Produced in partnership with Betashares.

After US dollar weakness was flagged as a key theme last year, the greenback went on to record its worst first half returns since the 1970s. Policy settings under the Trump administration and the currency’s fundamental overvaluation drove the decline, with the broad trade-weighted US dollar index ending the year down 8 per cent.

However, much of the decline occurred during the first half of the year, especially during the Liberation Day volatility and spent the remainder consolidating. What potentially mitigated the USD’s decline and supported it during the second half was that interest rate differentials remained positive against most other major currencies, combined with a fresh round of yen weakness.

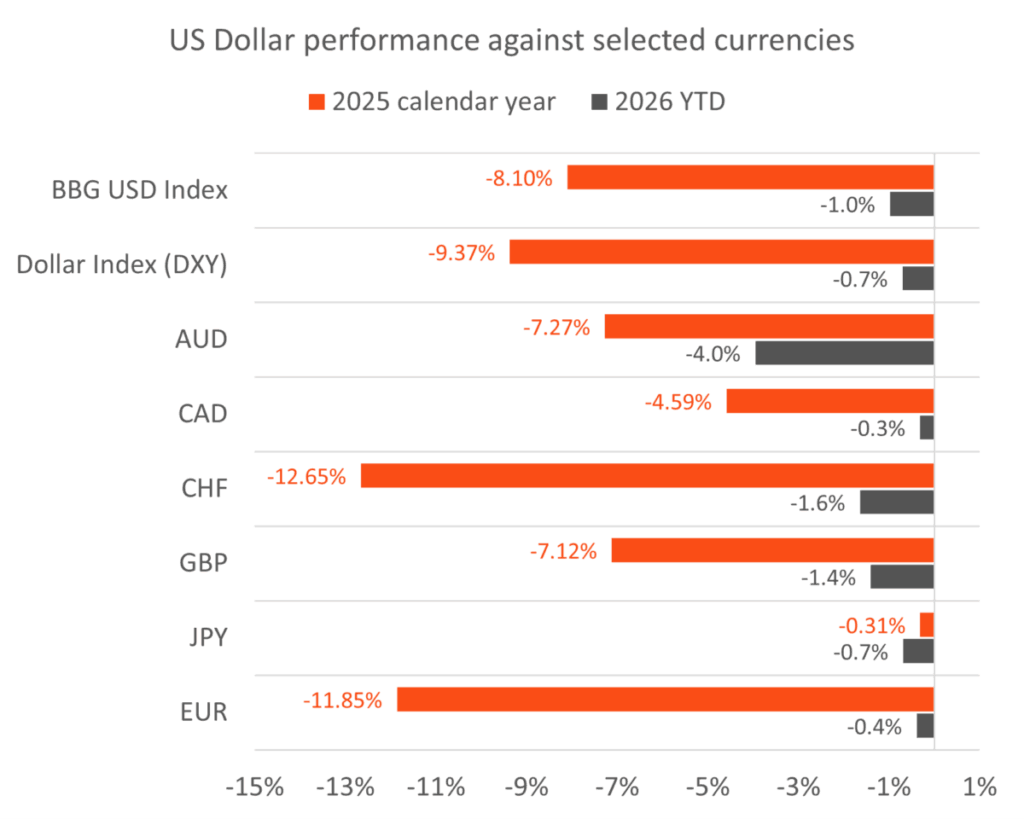

Figure 1: USD performance against selected currencies during 2025 and January 2026

Source: Bloomberg. As at 2 February 2026

That support has faded in early 2026 as the interest rate differential advantage has eroded and US President Trump has injected fresh policy uncertainty.

The Fed has maintained dovish guidance and the US rates market is expecting further cuts, with recent Federal Open Market Committee (FOMC) meetings revealing more concern about labour market weakness than inflation. This dovish tilt stands in stark contrast to central banks elsewhere, including Australia, where sticky inflation has seen markets pricing in a fresh hiking cycle.

