Global equity fund managers are bringing more and more new products to the market, as investor demand for global exposure and a range of different strategies continues to grow.

According to Lonsec Research’s recently released Global Equities Sector Review, 172 different global equity products were rated in 2015–16, with 25 new products added since the previous year. Along with the proliferation of new financial products, investors are continuing to benefit from developments such as smart beta, as well as alternative product structures such as Separately Managed Accounts (SMAs), Exchange Traded Funds (ETFs) and unlisted managed funds available through the ASX settlement service (mFunds).

“We have seen significant growth in the number of global equity products over the past year, and this has shown no immediate signs of abating,” said Peter Green, General Manager of Equities. “There are a number of possible drivers of this activity, including attractive past returns from the sector, waning domestic market performance, and a general push for greater portfolio diversification.”

With yields at record lows and economic growth still in recovery mode, investors are finding it harder to meet their return targets. Global equities may be seen as an effective way of boosting portfolio returns, while also achieving a greater degree of diversification.

“Managed funds are still dominating the global equities sector, but a growing number of investors are recognising the benefits of ASX-listed alternatives, and the market has been responding to this demand,” said Green. “Innovations such as smart beta ETFs, which provide systematic exposure to certain style factors, are bringing more transparency to the active equity space, as well as cheaper alternatives for investors.”

Growth shares still on top

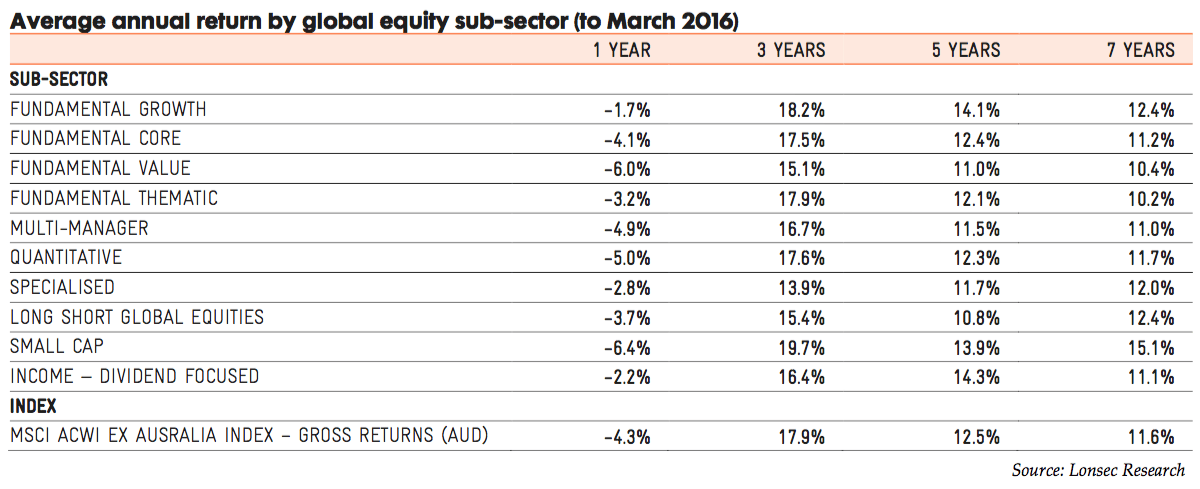

Growth has again proved the best-performing investment style, with Lonsec Research’s Fundamental Growth peer group returning -1.7% over one year, amid a series of significantly negative returns. Growth has also outperformed over longer periods, returning an average of 12.4% per annum over seven years, compared to the average for Fundamental Value products of 10.4%. Fundamental Core products returned -4.1% over one year and 11.2% over seven years, sitting between the growth and value results (see table below).

Quantitative financial products suffered as momentum reversed, returning an average of -5.0% over one year. Notably, on average, the growth peer group also outperformed the more flexible ‘long short global’ set of products over the year, which returned -3.7%. Small cap products delivered weak absolute performance, returning -6.4%, however they remain dominant over three and five years.

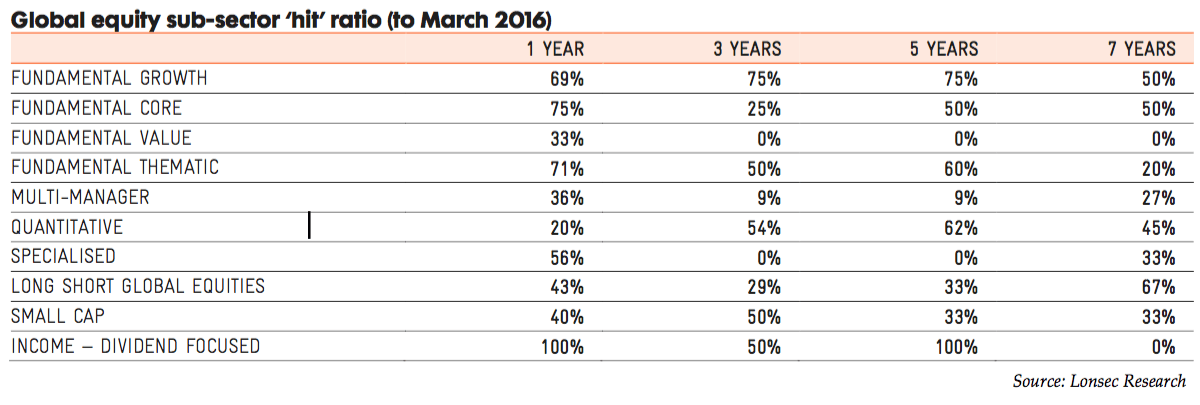

Looking at the proportion of financial products that have outperformed the benchmark, value has been lagging over every period. Only 33% of value products have outperformed over one year, while zero have outperformed over longer periods. In contrast, growth products have a stronger track record, with 69% outperforming over one year, and 50% outperforming over seven years. Multi-Manager products as a group have struggled over all periods. Surprisingly, the ‘hit’ ratio of the more flexible long/short products has been weak (see table below).