One of the biggest challenges facing Australia’s licensees is to make sure that the financial advisers whom they support run businesses which are completely and demonstrably compliant.

Compliance, to be honest, is both very, very simple and very complicated at the same time.

It’s simple because at its heart is a very simple ethos: make sure that everything that you do benefits the client and ensures the client fully understands what they are investing in.

That’s complicated – mostly because financial planning is complicated and the ideas contained within it are complicated, and because it deals with the future and the future is impossible to predict.

Since 2001 at CoreData we have been running a mystery shopping program. We recruit real customers from our database of mass affluent Australians who are seeking either a new financial planner or to change financial planners, and we watch them go through the process.

We measure a broad range of things, from how easy it is to make the appointment to what the inside of the office where the appointment was held looked like; but one of the most interesting thing we measure is compliance.

Measuring compliance

To measure compliance, we train the mystery shoppers on what they should expect, and we create a questionnaire with a series of hard gateways so that the process of onboarding them as a client becomes visible and measurable. While this questionnaire is broadly similar from year to year, it’s updated regularly to reflect changes in process and changes in the law.

Where the clients allow us – and not all of them do – we also look at what they have paid for their plan, the fees for the services and products, and what products they are placed in, to make a broad assessment of the quality of the plan.

We also contact them every year after the mystery shopping, to determine their satisfaction with the plan, their planner and their intentions.

In the past decade or more of this research, we have seen data on a wide range of activity, from implementing slightly outrageous investment ideas, to the kind of mild laziness of oversight that comes with running a busy practice and managing clients through a complicated purchase process.

This year’s Compliance Bench Marking Mystery Shopping researched 19 practices and involved more than 450 researchers and more than 1200 research events. The data show the very real effect that the compliance focus has had on the advice industry, with the range of scores (the difference between the high and low scores) narrowing to its tightest band ever.

It has been shown that one client can meet up to four planners if they are unsatisfied with the person and the business they meet; however, it’s valuable to know that clients rarely meet more than two planners, and the vast majority of clients do end up starting a relationship with a planner through the process.

In terms of compliance, the top five businesses this year were Westpac Financial Planning, NAB Financial Planning, Securitor and Commonwealth Financial Planning, with a range of less than four points between them. This range is narrow – but it is a useful guide because the sample for each of them was bigger than 100 events.

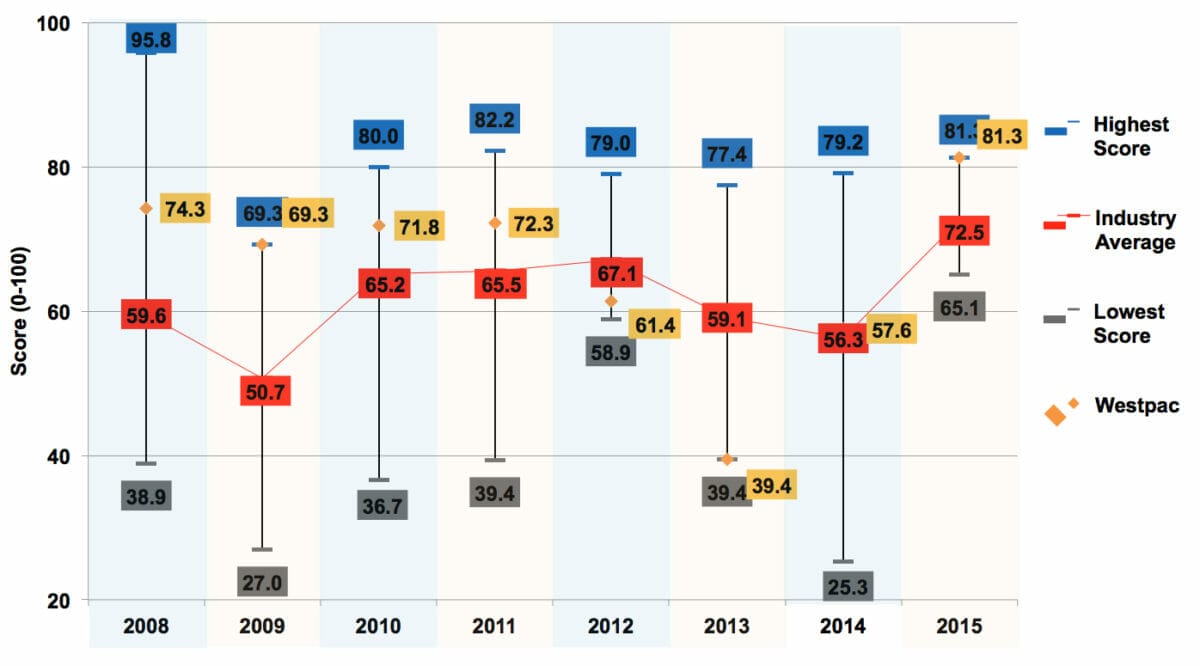

The chart that tells the story

As usual with research, however, it’s the longitudinal chart (left; click to enlarge) which tells the story. It shows the change in both the range of the compliance behaviour and the change in the businesses’ behaviour.

In 2012 and 2013, Westpac was the least compliant advice business in Australia, persistently falling over in the simple legislative areas of the customer onboarding process. By 2014, it was bang on the industry average in terms of compliance. And by 2015 it was the best in the industry.

Digging into what it had done differently in the past three years revealed three core things.

The first is that Westpac has made compliance a complete focus of the business, and has thrown huge resources into it. In doing this it has created a massive shortfall in the market of trained compliance staff, who are now tasked with building processes, reviewing files and spending hundreds and hundreds of hours running education sessions for new and old planners.

Second, it has almost completely systematised the process of compliance, creating a robust framework against which advisers can assess their plans and internal processes, and creating clear escalation points which go to teams that are well resourced and well trained. This has resulted in a new role in the business – the practice advice specialist.

Finally, it is downsizing. Our research shows that there are two businesses doing this better than others: Westpac, and Commonwealth Financial Planning.

While neither business will reveal how many businesses or people have gone, and certainly wouldn’t be drawn on businesses or business names, CoreData research reveals Westpac alone has shed more than 60 planners where they felt the business or the person didn’t meet their standards or share the same goals.