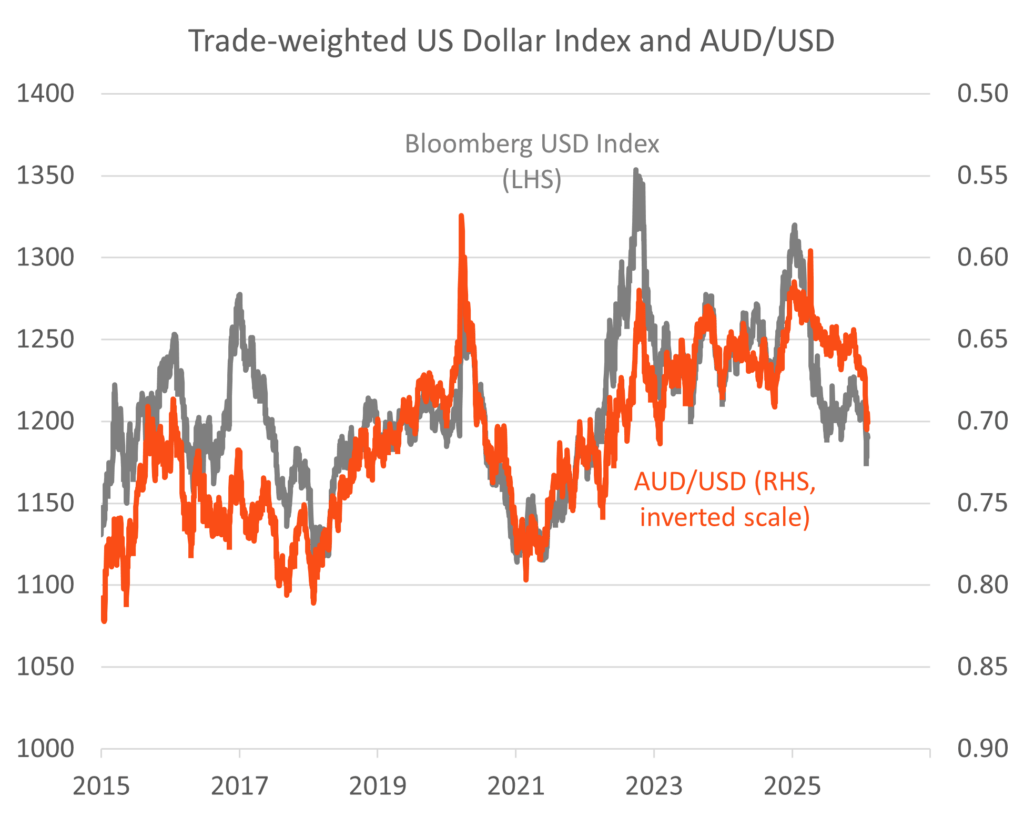

January saw the broad USD make a fresh cycle low, with the AUD among the best performers, up over 4 per cent against the greenback to breach 70 US cents for the first time in three years alongside a surge in commodity prices. President Trump’s recent comment that the dollar “hasn’t declined too much” only added fuel to the move, reinforcing the view that the administration is comfortable with a weaker currency.

Figure 2: Broad US dollar index and AUD/USD exchange rate

Source: Bloomberg. As at at 2 February 2026

Japan looms large in this policy divergence and broad USD story. The Bank of Japan (BoJ) has taken the policy rate to 0.75 per cent, with the 10-year Japanese government bond (JGB) yield breaching 2 per cent for the first time since 1998. More striking has been the action at the ultra-long end, where 30-year yields have approached 4 per cent amid growing fiscal concerns following Prime Minister Takaichi’s snap election announcement and the growing likelihood of further stimulus.

Despite this dramatic bear steepening in JGB yields, the yen has remained under pressure. Ultimately due to the slow pace of the policy normalisation and the highest inflation rates in decades, short-term real rates in Japan remain negative, and BoJ policy simply isn’t restrictive enough to support the currency. The yen remains favoured as a funding currency, and this is unlikely to change until the BoJ accelerates its hiking cycle or intervenes more aggressively in FX markets, which would likely accelerate the broad US dollar weakness.

