Advisers see the increasing cost of compliance and the incoming education standards as the most significant risks to their business and barriers to future growth, a study has found.

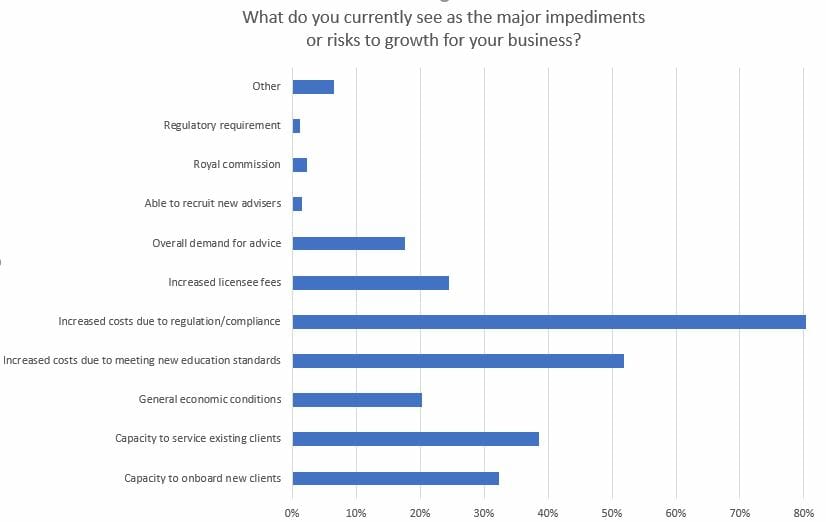

In a survey conducted by researcher CoreData, 80.2 per cent of advisers said “increased costs due to regulation/compliance” was a major impediment or risk to growth for their business.

Along with the compliance burden, more than half (51.8 per cent) said the costs of upskilling to meet new education standards prescribed by the government and administered by the Financial Adviser Standards and Ethics Authority are a major risk.

The Royal Commission into Misconduct in the Banking, Superannuation and Finance Industry, isn’t perceived as being such a danger by the survey’s participants. Only 2.4 per cent of advice businesses reported that the inquiry’s recommendations are likely to be a major impediment to growth.

The research found that while advisers overwhelmingly believe external factors pose the greatest threats to the growth of financial planning businesses, internal issues are also a factor. Onboarding new clients and the capacity to service existing clients are perceived as hurdles by 32.3 per cent and 38.6 per cent of practices, respectively.

Unlocked potential

Managing inflows in terms of new and existing clients is clearly a key determinant for business growth. Three-quarters of businesses (75.1 per cent) said growth would come from onboarding new clients and more than half (53.3 per cent) said growth would come from providing additional services to existing clients.

CoreData head of market insight Simon Hoyle, former editor of Professional Planner, said there was a widespread belief in the industry that technology would unlock potential for growth.

“About 45 per cent (44.9 per cent) of respondents believe growth will be achieved through efficiencies in the advice process brought about by fintech,” Hoyle said. “Removing bottlenecks to onboarding new clients will unshackle some firms, but the capacity to service existing clients – and avoid a fee-for-no-service scenario – is likely to remain an issue.”

While the findings indicate that advisers don’t see the royal commission’s impending recommendations as a serious impediment to growth, Hoyle said the commission would probably address subsidisation of advice from other places in the wealth management chain – principally product and platform – in its recommendations. The effect of this, he said, could be felt through commercial arrangements with licensees.

“Advisers may face an increase in the fees they’re asked to pay to licensees, as licensees seek to recoup costs directly from advisers,” Hoyle explained, “or in some cases may propose to recoup costs directly from clients.”

A sizeable chunk of advisers – 24.6 per cent – believed higher licensee fees would impede their growth, Hoyle noted.

Any increase in licensee fees would need to be offset by a corresponding uplift in services provided, Hoyle said, particularly in areas such as technology.

“Licensees can best help advice businesses grow in the future by adopting a clear strategy for assessing and investing in new technology, to [help advice businesses reduce] compliance costs and get better at onboarding new clients and serving existing clients.”

Hoyle said advisers would also be looking to licensees for assistance in navigating the incoming adviser education standards.

“Licensees can also provide meaningful support by guiding individual advisers through the qualifications upskilling process, as outlined by FASEA, and by facilitating access to (and/or funding) the necessary courses and educational materials,” he explained. “The imposts to advice businesses exist both as direct costs and as indirect costs, through diversion of advisers’ time to non-business-related activities.”

Leave a Comment

You must be logged in to post a comment.