Markets have shrugged off fears about slowing Chinese growth, higher US interest rates, and the UK’s vote to excise itself from the European Union, among many others. But sometimes fear presents itself in different ways.

Take the chart below that shows the bubbly median price-to-earnings ratio for the Leuthold 3000 Low Volatility Index. It’s not news that investors are devouring stocks offering stability. You can also see it on a company-by-company basis, or in different industries.

CHART 1

Median price-to-earnings ratio of

Leuthold 3000 Low Volatility Index

Source: Leuthold Group

The average price-to-earnings ratio of four stable food groups, including Hormel Foods, Kellogg Company, Campbell Soup and McCormick & Company is 32x, suggesting revenue and operating profits are growing rapidly. Not so. Their average annual growth in revenue over the past five years has been just 3.3 per cent, with operating profits growing a glacial 1.6 per cent.

Of course you could trade these fast growers of a bygone era for today’s meteoric stars, the FANG stocks, which includes Facebook, Amazon, Netflix and Google (now Alphabet), which trade on average price-to-earnings ratio of 153x. They’ve performed incredibly, but the odds of living up to today’s expectations over the next decade are stacked against them. Everything must go right, including handling the increasing competition between themselves.

So where is the growth?

Despite the common complaint that there’s too little growth, there are many companies and industries that are growing quickly. Outbound Asian (particularly Chinese) tourism is growing exponentially. Broadband usage is growing rapidly as we use more data for entertainment. Online flight and hotel bookings are also stealing market share from traditional travel agents at a rapid clip.

The problem is that the companies that are benefitting from these trends are usually priced accordingly. But for those willing to look outside Australia and prepared to do a bit of old fashioned hard work, there are opportunities to pay value prices for high growth stocks.

Charter Communications is one of the many cable companies that was written off last year as fears spread that more and more customers would ‘cut the cord’ or buy ‘skinny bundles’ to reduce their monthly cable bill in favour of internet options, such as Netflix. In the vernacular of US investor Howard Marks, it was classic first-level thinking.

Upon investigation, we found a company with a rapidly growing broadband business, run by the best chief executive in the industry, Thomas Rutledge, that was about to become the second largest cable company in the US, after acquiring Time Warner Cable and Bright Networks. Rutledge would rapidly cut costs and increase the quality and price of services for Time Warner Cable customers, while picking up more broadband customers wanting faster and higher quality internet services. Better yet, we purchased our shares via Liberty Broadband, a holding company whose primary asset was a shareholding in Charter Communications, giving us an added 12 per cent discount.

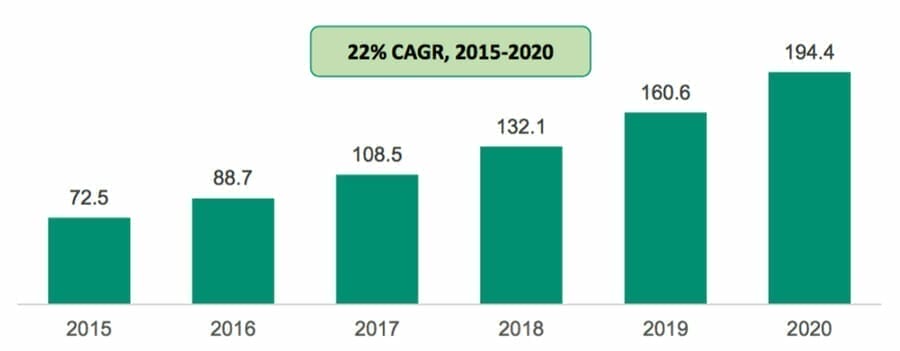

CHART 2

Global IP traffic forecast in Exabytes

per Month 2015-2020

Source: Cisco VNI Global IP Traffic Forecast, 2015–2020

We also recently purchased Liberty Ventures, another holding company with a shareholding in Liberty Broadband and Charter Communications, as well as rapidly growing online hotel and flight bookings company Expedia. Instead of paying full price for these wonderful franchises, we purchased Liberty Ventures at a 21 per cent discount to its net asset value and an almost 40 per cent discount to our estimate of intrinsic value. With ETFs and passive index strategies offering more risk than return at current valuations, these examples show you can buy growth companies without paying extreme price tags.

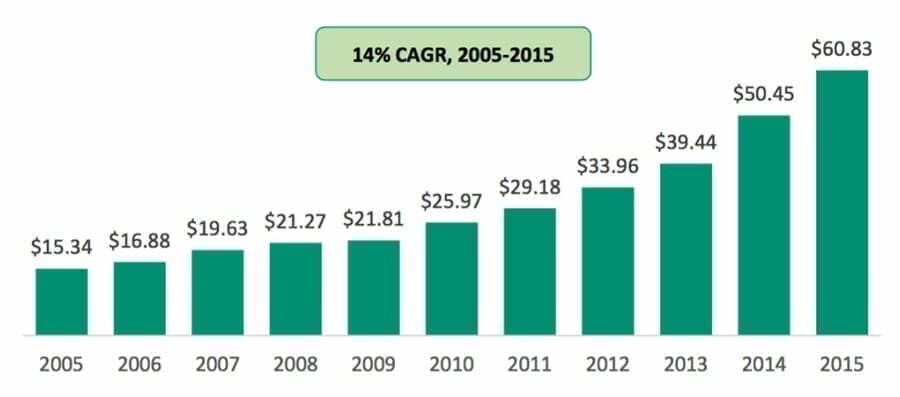

CHART 3

Expedia’s growing gross bookings

($US billions)

Source: Expedia

History says that value stocks have outperformed growth stocks 87 per cent of the time. With growth stocks currently enjoying their second longest winning streak ever, value stocks are reaching their time to shine. The remarkable recent performance of beaten up sectors, such as the resources and gold mining industries, may indicate that the trend has already started.

Buying value stocks doesn’t mean buying low-growth stocks any more than it means buying stocks with low price-to-earnings ratios regardless of their quality. Value simply means buying at a discount to minimise the chance of loss while providing maximum potential for gains. As the examples of Liberty Broadband, Charter Communications, Liberty Ventures and Expedia show, value and growth are not mutually exclusive, they are attached at the hip.