The ideal retirement is a pipe dream for the majority of Australia’s 4.7 million (see note 1) pre-retirees amid rising living costs and retirement income expectations, new research from CoreData has revealed.

CoreData’s 2016 Post-Retirement Report, which examines retirement attitudes and intentions among Australians aged 45 and older, found that pre-retirees expect to need an average of $1,224 a week in today’s dollars (up from $1,124 in 2015 and $1,015 in 2014) and a super balance of $804,559 to maintain their desired lifestyle in retirement.

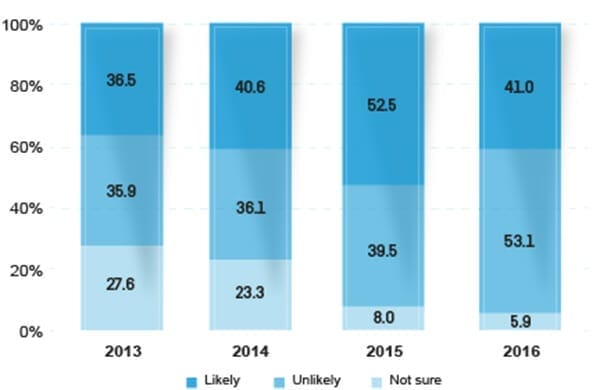

However, the majority (53.1%) think it is unlikely they will achieve this goal, up from 39.5% in 2015 and 36.1% in 2014

To manage the risk that they will outlive their savings and the impact of rising living costs, the vast majority (81.2%) of pre-retirees plan to keep working in some capacity after they retire from full time work.

Kristen Turnbull, Head of WA at CoreData, says the average superannuation balances at retirement of $292,500 for men and $138,150 for women (see note 2) fall well short of the $800,000 balance the average pre-retiree expects they’ll need.

“The reality is that retirees are either going to have to drastically alter their expectations for retirement or start making some serious financial and lifestyle sacrifices now if they have any hope of reaching their financial goals in retirement,” she says.

The rise of the silver surfers

Awareness and understanding of the retirement solutions available remains low among pre-retirees, with less than one in three (31.9%) claiming to have a good understanding of what an annuity can offer and only one in four (27.3%) likely to consider purchasing one in retirement.

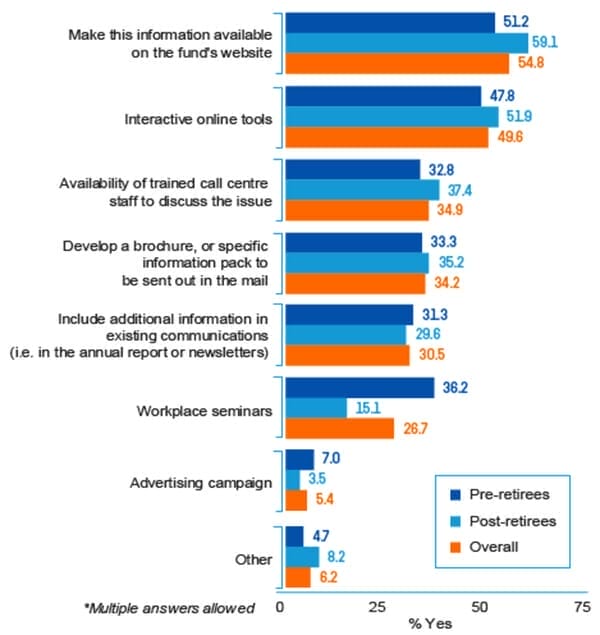

But digital engagement is emerging as a key way in which superannuation funds can educate the over 45s on their options, with the research highlighting strong demand for funds to provide information online.

More than half (54.8%) of pre- and post-retirees would like their main fund to make information available on the fund’s website, up slightly from 52.0% in 2015, while close to half (49.6%) would like their fund to provide interactive online tools, up from 44.5% in 2015.

“Funds that think digital engagement is only for the younger generations need to broaden their mindset,” Turnbull says.

“The rise in ‘silver surfers’ is seeing the older demographic using digital channels more and more as a way to engage with their service providers. The demand for super funds to post out information is falling out of favour with just one third of pre- and post-retirees (34.2%) wanting their fund to increase their awareness and understanding of retirement solutions through mailed out brochures, down from 41.1% in 2015.”

Turnbull says although annuities are not well understood, there is latent demand for the features that an annuity can offer, suggesting education could help improve take-up.

“Poor levels of knowledge and understanding are the more commonly cited barriers to take-up, however reluctance to relinquish control poses another key challenge for annuities providers, particularly at a time when cash rates are at record lows,” she says.

“The two key things that pre-retirees want in managing their retirement savings are a guaranteed income stream and to meet their desired lifestyle, so annuities providers, funds and financial advisers need to find ways to talk to members about the income solutions available in retirement in a language that they understand,” Turnbull says.

Notes:

ABS Catalogue 6238.0 – Retirement and Retirement Intentions, Australia, March 2016

ASFA – Superannuation account balances by age and gender, December 2015