Robo-advice does not work well in complex situations but suits people in their 30s and 40s who are already using the internet to manage their finances and are starting to save serious money toward retirement.

Robos work very well where the investor’s situation is not complex and a person neatly fits into one of several predetermined categories. For example, the small but relatively focused subset of people in their 30s and 40s who are starting to save serious money toward retirement are perfect for robos.

They may have already looked at negative gearing and margin lending to grow their savings but feel disinclined to take on the added risk in both. Having grown up with technology, this group is more likely to adopt web-based financial advice and therefore be the first target market for most robos. The group is reasonably homogenous – the main difference between individuals aged in their 30s and 40s derives from their risk tolerance profile.

Their need for wealth accumulation is great. In an age of reducing government spending on pension programs, Generation Y is increasingly being asked to fund more of its own retirement. With wealth-building strategies essential, some will turn to robo-advisors for financial advice that may well be much cheaper to access than advice offered by a human adviser.

Internet users targeted

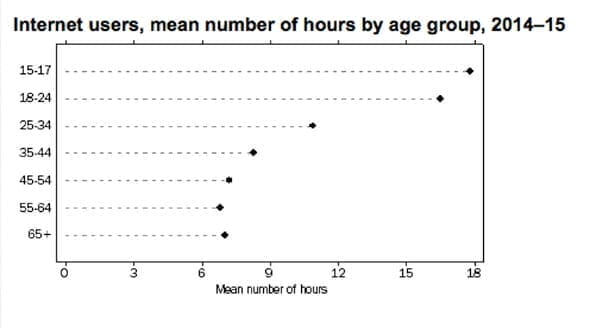

The recently released Australian Bureau of Statistics report, Household Use of Information Technology, Australia, 2014–15 revealed that for those aged 25 to 65 years or over, all reported their most common online activity as banking (along with social networking). So, in fact, most adults are already using the internet to manage their finances. Robo-advisers are taking advantage of this trend and offering the next step – online financial advice and investment transaction facilities.

The ABS report highlighted that internet activity is highest among the younger age groups (people under the age of 35). In 2014–15, 85 per cent of people were internet users. The 15–17 years age group had the highest proportion of internet users (99 per cent), while the oldest age group (65 years and over) had the lowest proportion (51 per cent).

People in this younger cohort could well be the second target for robos as they follow in their parents’ footsteps to manage and build their wealth.

Source: Australian Bureau of Statistics

Robos will differentiate

Currently, we are working with robo-advice version 1.0. It works on narrow, niche sectors. It can’t deal with complexity. But that is changing very quickly. In the US we are starting to hear about robo-advice 2.0 – it is much more able to deal with complexities when they arise. That’s a real game changer.

Soon there will be many “specialist” robos, just as there are specialist doctors. Planning a retirement income? There will be a robo that specialises in that. Want an aggressive equity exposure? There will be a robo that specialises in that. And so on. Robos will not remain generic. Once they specialise, robo-advisers will have applications throughout every level of the industry – in Australia and offshore in the US where they have been more readily adopted. This space is changing rapidly and the technology is being developed as we read.

But to flourish, robos will have to meet the same suitability standards as human advisers. It is unimaginable that an advice business would want the same client getting a different recommendation depending on whether they used robo or human advice. A business built on a multi-factor assessment of risk tolerance, risk capacity and risk needed will, of course, expect those same standards in a robo.

(Continues below.)

[tv playlist=’55a4af5c150ba0e92e8b459c’ theme=’pp_article’]

Like miners needed shovels

Just as every miner in the Californian gold rush needed a shovel, so robo-advisers need smart investment suitability tools – like our risk-tolerance test – to ‘plug-in’ to their algorithms.

Macquarie Group, for example, has taken the lead in Australia and joined forces with FinaMetrica to use its risk profiling software for its new robo-adviser platform, OwnersAdvisory. That new service is intended for “do-it-yourself” investors who want to manage their investments online and are seeking a flat-fee advice service to help them with their decisions – and Macquarie has put suitability of its advice at the core of its platform.

Other robos will also need to act to entrench suitability in their processes. No robo can afford the loss of confidence that may arise if an advisory business makes unsuitable recommendations to its clients. Robos will need to ask at least two essential questions:

1. Have you made suitable enquiries of your client to know enough about them to be able to make a recommendation relevant to their circumstances?

2. Is the recommendation you make suitable?

Without that, robos risk legal claims from dissatisfied clients.