Commissioner Kenneth Hayne stopped short of recommending advice be pulled from the country’s largest financial institutions, but the reforms he suggested in his final report will aim to continue the change that’s already been forced on the wealth industry.

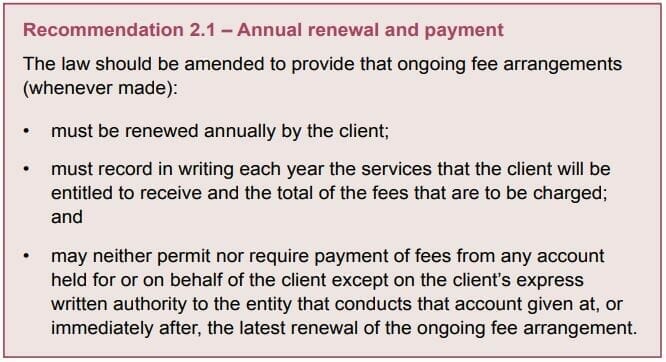

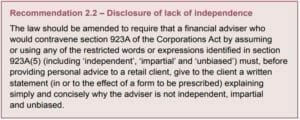

Hayne has recommended new rules be put in place to give clients the upper hand in their relationship with advisers, both in terms of the fee arrangements they enter into and the disclosures they receive.

He also put regulators on notice to hold institutions and individuals to account and has suggested another review in three years (no later than December 2022) to ensure the new rules take hold.

Hayne has decided not to remove the ‘safe harbour’ provision – a carve out from the best-interests duty under the Future of Financial Advice legislation – but he has suggested it be repealed in three years if a review at that time finds conflicts within the advice industry have been allowed to fester.

Specifically, Hayne has recommended responsibility for renewing agreements be put into the hands of clients, not advice or investment firms – a recommendation the final report outlines in depth.

Also, when it comes to disclosure, advisers will need to outline more simply and succinctly where their conflicts of interests lie.

Overall, Hayne has used the final report to amplify his findings from the interim report that financial advice has fallen short of being able to call itself a profession.

“The industry has moved from scandal to scandal, causing financial harm to clients, and damaging public confidence in the value of financial advice. This cannot continue,” he noted.

Hayne’s final recommendations focused on solving three main issues identified during the almost 70 days of hearings and through more than 10,000 written submissions.

The first was “fees for no service”, specifically the charging of ongoing advice fees when no advice was given. The second is that clients have often been given poor advice that has left them worse off than they would have been if proper advice had been given and the third is the fragmented and ineffective disciplinary system for financial advisers.

“…I do not believe that the practice of giving financial advice is yet a profession. The general weight of the evidence given to the Commission by those involved in the industry was to the same effect. Some said it is on the cusp, others were, perhaps, more cautious,” he said.

Vertical integration: the heart of the issue

Hayne spent much time in his final recommendations dissecting and critiquing the institutionally owned advice business model. He noted the acquisition path the big four banks and AMP went on following the Wallis Inquiry and the birth of the “one stop shop” model, in which institutions aimed to leverage client relationships developed by financial advisers to sell products that spanned the company’s vertical business silos.

Throughout the various reforms, Hayne noted, conflicts of interest between adviser and client were permitted to remain, and some forms of conflicted remuneration were, and still are, allowed to continue.

“Both of those compromises lie at the heart of the issue,” he noted.

Hayne stopped short of recommending product providers be forced to offload their wealth businesses, but he suggested that amendments already made to product design and distribution laws, along with the new intervention and enforcement powers given to the regulator, should go a long way towards ending conflicted advice practices.

“Treasury Laws Amendment (Design and Distribution Obligations and Product Intervention Powers) Bill 2018…if enacted, would introduce design and distribution obligations intended to promote the provision of suitable financial products to consumers of those products,” he stated.

Regarding ASIC’s new product intervention power, he explained: “ASIC could make an order that a person must not engage in specified conduct in relation to a product where ASIC perceives a risk of significant consumer detriment.

[Under this power] ASIC would also be able to ban aspects of remuneration practices where there is a direct link between remuneration and distribution of the product,” he stated.

Force and purpose

Hayne also spent a lot of time in his final report noting changes the industry had already undertaken since the investigation kicked off.

“Between them, AMP, ANZ, CBA, NAB and Westpac will pay customers of their advice licensees or their superannuation funds compensation totalling $850 million, or more, for taking money as payment for services that were not provided,” Hayne noted. “Until this Commission was established, ASIC and the relevant entities approached the fees-for-no-service conduct as if it called, at most, for the entity to repay what it had taken, together with some compensation for the client not having had the use of the money. That is, the conduct was treated as if it was no more than a series of inadvertent slips brought about by some want of care in record-keeping.

“It is necessary to keep steadily in mind that entities took money (a lot of money) from their customers for nothing. The conduct was so widespread that seeing it as no more than careless must be challenged.”

Consistent with the findings outlined in his interim report, Hayne’s final recommendations proposed that existing laws be applied more forcefully and purposefully, rather than suggesting wholesale changes.

Leave a Comment

You must be logged in to post a comment.