Beyond diverging rate expectations, the structural case for USD weakness remains intact. Currency cycles last years, with overshoots in both directions. The last major USD bear market (2002-2011) produced a 30 per cent real depreciation during a period of significant US fiscal expansion and hawkish foreign policy.

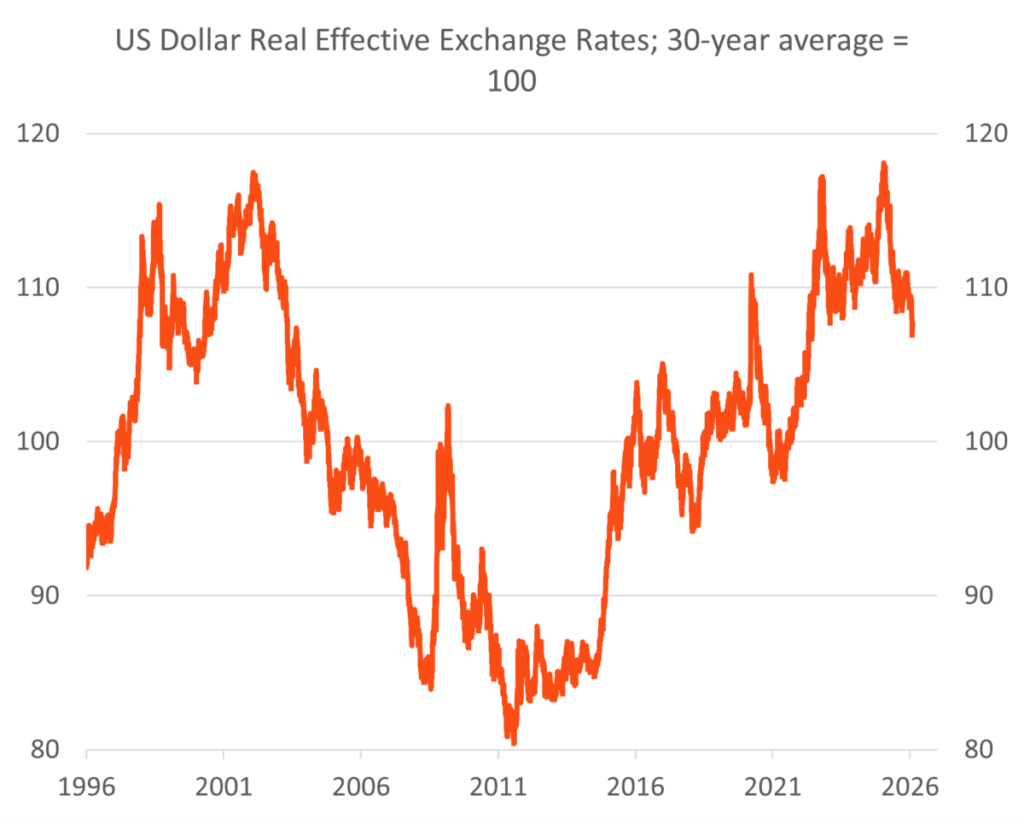

Despite the 7 per cent decline in 2025, the USD real effective exchange rate (the exchange rate adjusted for purchasing power vs trading partners) remains around 6 per cent above its 30-year average. If the Trump administration is serious about narrowing the trade deficit and rebuilding America’s industrial base, the USD may need to fall further in real terms.

Figure 3: USD real effective exchange rate based on purchasing power parity

Source: Citi. As at 2 February 2026

While the Trump administration officially maintains the “strong dollar” policy, this could be seen as referring to the USD’s reserve status rather than the exchange rate level. However, the administration will need to strike a delicate balance between facilitating a more competitive currency and not sparking capital outflows that accelerate the trend away from USD reserve assets.

Investment implications

For Australian investors with unhedged global equity exposures, these dynamics have meaningful portfolio implications.

