This article originally appeared in the print edition of Retirement Magazine Vol. 2, the decumulation-focused sister publication of Professional Planner.

The Australian annuity market has always been small. Many justifications have been offered, but none have explained the persistent low demand for life annuities.

In response to this so-called “annuity puzzle”, a team of academics from the School of Risk & Actuarial Studies, UNSW Business School studied new explanations for the apparent disinterest in life annuities, using data collected from two bespoke online surveys of Australians of around retirement age.

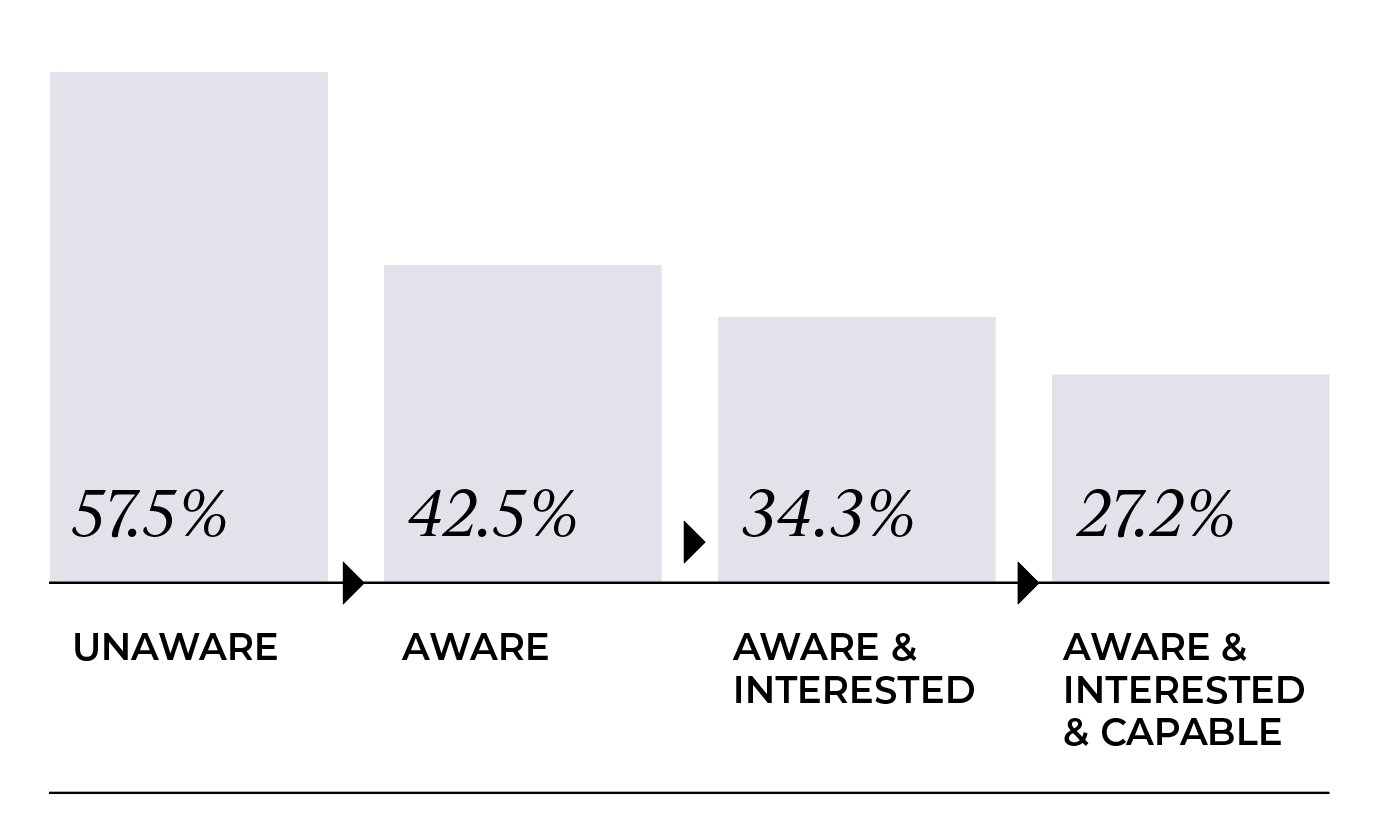

The first survey asked participants to self-assess their decision state for the purchase of life annuities: 57.5 per cent of participants stated that they were unaware of life annuities; 42.5 per cent were aware; 34.3 per cent were aware and interested; and only 27.2 per cent were aware, interested and capable.

