Our main reflection from the Conexus Retirement Conference (full reflections here) is that super funds are building momentum in retirement but have a long way to go. Given the positive progress, we could be accused of being a naysayer. However, evidence provided by APRA and ASIC suggests that many funds are lagging. A large gap remains between the current state of the system and its potential.

Funds need to keep moving forward to ensure that all retirees receive a suitable retirement strategy. And progress needs to be fast: around 250,000 Australians enter retirement age each year. In this article, we offer thoughts on how the industry might continue to progress.

The Retirement Conference is run in an open-forum style inside Canberra’s Old Parliament House, attendees from the 14 largest super funds were joined by representatives from Treasury, APRA, ASIC, Government and the opposition, as well as thought leaders including seven industry partners. The 2024 edition continued with a purpose-led format that focused on some of the key challenges faced by the industry.

Framing the ‘next steps’ discussion

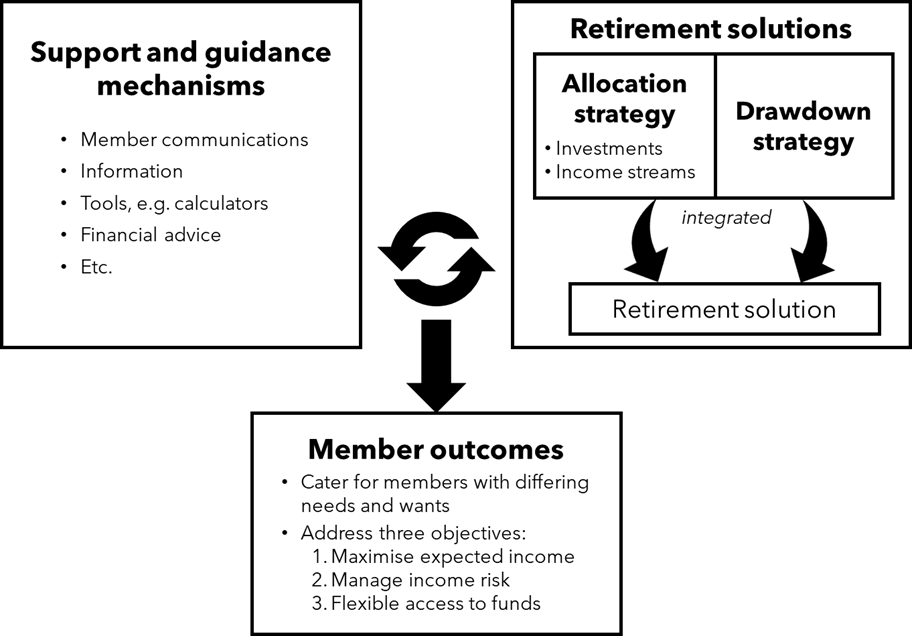

To frame the discussion, we use the diagram below that may be familiar to many readers. A high-quality retirement income strategy comprises two key components. On the left are the support and guidance mechanisms required to identify the characteristics, needs and preferences of retiring members. On the right are retirement solutions that convert assets into outcomes (mainly income) by blending investments (probably via an account-based pension), potentially lifetime income streams and drawdown strategies.

Funds need to move forward in both areas to satisfy their obligations under the retirement income covenant.

Next steps for support and guidance mechanisms

Further development of support and guidance mechanisms that can cater for different member types is required. As well as accounting for differences in personal financial characteristics, perhaps a more pressing area is how retiring members engage with their funds. Though there are various framings, APRA deputy chair Margaret Cole in her address at Retirement Conference identified three broad types: those who use a financial adviser, the self-directed, and the disengaged.

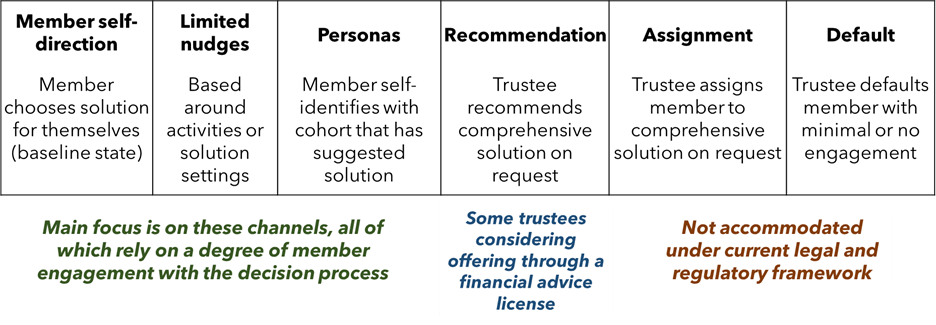

The diagram below expands on our previous work on retiree pathways into suitable retirement solutions and the mechanisms that might be used by fund trustees to assist members into appropriate retirement solutions.

