Russell Investments’ 2025 Value of an Adviser index contains an unspoken message for financial advisers who fancy themselves antipodean mini-Buffets: picking investments is not what clients value most..

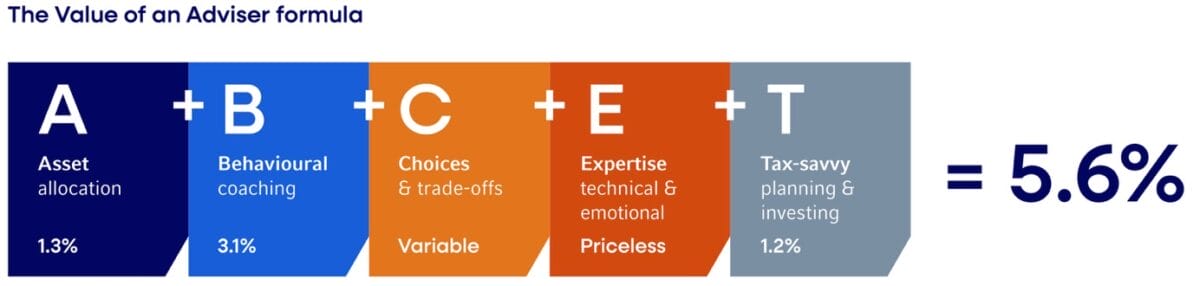

The index, released last week, illustrates the value added by advisers through the various elements that make up a stylised advice process. The 2025 index suggests that advisers could have added as much as 5.6 per cent in additional value to clients in the past year.

By far the greatest value – at least in the 2025 iteration of the index – was added by the work advisers do in “behavioural coaching”, keeping clients on-track and avoiding counterproductive actions such as panic selling the face of an equity market sell-off.

Advisers also add value by helping clients set an appropriate asset allocation, which, many decades after this was first shown to be true, remains the single largest determinant of long-term investment returns.

The least valuable of the quantifiable elements of the Russell index is what it describes as “tax-savvy planning and investing”, which includes selecting the most tax-effective structures for saving and investing.

It’s notable that the index does not attribute value to picking individual stocks or funds or to constructing managed account portfolios.

The Russell research echoes similar work conducted elsewhere, such as Vanguard’s Adviser’s Alpha analysis which, likewise, shows the greatest adviser value-adds are goal setting, determining asset allocation, and behavioural coaching, and relegates stock picking and fund selection to a low-value sideline.

A sceptic might suggest that’s because not many advisers do it consistently well, and that in some years the contribution to the overall index from this activity could be negative – and could conceivably outweigh the contributions of all other elements combined.

Both pieces of research suggest that, except in cases where an adviser clearly has established structures and has the resources, expertise and qualifications to do it very well (or the backing or an organisation that does), they could rethink whether they need to hold themselves out to be investment managers.

There’s a risk to the adviser and practice; it takes a lot of time and expertise, developed over many years; and at the end of the day clients don’t seem to care that much about who does it.

Russell Investments head of distribution for Australia and New Zealand, Neil Rogan, says – although he would, wouldn’t he – that the task of picking investments may be better outsourced, so that advisers can focus on the things they do that clients value most, and at the same time offload some of the risk of doing things that clients don’t value as highly anyway.

“If you look at behavioural coaching, choices and trade-offs, and expertise, they’re going to shift the dial the most in terms of how the client’s going to feel about you,” he tells Professional Planner.

Driven by good intentions

Rogan believes advisers are driven by nothing but good intentions when they decide to take on responsibility for managing clients’ money.

“Most advisers I’ve ever met, at their core, want to help their clients achieve their goals,” he says. “And, in doing that, some advisers choose to build their own models.

“Others may have chosen to outsource the investment management piece to a provider who designed constructs and manages models for them, like ourselves, Lonsec, Zenith, et cetera – there’s a raft of them in the market.”

Rogan says outsourcing investment management doesn’t weaken an adviser’s value proposition; maybe counter-intuitively, it strengthens it.

“There’s a trend more so towards some of the more scaled advice groups taking this approach, which puts guardrails around the investments that they have, the structures that they’re using, and provides them with the degree of comfort that maybe things won’t go wrong,” he says.

He suggests smaller practices, sole practitioners and “others who may not be doing that [yet] consider that kind of approach”.

But when Professional Planner suggests that the index is “one of the most coherent arguments against financial advisers as investment managers”, Rogan says he would “not be as strong as to say that”.

But he says it does support the argument that advisers should focus on where they deliver the most client value, and that the benefits of doing that can flow both ways: advisers could reduce compliance risk and the risk of things going wrong; and clients are placed into professionally constructed portfolios with the scale and manager skill to stand up over time.