US equities now account for over 70 per cent of the global developed market benchmark, well above the 30-year average of 56 per cent (as of 31 January 2026), meaning currency movements can have an outsized impact on returns for globally diversified portfolios.

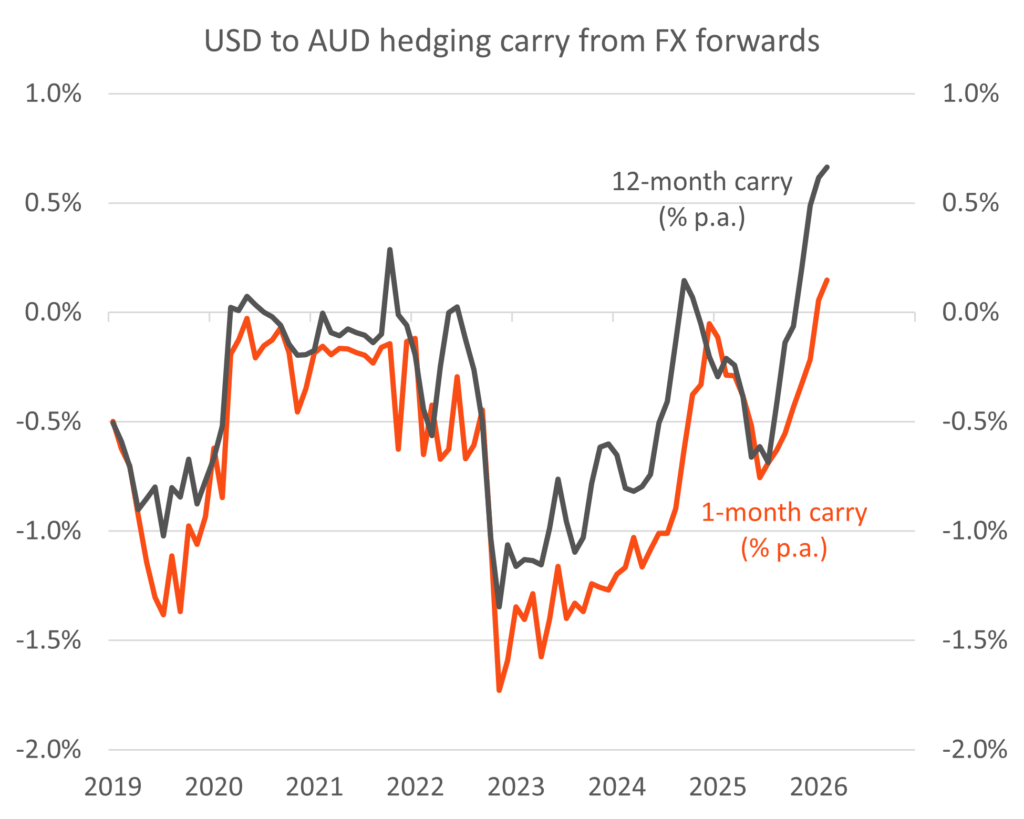

Perhaps the most notable shift has been in AUD/USD forward points, which have turned negative across all tenors as rate differentials have reversed. This means investors now receive positive carry when hedging USD exposures back to AUD – a stark reversal from the cost of hedging that prevailed throughout much of the post few years. Combined with a broader AUD tailwind from recovering commodity prices and a growing rate divergence between the Reserve Bank of Australia and the US Fed, the case for raising FX hedge ratios on global equity portfolios has strengthened considerably.

Beyond the hedging implications, the performance of the broad US dollar may have a large bearing on the relative performance across global equities and will be key to any rotation narrative playing out. Ultimately, US equity market outperformance has coincided with USD strength in recent years, and a sustained USD bear market will likely see emerging markets and more cyclically oriented developed markets benefit.

Figure 4: Annualised carry from hedging USD underlying to AUD using FX forwards

Source: Bloomberg. As at 2 February 2026

Unpack more key market questions and investment implications in our latest report.

Chamath De Silva is head of fixed income at Betashares, responsible for the portfolio management function and fixed income product development.