benefits listed above are strictly financial: optimised asset allocation, and more money in superannuation/retirement. The others address non-financial issues, ranging from lifestyle to peace of mind, reduced stress and greater confidence.

But non-financial issues are difficult to quantify and difficult to measure. It’s easy to calculate an increase in the value of a portfolio over a given period of time, but on what scale do you measure peace of mind?

It is understandable why advisers have in the past tended to focus on something that can be measured accurately and reliably when charging for services: assets under management. As well as being simple, it also demonstrates the adviser has skin in the game.

A financial advice community conditioned to charge for its services based on things that can be very accurately measured might struggle to adjust to asking people to pay for something that can’t be measured in the same way, or with the same degree of certainty. But that’s what the future of financial advice looks like. It’s less about how much an adviser helps an individual’s wealth or a family’s wealth to increase from one point in time to another, and more about how the professional guidance and expertise of the adviser support the individual or family in doing or achieving the things that really matter to them.

Sure, for some people, just getting wealthier is all that matters. But for most people, and for the kind of clients that sustainable and professional financial advice practices can be built around, the value of advice is in helping them achieve their goals and the non-financial benefits of advice alongside the financial benefits.

Sure, for some people, just getting wealthier is all that matters. But for most people, and for the kind of clients that sustainable and professional financial advice practices can be built around, the value of advice is in helping them achieve their goals and the non-financial benefits of advice alongside the financial benefits.

FUTURE SUCCESS STATES

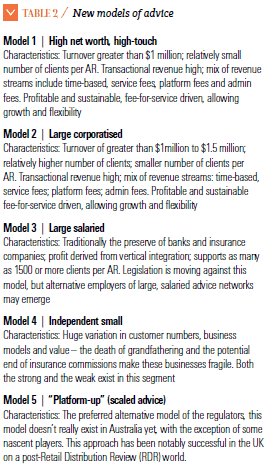

CoreData’s ongoing new model advice research suggests there will be a number of basic advice models that emerge to empower advisers to serve the best interests of clients, depending on the nature of the advice those clients seek. Some look somewhat like the models of today, with the caveat that they must all accommodate the new world of professional, ethical and education standards, and new legislation – notably emerging from the government’s responses to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (see table 2).

New models of advice will also evolve as growing numbers of financial advisers leave institutionally branded licensees and strike out into new territory. CoreData’s 2019 Licensee Research has uncovered a high level of dissatisfaction among advisers authorised by institutionally branded licensees, along with a heightened propensity to leave institutions and find new homes. As these advisers consider their options, new approaches to delivering advice will be developed, along with the business structures necessary to support them. At the end of the day, that’s unequivocally good news for consumers, as advice becomes more client-focused, and delivered in a recognisably professional way.

Leave a Comment

You must be logged in to post a comment.