When the first draft of the Future of Financial Advice (FoFA) legislation was released what seems like a lifetime ago now, in 2011, when Bill Shorten was still Minister for Financial Services and Superannuation – it came as a shock to many Australians that financial planners were not already required to put their clients’ interests ahead of their own.

It spoke to a perceived lack of care and focus regarding clients in the industry that a best-interests duty had to be codified in law.

Last month, the Financial Adviser Standards and Ethics Authority (FASEA) released the first-ever industry-wide code of ethics. It may come as just as big a shock to many Australians that behaving ethically is still optional for financial advisers. Complying with a code of ethics is truly required only if it’s a condition of association membership.

Plenty of associations have no ethical requirements for members, and plenty of advisers are members of those associations (and only those associations). And the FASEA-developed code does not come into force until January 1, 2020, anyway, which means ethics remain optional for segments of the industry for another 21 months.

The game-changer

While advisers have been preoccupied recently with what might or might not be required of them in terms of educational qualifications, bridging courses and recognised prior learning (RPL), FASEA’s single, industry-wide code of ethics could be the real game-changer, with an impact both wider and deeper than any education standards.

It’s deeper because, leaving continuing professional development (CPD) to one side for a moment, education standards are a one-time thing. Meet the standard and you’re in (or you can stay in). But a code of ethics is for life, and it permeates every aspect of how an adviser thinks and behaves – or at least it should.

And it’s wider because irrespective of where an adviser stands in terms of formal qualifications, from those who have none right through to those who already have an approved degree, FASEA has decreed that they must undertake further study, specifically on ethics.

The standards that define and elevate any profession emerge from a community of practitioners explicitly agreeing to be held to a standard of behaviour and competence that exceeds the minimum requirements of the law. In fact, paragraph 3.5 of the explanatory memorandum to the Corporations Amendment (Professional Standards of Financial Advisers) explicitly states that the code of ethics should operate at a standard that exceeds the law.

Legislation creates only a foundation. It’s what’s built on top of that, which often does not have the force of law at all, that conjures a profession into existence.

The release of FASEA’s proposed code is only a first step. It has yet to be finalised, and before it comes into force, every practising adviser must sign up to a compliance scheme. Advisers not covered by a compliance scheme will be expelled from the industry. Compliance schemes must be overseen by monitoring bodies, which will take action if an adviser breaches the code. This could lead to expulsion in extreme cases.

It’s quite a big job to create a compliance scheme and a monitoring body, and to get the whole lot approved by the Australian Securities and Investments Commission. But that issue is an article for another day.

Get ready for the hot seat

The absence of ethics in financial planning is sure to be painfully revealed as the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry turns its attention to advice this month. If the pummeling meted out to the mortgage broking industry last month is any guide, it will be a torrid couple of weeks for the financial planning community.

It will be a miracle if the industry is not dealt another blow to its reputation. But to gauge any potential impact, we first need to take stock of where the industry and its practitioners stand now.

Research by CoreData before the inquiry got underway found 60 per cent of people said they trust financial advice, as an industry, and think financial planning is “a valuable industry”. A similar proportion, about 58 per cent, said a financial planner could “make an economic difference” to their lives.

The CoreData research shows financial planning ranks behind only superannuation funds (75.2 per cent) and on a par with banks (60.8 per cent) in terms of trust, and ranks a mile ahead of government and the media.

It also found about a quarter (28.4 per cent) of Australians said they had a financial adviser, and about 17 per cent said they used to have one, but don’t anymore. Just less than 60 per cent (58.4 per cent) said they had never had an adviser.

While the research identified specific banks and super funds as the most trusted, there was no single financial advice brand that stood out. This is both a blessing and a curse: while there’s no single organisation that sets the lead, the public also tends to sheet home the shortcomings of financial planning as a collective, rather than directing its displeasure at any single business or brand.

During public hearings last week, the mortgage broking industry relied on claims that lenders’ systems and processes have changed, and on promises that procedures and practices have improved. In some instances, the defences looked particularly flimsy. At least the financial planning industry can point to actual laws designed to raise standards, and at the work beginning to emerge from FASEA, as evidence of changes that will start to address many of the issues of malpractice the inquiry is sure to cover.

It’s a small mercy, but in next month’s public hearings, the financial planning industry may need all the mercy it can get.

Simon Hoyle is head of market insight for CoreData Research.

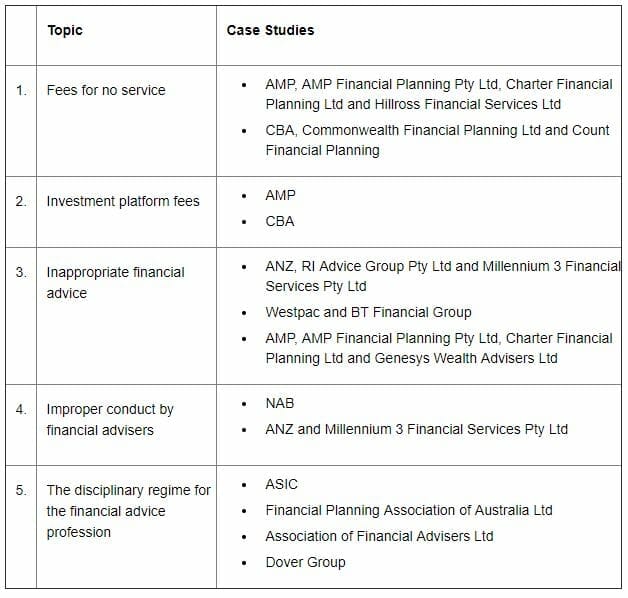

Royal commission advice case studies

Leave a Comment

You must be logged in to post a comment.