Could we be witnessing the gradual disintegration of vertical integration and the emergence of a new style of licensee owner? Tahn Sharpe delves into ASIC’s latest registry of licensees and their owners.

The movement of advisers from the most prominent and well-known licensee brands to start-up and lesser-known licensee owners started well before the revelations from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, but the events of recent weeks and months will probably further this trend.

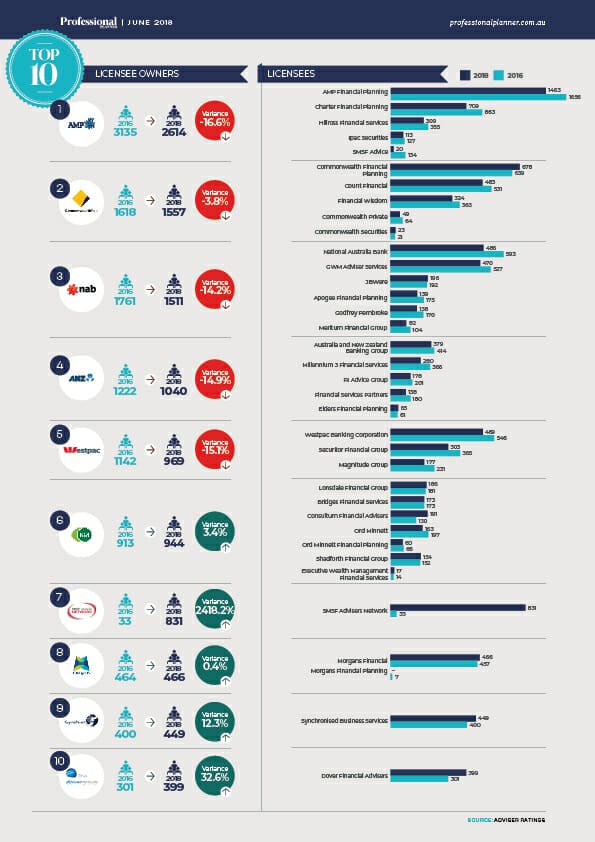

ASIC data compiled by Adviser Ratings shows the country’s five largest licensee owners, based on adviser numbers, have shrunk by an average of almost 13 per cent since 2016.

Meanwhile, the next tier of licensee owners has begun to cement a position among the top 10; that includes the scaled-back SMSF Advisers Network (SAN). It also counts Dover, which has grown in adviser numbers by more than 30 per cent despite well-documented troubles.[k_vc_modal modal_on=”image” btn_img=”62180″ modal_size=”block” overlay_bg_opacity=”80″ img_size=”80″] [/k_vc_modal]Download PDF*Please note: these figures were updated at 10.20am, May 11, 2018.

[/k_vc_modal]Download PDF*Please note: these figures were updated at 10.20am, May 11, 2018.

While there are some long-established names such as IOOF Holdings within the top 10 licensees, many of the fast risers in this second tier are designing their offerings specifically to appeal to advisers looking for alternatives to big-branded dealer groups.

IOOF, the leader of the second tier, will become the second-largest licensee owner in the country when its recent acquisition of ANZ Bank’s wealth-management business is enacted. Its adviser numbers will swell from under 1000 to more than 1600. It will have its challenges managing exponential growth through acquisition.

Nevertheless, IOOF represents the new order and the timing of the ANZ Wealth acquisition gives it an opportunity to herald a fresh era of accountability at the top end. A full analysis of the tectonic shifts in the licensee landscape will be published in the upcoming print issue of Professional Planner in mid-May.

The owners trailing the big five are a diverse collection of bulky dealer groups, opportunistic new entrants and smaller success stories.

Meteoric rise

SAN is the biggest mover in the top 10 by a considerable margin. Its network has increased from 33 to 831 advisers. SAN is owned by the National Tax and Accountants’ Association (NTAA). It provides limited licensing provisions to accountants who still want to give SMSF-related advice following the repeal of the accountants’ exemption in 2016. Geoff Boxer, chief executive of NTAA and director of SAN, says it’s just a matter of reacting to regulatory change at the right time.

