In February this year it became law that all workers will be covered by the superannuation guarantee (SG) regardless of their monthly pay. This replaces the $450 monthly threshold. Ever since that announcement I’ve worried that many low-income earners will experience a reduction in take-home pay. Fortunately that is unlikely to be the case. Overall, this provides a good opportunity for self-reflection.

The problem explained

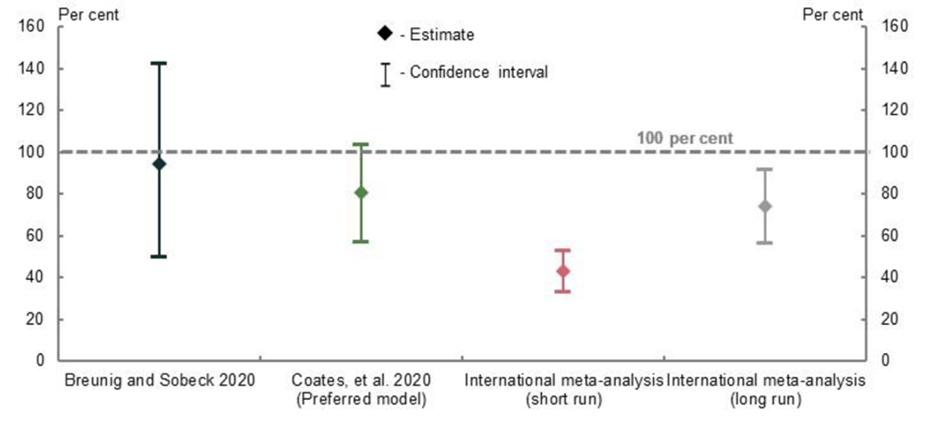

The Retirement Income Review explored the nature of the pass-through relationship to wages from the SG. A range of different analyses (see the summary chart from the RIR below) identified that a strong positive relationship exists, with 80 per cent a reasonable approximation. This means that 80 per cent of any increase in SG payments would be met, over time, through reduced wages. In some cases this would be instant (where a job contract exists whereby remuneration is $X inclusive of super), while in other cases this would occur through time and be less explicit (i.e. reduced future wage increases).

Chart: Estimates of the pass-through to wages from the SG and mandated benefits, 95 per cent confidence intervals. Source: RIR (Chart 6A-3).

My fear was that providing SG coverage for low-income earners would result in an instant reduction in wages. While many people earning less than $450 per month may be young casuals there is also a cohort of mature workers who have limited work opportunities due to carer responsibilities (children or elders) or are restricted by a disability. Many in this cohort are women. For these people a reduction in take-home wages would be a poor outcome. They may not be able to work extra hours to offset the shortfall.

Wages unlikely to fall

Fortunately, wages are unlikely to fall for low-income workers under the extended SG eligibility arrangements. There are various reasons.

First, existing award structures for lower income roles appear to be explicit on wage levels, not the aggregate of wages and SG payments. So there is no automatic reduction in wages. Even for those workers not covered by industrial awards it is difficult (unpopular) to reduce take-home wages.

Second, the administration of SG eligibility arrangements has always been problematic. Employers needed to assess whether employees have met the $450 per month income test (a frequency which may not match up with their pay cycle). This explains why around 30 per cent of all workers earning less than $450 per month were already receiving SG. The new eligibility law will reduce administration costs for employers, partly offsetting what are nominally quite low SG payments ($45 per month or less).

Third, the overall cost to employers is small in the context of total labour costs, and partly offset by the reduced administration costs. Employees earning less than $450 per month make up less than 5 per cent of all employees and a much smaller percentage of total employer labour costs.

Overall, it appears that in most cases, any net increase in employment costs will either be absorbed by employers or spread over the full payroll, which would result in a very small adjustment for all workers, most likely offset against future wage rises.

Reflections

When the SG-eligibility laws changed this year, a natural reaction would have been positivity at the prospect of improved retirement outcomes for low-income workers. The reflection is whether you balanced this against the possible impact on working-life outcomes.

You, unlike me, may have been well-aware of the micro-detail of casual and part-time labour markets and confident that there would be no adverse effects for low-income workers. In that case no reflection required.

However, if you hadn’t considered this issue, is some introspection required? As an industry do we have the right framing between working-life and retired-life outcomes? Does this framing account for the varying support received by households through the life-cycle (e.g. unemployment support relative to Age Pension) and the changing nature of pressures faced (e.g. housing and rent affordability)? These are all elements of how one part of a system integrates with broader society, and accordingly a reflection of the maturity of the superannuation industry.

It is fantastic that more people will experience SG contributions, and reassuring that in the majority this will not be to the detriment of working life outcomes. If you hadn’t considered the impact on working life outcomes this is a safe opportunity for self-reflection around getting the balance right.

Leave a Comment

You must be logged in to post a comment.