Interest in life annuities was associated with good financial literacy, positive perceptions of life annuities and optimistic survival beliefs. A follow-up survey tested the impact of alternative forms of information presentation, designed to motivate a better understanding of longevity, on interest in life annuities. Interest in life annuities was 38.6 percentage points higher for those participants who were initially pessimistic about their survival but responded to objective life expectancy information by revising their survival beliefs upwards.

The annuity puzzle

In the academic literature the explanations for low demand for life annuities are generally categorised into rational (or economic) factors and behavioural (including knowledge) factors. The economic factors include pre-existing annuitisation (including public pensions or defined benefit pensions), bequest motives, adverse selection (through its impact on annuity prices), the desire for precautionary savings (such as to fund health and aged care expenses) and risk sharing within families. In Australia the Age Pension crowds out annuity demand for a large minority of retirees and the bequest motive and desire for precautionary savings cannot be dismissed. However, these economic factors alone cannot explain the small market for life annuities in Australia.

The behavioural explanations for subdued demand for life annuities have included: framing (specifically, presentation in an unattractive investment frame rather a consumption frame, narrow bracketing (where annuities are considered in isolation from overall retirement needs), default settings (where an annuity is not the default), loss aversion, psychological factors including fairness and psychological ownership, and product and system complexity.

However, in recent years most of the economic and behavioural barriers to annuity demand have been addressed by regulation and product design.

Decision states for the purchase of life annuities

The low demand for life annuities is typically considered in a world where people are assumed to be aware, interested and ready to choose a life annuity, and we are puzzled why people appear reluctant to purchase.

An alternative view, examined in the first survey reported in this article, is that people move through a series of decision states – from awareness to interest to capability – before they are ready to make a purchase decision. To be aware, they need to know the product exists; interest is associated with a belief that a life annuity is beneficial to them; and capability requires an understanding of the product features and their implications.

An online survey of decision state membership for the purchase of life annuities was administered in April 2024 to a representative sample of 1190 Australians aged 50 to 75, who currently have or previously had a superannuation account. The survey included a series of questions to elicit membership of four decision states: unaware of life annuities; aware; aware and interested; and aware and interested and capable. It collected data on demographics, household finances, preferences, financial literacy, product knowledge and perceptions, attitudes, psychological traits and subjective survival beliefs.

From the data collected, the decision state membership for the purchase of life annuities is summarised in Figure 1:

Figure 1 shows that in the representative sample of Australians of around retirement age, 57.5 per cent were unaware of life annuities, 42.5 per cent were aware, 34.3 per cent were aware and interested but only 27.2 per cent, or just over one quarter, self-assessed themselves as aware, interested and capable – in other words, ready to purchase.

