*This article is produced in partnership with PIMCO

Bond markets suffered one of their worst years in decades in 2022 as central banks, including the Fed and RBA, hiked rates aggressively in their battle to tame inflation. Given the experience of 2022 and a volatile first quarter of 2023, investors are understandably wary. However, we believe that the rate hiking cycle, which contributed to recently elevated volatility across asset classes, is coming to an end in most developed markets. In Australia, we estimate that a 3.5-4 per cent cash rate in 2023 will be close to the most restrictive Australian households have experienced in terms of the percentage of their disposable income that will be required to service their debt. We think this limits the extent that the Reserve Bank of Australia can hike beyond 4 per cent without creating material financial stability risks.

We believe that recessions are likely across developed markets in 2023-2024, although we expect them to be modest. Consistent with that picture, equity markets appear more vulnerable than usual. From an asset allocation perspective, the outlook for fixed income has become much more positive. Following central bank moves over the past year, bonds now offer more attractive yields than they have in several years. We also believe that with today’s uncertainty, fixed income can act as an important building block for defence, income, and diversification, offering the potential for both attractive returns and mitigation against downside risks, particularly in a recessionary environment.

Why yield matters: Higher return prospects for bonds

In 2022, 10-year US and Australian government bond yields both rose as the Federal Reserve and RBA hiked cash rates. This recalibration to higher levels of yield may provide an attractive entry point for multi-asset investors. In addition to the higher return prospects, a higher level of yield reduces the probability of a negative return in the future. The yield creates a cushion against potential increases in the risk-free rate beyond what is currently priced into markets. Further increases in yields (beyond current market expectations) could lead to short-term losses, but they would improve the reinvestment opportunity and could lead to higher returns over the long run. In considering historical performance, analysing returns over all five Fed hiking cycles since 1988 we found that, on average, core bonds underperformed equities in the year before and during the hiking cycle. However, for the 12 months after the hiking cycle, rate sensitive sectors tended to outperform credit and equities. Hence, investors have historically been well served by increasing exposure to fixed interest towards the end of a hiking cycle.

The stock-bond correlation should remain negative in recessionary periods

For the past 20 years, the stock-bond correlation has, on average, been negative. However, in 2022 the correlation was positive in both the US and Australia. This was hardly surprising. Generally, we find that shocks to the equity market tend to be associated with a negative relationship, while shocks to real bond yields and expected inflation are associated with a positive relationship between stock and bond returns.

Importantly, bonds have typically provided positive returns and outperformed equities in recessionary periods. In fact, excess bond returns have been positive in nine out of the last 10 recessions in the US, and we expect this diversification property to remain intact in the event of a material economic downturn. With yields much higher than a year ago, the room for a potential bond market rally in a recessionary shock is much higher.

Diversification benefits of fixed income in an equity-dominated portfolio remain intact

Most Australian portfolios have a large allocation to equities. This overweight may have appeared reasonable when government bond yields were close to all-time lows, but the optimal stock-bond portfolio mix has changed materially given the repricing seen in 2022.

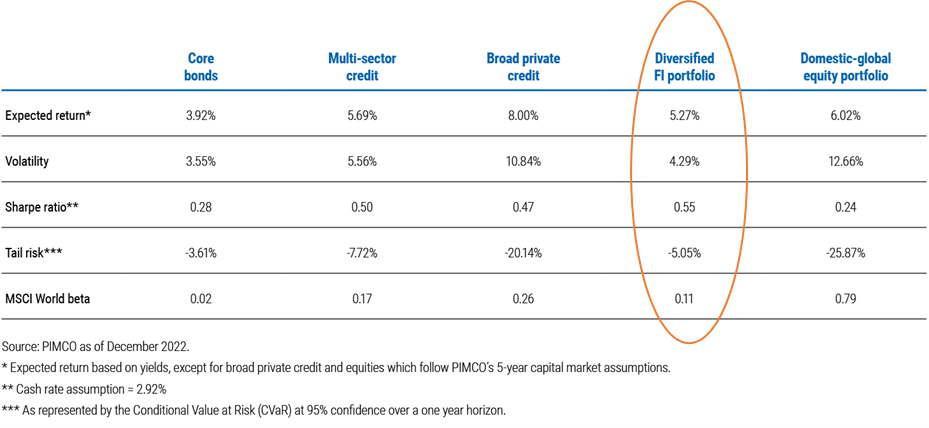

We analysed the risk and return characteristics of core bonds, liquid multi-sector credit, and private credit as well as a diversified portfolio combining these three assets and compared these to an equities portfolio. The diversified fixed income portfolio demonstrated an attractive expected return not far below equities with less than half of the risk.

Table: A diversified fixed income portfolio offers reasonable returns with lower risk than a diversified equity portfolio

Source: PIMCO

Bonds continue to play a key role in a diversified portfolio

From an asset allocation perspective, the outlook for fixed income has become much more favourable in recent months. Investors with long time horizons can lock in high levels of yield and benefit from the increased diversification potential in fixed income.

The fixed income universe is broad and ranges from assets that have low to negative correlation to equities, to those that are highly correlated to equities. This means diversification and sensible portfolio construction are key to meeting investor objectives.

While core bonds should remain the anchor to a traditional fixed income portfolio, complementary strategies like multisector credit, or private credit strategies may aid performance during periods of elevated interest rate volatility.

Our analysis shows that adding diversified fixed income exposure to multi-asset portfolios that are dominated by equity risk materially improves the expected Sharpe ratio even if the stock-bond correlation were to be strongly positive.

Disclaimer:

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

The material contains statements of opinion and belief. Any views expressed herein are those of PIMCO as of the date indicated, are based on information available to PIMCO as of such date, and are subject to change, without notice, based on market and other conditions. No representation is made or assurance given that such views are correct. PIMCO has no duty or obligation to update the information contained herein.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown.

The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. You should consult your tax or legal advisor regarding such matters. Please contact your account manager for further information.

PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246 862 (PIMCO Australia).

Past performance is not a reliable indicator of future results. Investment management products and services offered by PIMCO Australia are offered only to persons within its respective jurisdiction, and are not available to persons where provision of such products or services is unauthorised. Before making an investment decision investors should obtain professional advice. PIMCO Australia believes the information contained in this publication to be reliable, however its accuracy, reliability or completeness is not guaranteed. Any opinions or forecasts reflect the judgment and assumptions of PIMCO Australia on the basis of information at the date of publication and may later change without notice. These should not be taken as a recommendation of any particular security, strategy or investment product. All investments carry risk and may lose value. To the maximum extent permitted by law, PIMCO Australia and each of their directors, employees, agents, representatives and advisers disclaim all liability to any person for any loss arising, directly or indirectly, from the information in this publication. No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission of PIMCO Australia. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

Leave a Comment

You must be logged in to post a comment.