The mechanisms of assignment and default can be placed aside for the time being as they are not currently supported by policy. Variable degrees of development are observed in other areas, potentially reflecting the difference in degrees of legal and regulatory support, interpretations of what is required and risk appetite across funds. We provide a few examples to illustrate.

Many funds have developed services for member self-direction. AustralianSuper is one of a number of funds offering a broad information hub containing financial and non-financial retirement information. EquipSuper offers direct in-person assistance with advisers who provide general advice. UniSuper offers a service consisting of multiple calculators and personal assistance to help members understand and use the calculators effectively.

While we are seeing the use of limited nudges, most seem to be activity-based rather than offering financial recommendations. Examples of activity-based nudges prompt members to seek information or initiate application processes, often within the framing of ‘member journeys’. The hesitancy around using nudges to support financial decisions appears motivated by concern over legal and regulatory risk and recognition that member circumstances can be complex. These considerations arguably leave other mechanisms on the above diagram as ‘safer ground’ for trustees.

A notable application of personas was CSC’s recent launch of personas-based pathways for its members. This approach asks members to self-identify with a member type for which a broadly tailored solution has been designed. Videos and calculators are provided to support members with their decisions.

Some trustees are providing personalised recommendations on a scalable basis under a financial advice license. Aware Super is the most prominent example, where a Statement of Advice is generated through a digital process. This is supplemented by potential for conversations with staff, and a linked retirement calculator to explore options. Aware suggests that the impact on participation and next-step taking by members have been quite constructive. We expect further announcements by super funds around digital advice, potentially implemented through partnerships with licensed digital advice providers.

Leading funds need to offer integrated retirement solutions

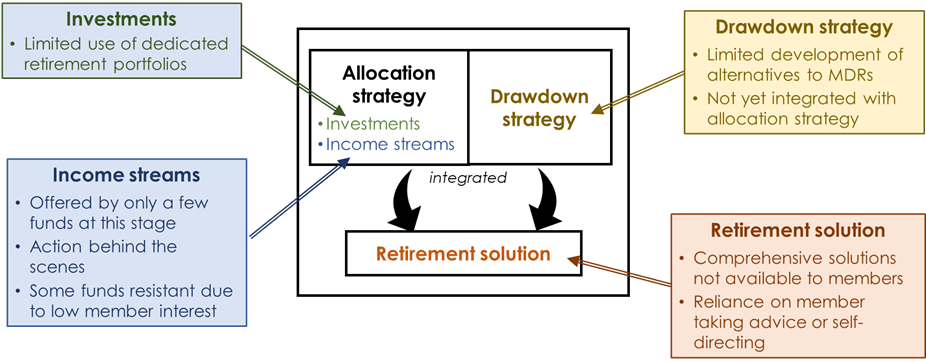

Greater focus seems to have been placed on guidance and advice, i.e. the left side of our first diagram. While there has also been progress on the (right-hand) solution side, we sense that the industry has much more to do. Our assessment is reflected in the diagram below. There is considerable scope to develop each of the component activities. At the moment, no fund has all the building blocks fully formed-up and brought together in an integrated fashion.

Many funds offer the same investment strategies as for their accumulation funds, despite aspects such as differences in purpose (income provision versus growing savings), tax regimes, member risk tolerances, etc. (We discuss how retirement portfolio might be run differently here.) Aware Super and Telstra Super are examples of funds that have innovated in their investment portfolio design.

Few funds have incorporated lifetime income streams on a fully integrated basis ranging from member information through to effective incorporation into calculators and advice engines onto administrative implementation. As well as development lags, we sense that some funds may be facing into challenges such as internal philosophy (e.g. relevance of lifetime income streams across their membership, and need to face into tailoring), and the complexity and costs associated with delivery.

Drawdown rates could be more effective than simple reliance on the minimum drawdown rates. AustralianSuper is a prominent example of one of the few funds offering a financial nudge through their Smart Default drawdown rates that raise income in the early years of retirement. CSC also varies drawdown plans across its persona-based solutions.

We are yet to see a fund that readily provides tailored solutions bringing together all of the components – although CSC comes close. We acknowledge that funds reaching this point is difficult and will take time.

Guidance and advice enable integrated solutions, but other factors also at play

Both sides of our first diagram are important, and need to work in tandem. The left side of guidance and advice is an important enabler of the right-hand side. The right side of retirement solutions is what delivers the actual outcomes through retirement (you can’t eat advice). Members need to be in the solution that suits their needs, and for that solution to deliver good outcomes.

David Bell is executive director and Geoff Warren is research fellow at The Conexus Institute, a not-for-profit think-tank philanthropically funded by Conexus Financial, the publisher of Professional Planner.

Leave a Comment

You must be logged in to post a comment.