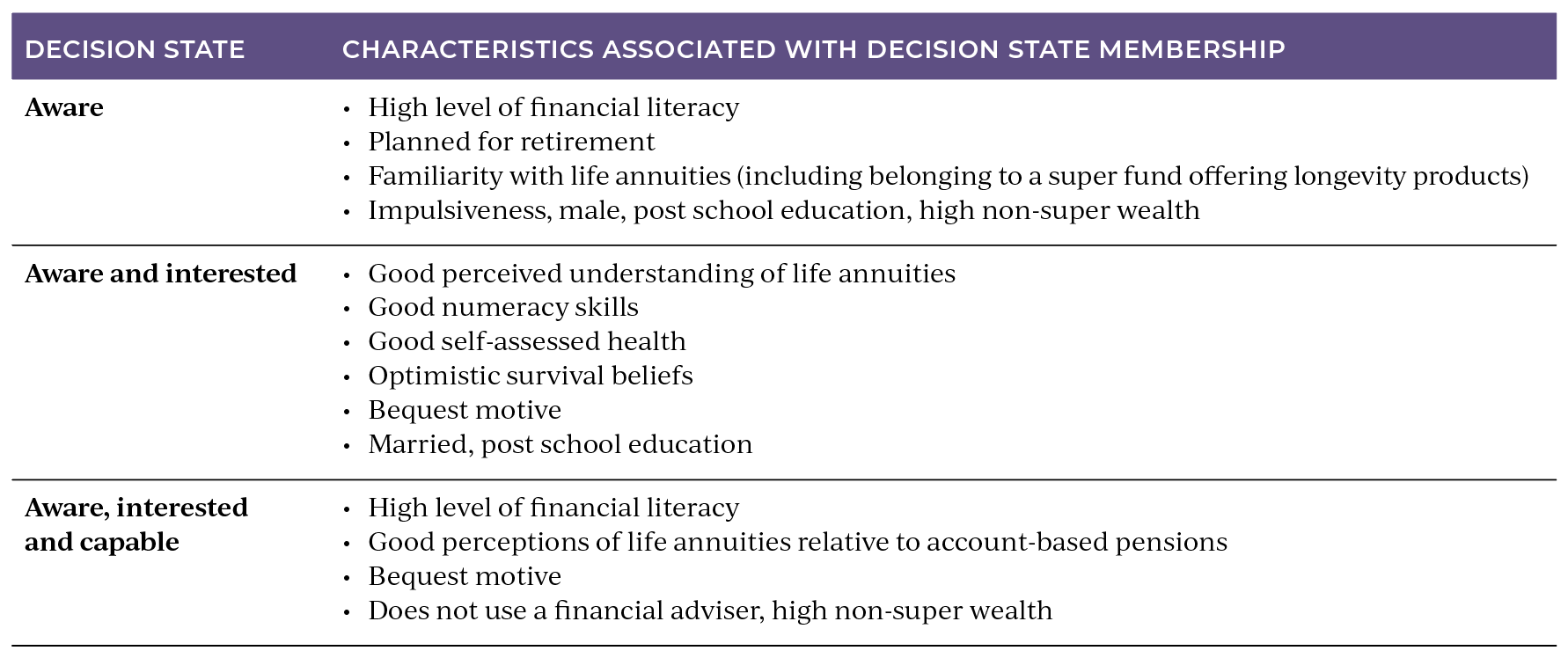

The collection of additional data enabled identification of personal characteristics associated with decision state membership, as summarised in Figure 2:

In summary, the decision state survey results suggest that the main barrier to lifetime annuity demand is lack of awareness, with 57.5 per cent of the representative sample of Australians of around retirement age unaware of life annuities. Low levels of financial literacy, poor perceptions of life annuities (relative to account-based pensions) and pessimism about health status and longevity are all associated with lack of progress through the decision states.

These results should not be surprising. Australians have had little opportunity to become aware of life annuities. The market for life annuities has always been small, there has been little opportunity for “social learning” through experiences of family and friends, and many superannuation funds do not include life annuities or other longevity products on their product menus.

Of participants who stated that they were aware of life annuities, only around one-third stated that they were interested in life annuities. Interest is motivated by relevance, yet many survey participants reported pessimistic beliefs about their survival as compared with a person of the same age and gender in the Australian Life Tables.

Survival beliefs and interest in life annuities

A second online survey was motivated by the finding that pessimism about longevity was associated with lack of interest in life annuities. The aim was to find out whether interest in life annuities could be enhanced through presentation of information treatments designed to improve understanding of longevity.