SAN provides a scaled, easy alternative to self-licensing for accountants who didn’t see financial advice as their core offering. It is a different breed of licensee and an outlier in many ways. But its pared-down model works because that is all its advisers need. It is also affordable, employing what Boxer calls a “very flat fee structure”.

Scrolling down the list of licensees, growth is apparent throughout the second tier. Morgans Financial, Synchron and Dover round out the top 10, and all are growing.

The rest of the middle tier is jostling to fill the vacuum the banks’ retreat is leaving.

The new era of self-licensing

The ascendancy of the self-licensing model is just as stark as the top end’s decline. There are 507 self-licensed entities that did not exist 22 months ago, and 488 of those have fewer than 10 registered advisers. The average number of advisers in this group is 2.79, and 258 of them operate as a sole adviser.

While the self-licensing route has traditionally been seen as arduous, advisers are increasingly willing to undergo ASIC’s vetting process.

Damien Burns, founder of D&M Financial Services, says vested interests are happy for advisers to overestimate the difficulty of the process.

“There is a myth that it’s very difficult to become self-licensed, and that is what the larger institutions are happy for people to believe,” Burns says. “But it’s not the case.”

Burns received his own Australian Financial Services licence in April 2017, and encourages other planners to do the same.

“It’s not too hard and not too costly,” he says.

Vale vertical integration?

The primary scapegoat for the exodus is the proliferation of flawed vertical integration models. The conflict is clear: pay advisers more for recommending internal products and the incentive naturally shifts away from the client’s best interests. This dynamic has grated against both advisers’ better intentions and the Future of Financial Advice reforms.

The issue was exacerbated in January when ASIC published a report on vertically integrated institutions and conflicts of interest at the big five. The study shows that while advice licensees’ product lists comprise 21 per cent of in-house products, 68 per cent of customers’ money was invested in them.

The results alone weren’t a damning indictment of vertical integration. If licensee owners can obtain better deals on the proprietary products, adviser recommendations will naturally skew towards them. The practice has shades of grey; while egregious conflicts of interest are easy to spot, most require a nuanced assessment.

Rhiannon Kanoniuk, director of newly self-licensed planning firm Pekada, says that despite moving away from the institutional side – the firm was previously licensed under AMP’s Charter Financial Planning Group – she appreciates the benefits of vertical integration.

“Some firms are doing it well by passing on the benefits to consumers,” Kanoniuk says. “You may have a preferred wrap that fits 90 per cent of your clients because it’s an excellent product or you may have the ability to leverage scale to negotiate better fees.”

She also says that if a movement to abolish the practice were to take hold, implementation would be problematic.

“It’s a pretty complex thing to unwind because there are going to be flow-on effects to the consumer, and it’s going to stop people getting advice,” Kanoniuk says.

Reality check

Ian Knox, co-founder and managing director of Paragem Dealer Services, agrees that abandoning vertical integration is not the answer.

“I think we’re going backwards if we eliminate it entirely,” Knox says. “On the global stage, that is an unproven formula.”

Vertical integration also shouldn’t be associated only with the big five, he asserts. Mid-sized firms that recommend their in-house accounting teams are vertically integrating, as are smaller firms that recommend a managed account platform provider and subsequently charge an attendant fee. These practices permeate the industry and are all valid if they remain in the clients’ best interests. Independent firms, he warns, may back themselves into a corner by castigating the institutional side.

“If the advice industry is to criticise vertical integration in the banking system, the independent financial advice movement needs to be sure that it doesn’t vertically integrate,” Knox says.

Still, the ubiquitous nature of vertical integration doesn’t negate the likelihood that the big five are abusing it. The revelations coming out of the royal commission are deplorable, and the institutions no longer deserve the benefit of a doubt. However, the problem is mismanagement of vertical integration, not the practice itself.

“It is not the advice industry, per se, that has created reputational damage for the banks,” he argues. “It is poor management of the advice sector that has created that.”

Leave a Comment

You must be logged in to post a comment.