Retirees need to find their way to a retirement solution that is suitable for their needs.

In a newly released research report (feedback appreciated) we address the various mechanisms through which this could occur.

The retirement system is currently configured around two mechanisms. One is a retiree taking personal financial advice. However, some people find this too expensive, and this pathway is constrained by limits on the number of people the financial planning community can practically serve.

Another is a retiree choosing for themselves. This is a daunting task that many people neither have the desire to do, nor the capacity to do so effectively.

Which raises the question: what other options are available? In particular, what role might be played by superannuation fund trustees?

Superannuation funds are currently developing retirement income solutions for their members and decision support services to help them choose. However, trustees going a step further to explicitly direct members towards solutions is problematic under the financial advice rules.

If a member asks their fund ‘what solution would work for me?’, it is highly likely they won’t get a direct answer.

Against this background, the role of trustees in guiding members to retirement solutions is a live issue following the Quality of Advice Review. The QAR proposed a broad range of providers advising on a large range of topics under a ‘good advice’ obligation. The Government’s response has been to focus on retirement as a critical unmet advice need that could be addressed through super funds.

The rationale for using funds is that trustees need to guide members under the Retirement Income Covenant and operate under strong duties and regulatory frameworks. A mechanism that draws on the intra-fund advice framework is a possibility.

Meanwhile, there has also been talk around retirement defaults. While AustralianSuper has been at the forefront of this conversation we are also hearing some discussion around the industry.

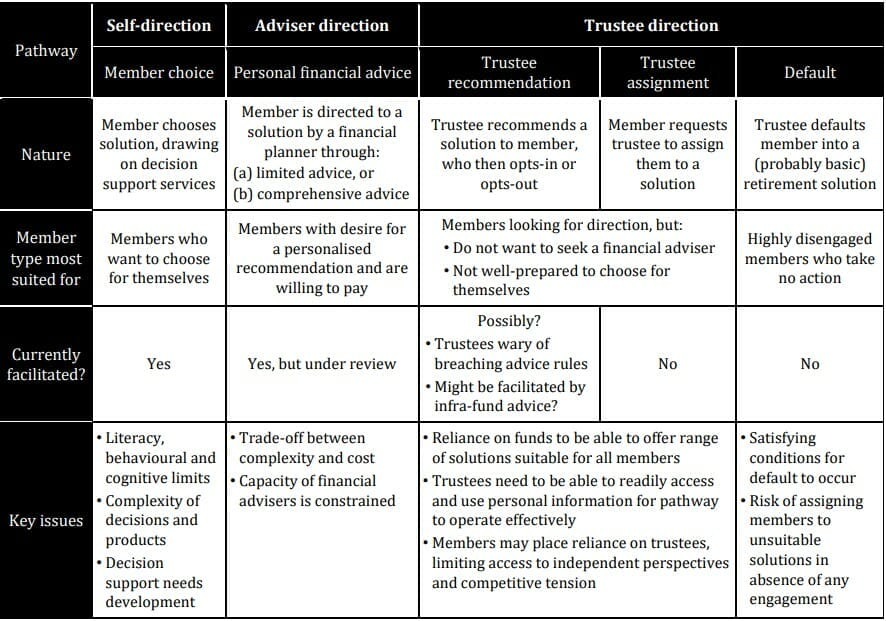

Stepping back, we see five potential pathways for directing consumers to retirement solutions. These are summarised in the diagram. As well as self-direction and adviser direction, we see three further pathways under the trustee direction heading including recommendation, assignment and default.

Pathways to a suitable retirement solution

The trustee direction pathways would cater for members who won’t pay for advice and do not want to choose for themselves. About 70 per cent of members might sit in this group across the industry. For instance, a member survey conducted by Frontier Advisers in 2022 found that 20 per cent of members (sampled from five profit-for-member super funds) wanted to choose a retirement solution for themselves while only 9 per cent were seeking financial advice. The other 71 per cent wanted some form of guidance from their fund.

The trustee recommendation pathway might accord with what the Government has in mind. However, framing the issue around the intra-fund advice mechanism may not be the right place to start.

Rather, we suggest first identifying the problem that needs solving. We see this as ‘a need for an efficient and scalable mechanism for fund trustees to direct members to retirement solutions’.

This might be done through accommodating trustee recommendation as a particular form of advice. Or it could be achieved through the trustee assignment pathway under a different type of legal mechanism. Both pathways would require the ability of trustees to readily use personal information to identify a suitable solution for a member and direct them towards it.

A ‘hard’ default could benefit highly disengaged members who might otherwise take no action and remain in accumulation. As of June 2022, there was $266 billion invested in 1.37 million accumulation accounts by members aged 65 or over. A portion are likely still in accumulation for no good reason.

While some sort of trustee-directed pathway is needed to cater for members who might not otherwise receive the guidance they need, it must be efficient and scalable to make a meaningful difference. This requires enabling trustees to assist members through straightforward and possibly automated processes without too much cost on funds or burden on members.

Retirement plans provided by advisers will differ from the guidance provided by super fund trustees in important ways. Advisers can provide comprehensive advice for all members of a household and address all financial exposures. Super funds will most likely be constrained to addressing individual members and their super fund assets. Advisers can use products from a variety of providers, presenting a ‘best-of-breed’ opportunity. Advisers can thus offer high quality retirement plans that go well beyond what a super fund trustee can provide, especially for households with complex situations.

A range of potential pathways exist for directing retires to suitable retirement solutions that cater for the differing ways that members engage with the system. The Government wants super funds to be a major part of the solution, which would amount to enabling trustee direction. The challenge for policymakers is to design an effective mix of pathways to meet the needs of all members.

David Bell is executive director of The Conexus Institute. Geoff Warren is research director of The Conexus Institute, and an Associate Professor at the Australian National University.

Leave a Comment

You must be logged in to post a comment.