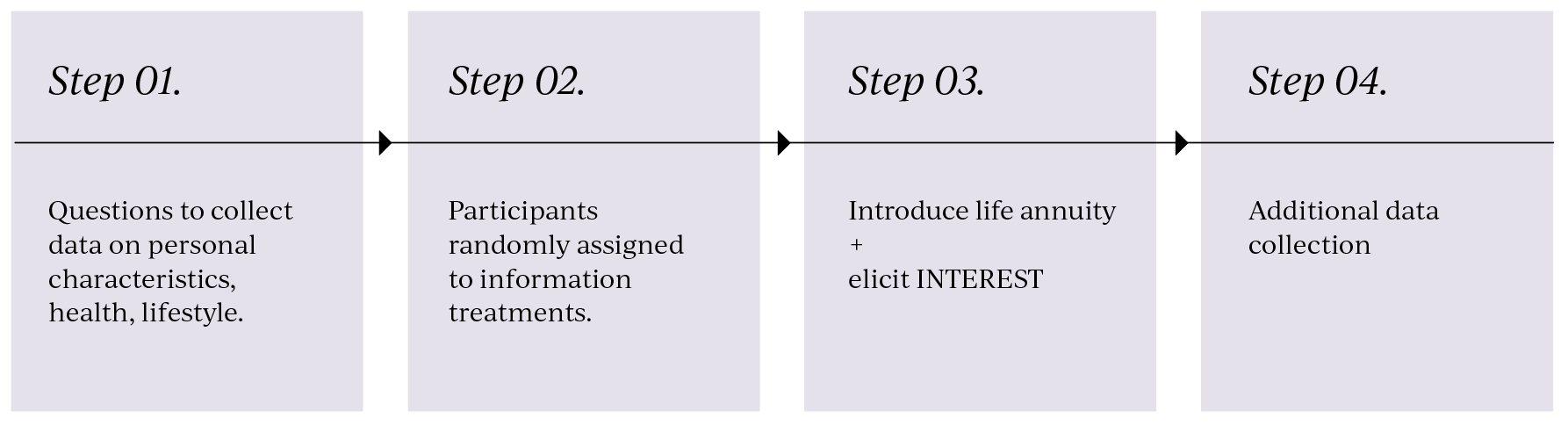

The survey was conducted in May 2025 with a representative sample of 1589 Australians aged 50 to 75, who currently have or previously had a superannuation account. Participants progressed through the survey in four steps, as illustrated in Figure 3:

Steps 1 and 4 involved the collection of data on the survey participants. In Step 2, participants were randomly assigned to either a control group or one of 16 different information treatment groups designed to enhance their understanding of longevity.

In Step 3, all participants were introduced to a life annuity and its characteristics and were asked about their interest in life annuities in terms of: NOT interested, SOMEWHAT interested, MODERATELY interested, VERY interested, EXTREMELY interested.

The information treatments in Step 2 were designed to help people understand how long they might live and the financial implications of living long, and included one or more of the following:

- Standard survey questions to elicit survival beliefs, specifically subjective life expectancy and/or late-in-life subjective survival probabilities.

- Presentation of “Objective” cohort life expectancy and late-in-life survival probabilities for a person the same age and gender from the Australian Life Tables.

- Presentation of “Personalised” life expectancy and late-in-life survival probabilities (modified from the Australian Life Tables using responses to survey questions on personal characteristics, health and lifestyle).

- Presentation of financial consequence information, which illustrated the financial consequences of living long, in the absence of a life annuity.

Participants assigned to treatment groups which involved the presentation of “Objective” or “Personalised” life expectancy and survival probabilities were invited to update their survival beliefs.

Results: interest in life annuities

Overall, regression analysis found that none of the information treatments had a significant impact on interest in life annuities as compared to the control group (who had received no motivating information). We had expected that motivating participants to think about their longevity and the financial consequences of living long would enhance their interest in life annuities.

Nevertheless, some interesting results emerged after consideration of the impact of the information treatments on participants’ survival beliefs.

A large proportion of the sample initially underestimated their life expectancy relative to both the “Objective” life tables and the modified “Personalised” life expectancy. On average, females in their 50s under-estimated life expectancy by around eight years and in their 60s by five years. Males in all age groups under-estimated their life expectancy by three to five years.

