A key theme in global and Australian financial markets is increasing investment in private assets by the private wealth sector. Private markets are transitioning from largely sitting within the realm of institutional investors, large family offices and ultra-high net worth investors towards being more widely used by the high-wealth and retail investor segments. Some have called it the ‘democratisation of private markets’.

Whether this is a positive development is a source of debate, and a focus of ASIC’s recent consultation into the state of public and private markets. Our submission took the stance that (institutional) super funds are a relatively safe way for individuals to access private markets, but more direct access by individuals raises some issues.

The fact is that increasing private wealth market participation in private assets is a strong trend that is likely to continue for the foreseeable future. Given the complex and opaque nature of private markets compared with their public cousins, a key question is how financial advisers can best assess client appropriateness and facilitate quality private market exposures for their clients.

Characteristics of private markets

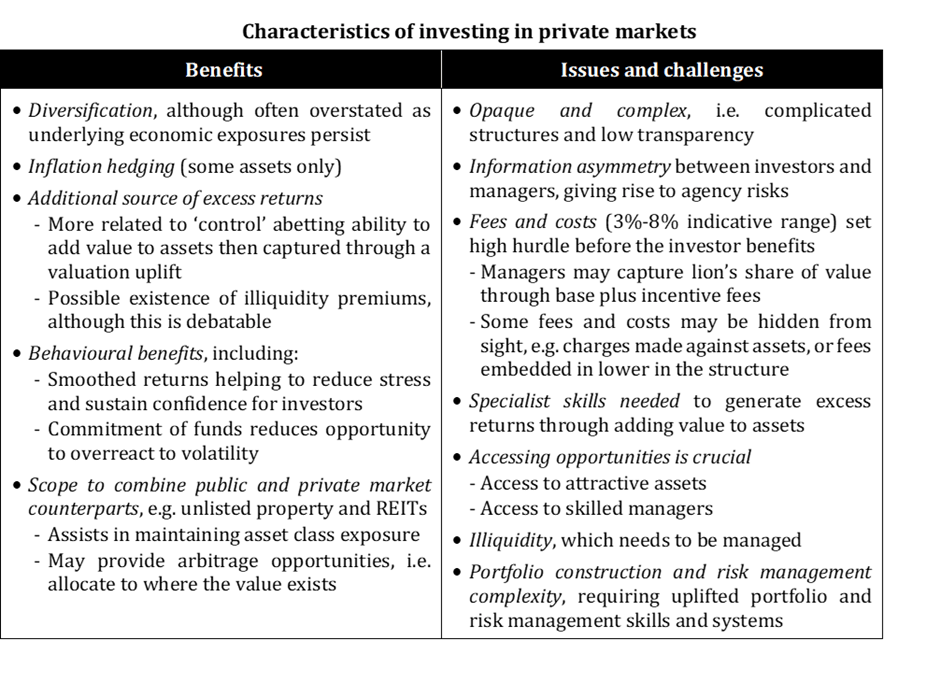

The figure below summarises benefits as well as issues and challenges of investing in private markets. Most of the benefits on the left are conceptually available to individual investors. It is when the issues and challenges on the right column are considered that the potential problems for individual investors become evident.

Source: The Conexus Institute*.

The role of advisers is central to the quality of private market exposures that many investors end up with. There are a range of hurdles for wealth advisory firms, the most critical being identifying and accessing investment managers (general partners) that will add value in excess of the lofty fees they charge in complex and opaque markets. While most institutional investors like super funds have overcome the hurdles to a significant degree, there appears greater dispersion in capability in the private wealth advice sector.

Private asset managers pushing into private wealth raises questions

We have two misgivings over the significant push of private asset managers into private wealth, who are being attracted by a significant asset-gathering and fee generation opportunity.

First is whether individual investors get the dregs rather than the cream. Relationships matter for access in private markets, with the better private market managers often picking their own clients. Could individual investors be given access to poorer managers who have trouble raising funds elsewhere? Could they be offered the less attractive opportunities?

Second is the implications of raising a lot more capital. At the industry level, it creates competition for attractive assets and can test capacity limits. More subtly, the push into private markets is being led by the larger private asset managers that have traditionally demonstrated skill. In a large part this is because the larger managers can afford the resources needed to service the private wealth sector and leverage their recognisable brands.

However, larger size may make it harder for those organisations to generate returns for a range of reasons. There are larger portfolios to fill up and attractive opportunities may be limited. Skill can be diluted as the talent moves from managing money to managing people. Bureaucracy can stifle entrepreneurial spirit. Stars could leave to set up their own shop.

In short, outsized asset gathering can erode returns. The push into private wealth is playing its part.

Wealth advisers critical to outcomes

Advice firms, whether operating on a retail or wholesale basis, are fundamental to guiding individual investors when accessing private markets. They can educate their clients on the workings of private market investing. They can help clients assess the appropriateness of private markets given their objectives and liquidity needs. From an investment perspective, advisers can provide intelligence on and access into a selected universe of opportunities.

Wealth advisers may face some limits in assisting clients in these ways. Advisory firms are likely to face transparency issues to the extent that manager disclosures and manager research are limited in scope, and their avenues to directly engage with managers are very limited. Adviser groups may have trouble accessing the best private asset managers. There is likely to be little scope for advisers to negotiate fees.

What to consider when investing through private market managers

Below is a (non-exhaustive) checklist of issues that financial advisers and advisory groups could consider when investing with private market managers. The list motivates two challenges. First is ability to access high-quality managers that are likely to deliver returns to the benefit of clients. Second is being resourced to evaluate managers, which will involve highly-compensated staff or consultants. There is scope for sizable dispersion in these areas across the private wealth sector that is likely to lead to a broad range of client outcomes.

Checklist of considerations when investing with private market managers

| Consideration | Notes |

| Manager capacity to generate returns | Whether a manager is any good is critical but uncertain aspects to consider:

· Asset class and sector outlook · Manager research, where it is available · Experience and track record of manager and key investment staff · Quality of co-investors · Whether assets invested exceed capacity, considering fund and sector · Organisational developments that could dilute skills or impact culture |

| Manager alignment with investors |

|

| Fees and costs |

|

| Risk |

|

| Fund structure | Different fund structures suit different investors, with two most notable:

|

| Liquidity |

|

| Valuation governance | Consider scope for risk of conflicts due to fee structures and potential for inequities from access to funds being inconsistent across different investor classes, including method used and frequency

|

| Manager resources |

|

Source: The Conexus Institute.

Private markets can also create financial incentives, direct or indirect, such as fees for underwriting, placement and product manufacturing (for example, embedded into internally managed vehicles). At a minimum these should be disclosed to clients.

Finally, private markets can introduce considerable operational complexity to wealth advisory businesses. A well-known example is coordinating capital calls across a client book. This introduces a higher-touch engagement model accompanied by greater cost.

Trend to private assets can be sustained if care is taken

The trend towards greater use of private assets by individual investors seems likely to continue, partly self-motivated and partly prompted by private wealth advisers. Private asset managers seem eager to oblige. The challenge for the private wealth sector is to ensure that clients have access to quality exposures that are properly incorporated into their portfolios, and remain well-informed.

Super funds are a well-established conduit to private markets for their members. We see a broader range of capabilities in the private wealth space. And private markets provide an exciting opportunity set but are far from an easy win. Care is needed to ensure the trend to private markets by private wealth doesn’t lead to case studies of poor client outcomes.

*The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.