Salary sacrifice to superannuation is an effective way to save for retirement. It allows clients to build savings using pre-tax money. But changes announced in the 2016 federal budget may trigger a rethink from July 1, 2017 (assuming the changes are passed).

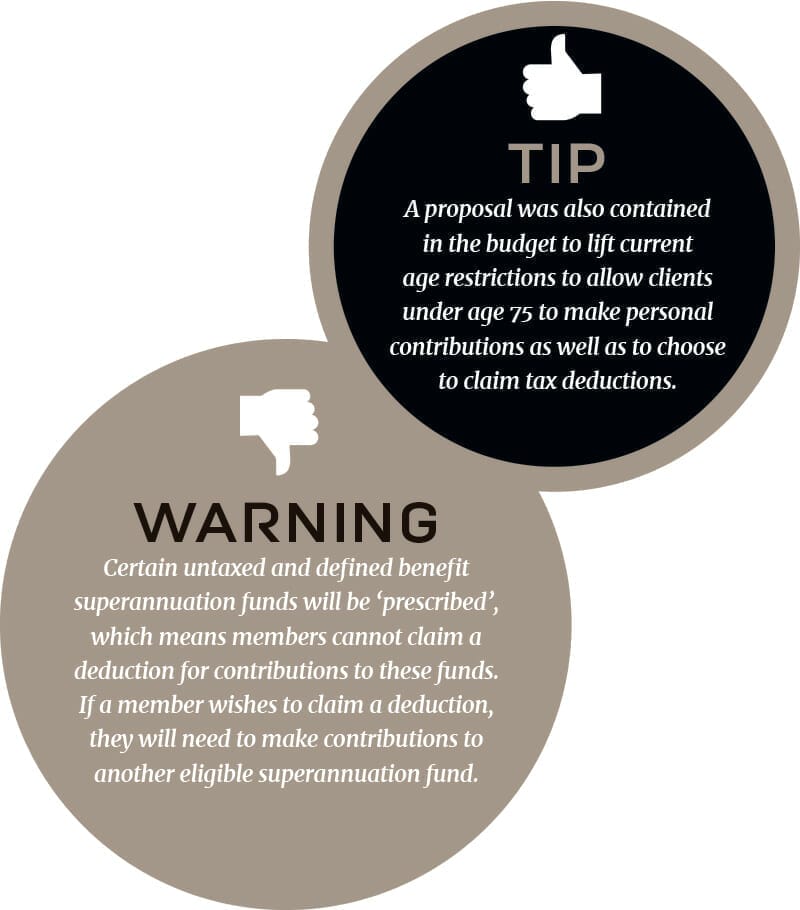

Salary sacrifice will remain an option but the budget proposals will allow everyone under age 75 to make personal contributions and choose to claim a tax deduction, regardless of work status, from July 1, 2017.

Perhaps in the future clients will prefer to make personal deductible contributions instead of arranging salary sacrifice with employers.

The problem with salary sacrifice

Both salary sacrifice and personal deductible contributions provide the same tax advantages and outcomes. The difference lies in who is eligible for

each contribution option.

Under current rules personal deductible contributions can only be claimed by clients who are fully or substantially self-employed (and meet the 10 per cent rule) or not working. So most employees are left with only the option to salary sacrifice through an arrangement with their employer.

The problems with salary sacrifice arise from:

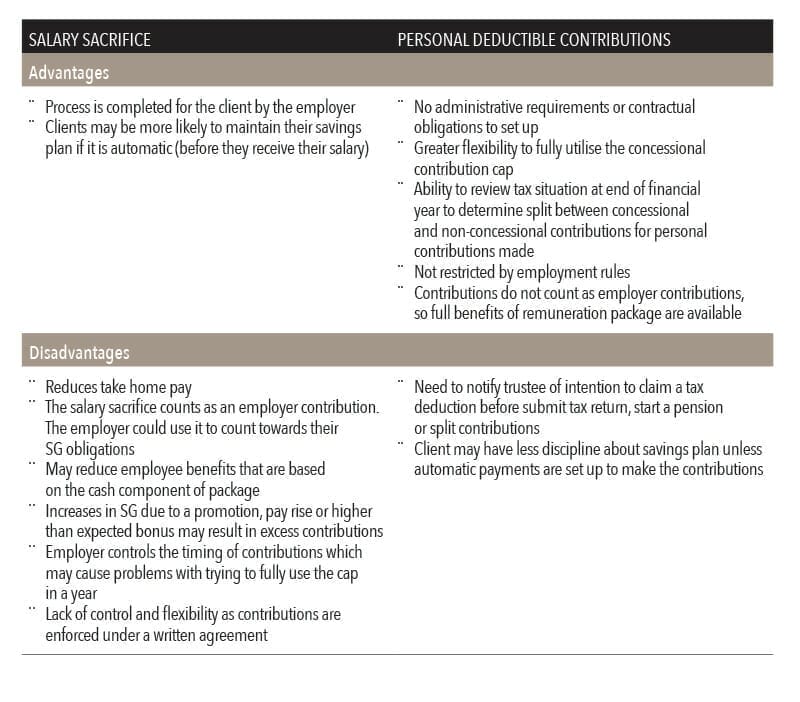

• The need for an effective agreement to be in place before the salary is earned – reduces flexibility and makes it difficult to sacrifice bonuses

• Classification of salary sacrifice as an employer contribution – requires careful structuring of employment packages to ensure the superannuation guarantee (SG) otherwise payable and other employment benefits are not reduced

• Timing and control of the payments is in the hands of the employer – may cause problems with contribution caps or non-payment.

In contrast, making regular personal contributions and choosing whether or not to claim a tax deduction at the end of the financial year may allow clients to make more controlled contributions and provide a greater opportunity to manage the strategy more effectively. It allows the benefit of hindsight.

If the changes are passed, personal deductible contributions may become more appealing than salary sacrifice for many employees.

2016 federal budget proposals

If budget changes are passed, the employment status of individuals will no longer be a factor of whether or not a personal, deductible contribution can be made from July 1, 2017.

This would enable clients to choose to claim an income tax deduction for any personal superannuation contribution, into an eligible superannuation fund up to the concessional contributions cap. These contributions will be subject to 15 per cent contributions tax.

Example

Frederick (salary of $85,000) is age 45 and wants to boost his retirement savings.

He is considering a salary sacrifice arrangement with his employer for 2017/18 but is concerned that by reducing the cash component of his salary he might impact other employment benefits, such as redundancy entitlements.

His cashflow each month is reasonably tight but he is expecting a good bonus later in the year. He is unsure how much this will be, but hopes he can use it to help fund his savings plans.

If he sets up a salary sacrifice arrangement for monthly contributions he needs to plan how much to contribute at the start of the year, taking into account what might change throughout the year, including the receipt of any bonuses which are subject to SG. If he sacrifices the bonus he needs to let his employer know how much to contribute before he knows how much he will receive. This makes it difficult to plan and not exceed the concessional contribution cap.

Assuming the budget proposals are passed, Frederick will have the option to make regular personal contributions or to wait until his bonus is paid and decide how much to contribute. At the end of the year, after reviewing his tax situation, he can choose how much to claim as a tax deduction.

Comparing the options

When making recommendations to clients on which option to choose consider the following comparative advantages and disadvantages.

Mechanics of personal deductible contributions

Clients can make regular or irregular personal contributions to superannuation.

At the end of the financial year (if eligible) they can review the amount contributed and their tax situation to determine how much, if any, to claim as a deduction. This amount must be notified to the superannuation fund trustee using Notice of intent form (NAT 71121). The trustee will provide an acknowledgement back to the client and the deduction can then be claimed in the client’s tax return.

The trustee deducts the 15 per cent contributions tax and the deductible amount becomes a concessional contribution, which is added to the concessional contributions cap.

If a deduction is not claimed for some or all of the contributions, these amounts remain non-concessional contributions.

Some clients may be more likely to follow the savings plan if arrangements are set up each month to have the contribution automatically paid. This could be arranged through the client’s bank or superannuation fund. Some employers’ funds may agree to deduct after-tax contributions from net salary and remit directly to the superannuation fund with SG payments.

To sum up

Firstly, the proposal must be made law. If this occurs, it will be important to schedule reviews with all clients undertaking salary sacrifice arrangements before July 1, 2017.

In some cases, it may be beneficial for clients to cancel their salary sacrifice from July 1, 2017 and set up a regular savings plan with their bank or super fund to have contributions paid directly into their superannuation account as personal contributions, with tax deductions claimed at

the end of year.

All superannuation contribution arrangements should be reviewed to ensure clients do not exceed the reduced contributions caps (the concessional cap is proposed to reduce to $25,000 per year from July 1, 2017).

What to consider

Before deciding on changes to current salary sacrifice arrangements, consider the client’s individual circumstances including:

• Age

• Taxable income (including salary)

• Employer SG contributions for the year

• Implications of the salary sacrifice on employment benefits/packages.