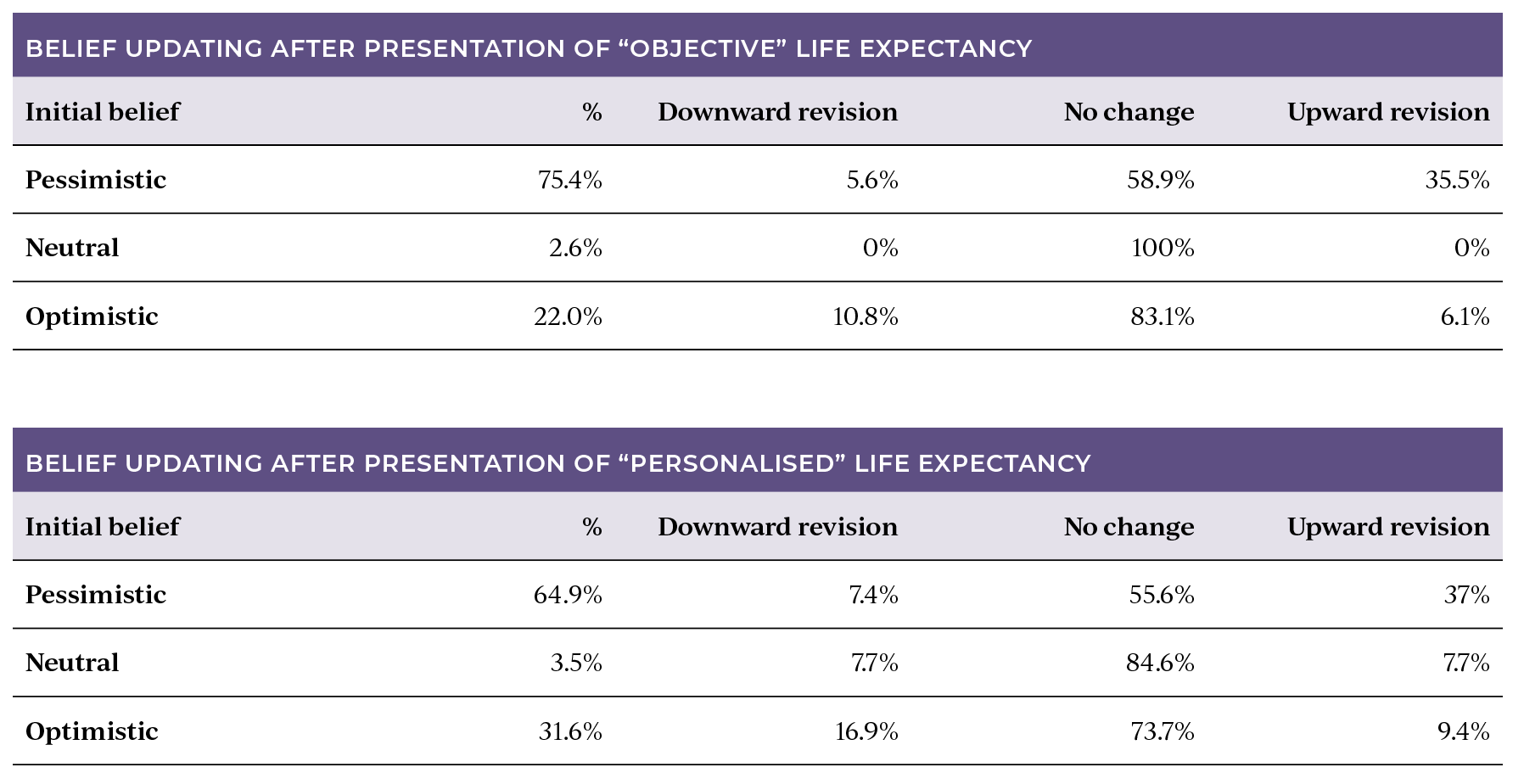

However, following presentation of “Objective” life expectancy information (for a person of the same age and gender), a large minority of those who were initially pessimistic about their life expectancy (specifically 35.5 per cent of the relevant sub-sample) revised their survival beliefs upwards. Similarly, 37 per cent of the relevant sub-sample of those initially pessimistic about their life expectancy revised their survival beliefs upwards following presentation of “Personalised” life expectancy information. The full set of survival belief updating is reported in Figure 4.

Impact of survival belief updating on interest in life annuities

In the final stage of our analysis we performed a regression to compare interest in life annuities between participants who were initially pessimistic and subsequently revised their survival beliefs upwards following the information treatments, and those who did not.

The key finding was that survey participants who were pessimistic about their life expectancy and revised their subjective belief upward after receiving “Objective” life expectancy information were 38.6 percentage points more likely to state that they were interested in life annuities. No significant effects were found for the other information treatments.

The results of the two surveys reported in this article can be summarised as:

- The decision state model provides a new explanation for the low demand for life annuities by categorising people of around retirement age by their readiness to make decisions about annuity purchase. An important finding is that 57.5 per cent of a representative sample of close to retirement Australians were unaware of life annuities.

- Key barriers to progression through the decision states for the purchase of life annuities are low levels of financial literacy, poor perceptions of life annuities relative to account-based pensions and pessimistic survival beliefs.

- Provision of “Objective” and “Personalised” life expectancy information motivated people to update their survival beliefs and, in some circumstances, increased interest in life annuities.

- People planning for retirement need some understanding of their expected life span and the implications of living long.

These findings should be of interest to superannuation funds who have the responsibility to assist members to achieve and balance maximising their expected retirement income; managing expected risks (including longevity risk) to the sustainability and stability of this retirement income; and having flexible access to expected funds during retirement.

Hazel Bateman is a professor in the School of Risk & Actuarial Studies at UNSW Sydney and deputy director of the ARC Centre of Excellence in Population Ageing Research. She is a member of The Conexus Institute advisory board, a retirement policy thinktank philanthropically funded by Conexus Financial, publisher of Professional Planner.

It is in many retiree’s Best Interests to purchase real lifetime annuities and be able to choose investment options that fit their risk profile.