Every year the Australian Securities and Investments Commission (ASIC) releases its corporate plan, looking ahead five years and giving us an insight into which rocks it will be looking under to find the creepy crawlies that periodically infest the financial services industry.

In its latest plan, ASIC looks ahead to 2025 and provides readers with an handy guide to what it describes as “positive behaviours”. These are the behaviours ASIC expects of the companies and individuals it regulates, which it believes will “[improve] financial outcomes for consumers and investors and [support] the economic recovery”.

“At all times, we expect our regulated population to act in a fair, professional and ethical manner, in the best interest of consumers and investors,” it says.

A regulator charged with upholding consumer protection would say that, wouldn’t it?

ASIC defines “positive behaviours”

Below is what you could reasonably call ASIC’s summary guide to being good:

- Strong governance controls that support sound decision making and a culture of achieving fair and efficient outcomes

- A commitment to design and distribute products that meet the needs of consumers

- Robust disclosure and reporting practices that provide clear, accurate and timely information to consumers based on their needs

- Healthy competition between product and service providers, based on differing business models and structures

- Timely and accurate significant breach reporting to ASIC

- Efficient handling of complaints and dispute resolution, and appropriate and timely consumer remediation where losses have resulted from poor conduct.

If this all sounds a bit familiar, then there’s a good reason. You may remember an inquiry that ran for most of 2018 and examined misconduct in the banking, superannuation and financial services industry.

At the end of that, amid several thousand pages of background, context, reasoned arguments and recommendations, Commissioner Kenneth Hayne came up with a handy checklist that distilled almost the entirely of the Corporations Act and his recommended amendments into six pithy principles: obey the law, do not mislead or deceive, act fairly, provide services that are fit for purpose, deliver services with reasonable care and skill, and (when acting for another) act in the best interests of that other.

ASIC’s 2021 guide to being good has clear echoes of the royal commission’s 2019 final report, so at least the regulator’s focus is consistent, and the financial services industry can’t say it hasn’t been warned about the sorts of carry-on that won’t be tolerated.

Given the sheer volume and complexity of regulatory change in financial advice to date and what is yet to come (especially in October alone), ASIC’s guide is a timely reminder of what licensees, advisers and advice practices should keep their eye on as they grapple with the gritty practicalities of implementing new rules and laws.

Even if a potential response to new requirements meets the letter of the law, will it adhere to one or more of ASIC’s outlined behaviours? If the answer is clearly yes, it’s worth considering. If the answer is clearly no, then it’s a response best avoided. Even if it’s not clearly yes, it may be worth thinking about more deeply before going ahead.

The importance of being authentic

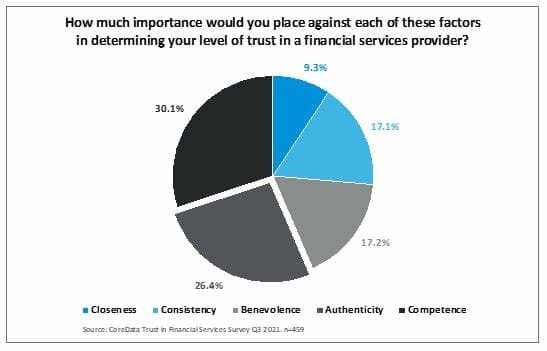

When we ask consumers about their trust in financial services providers, we first ask them how they rank three important elements of trust: authenticity, benevolence, competency, consistency and closeness.

In the context of discussing ‘good’ behaviour, it’s instructive to look at how consumers perceive authenticity – or, as it is described in our survey work, how important it is to them that a financial services provider is “genuine and honest, i.e. they are what they say they are and will not misrepresent anything.”

Authenticity in dealing with consumers is the second most important element of building trust, behind only competence. We’ve discussed here before the issue of competence, and the undoubtedly positive effect new education standards have on consumers’ perception of financial advice and advisers.

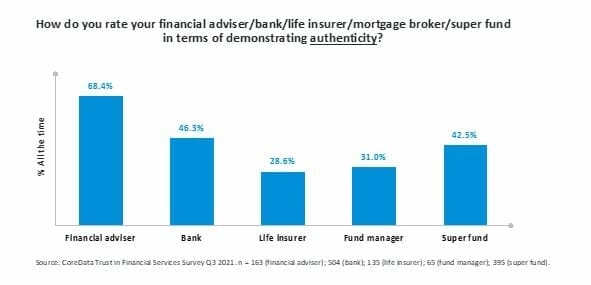

We find that consumers of financial advice rate their financial adviser much higher for demonstrating authenticity than consumers rate their banking, superannuation, life insurance, fund management and mortgage broking services. And this has a significant impact on how much consumers of financial advice trust their financial adviser.

Overall, less than half (45.6 per cent) of consumers consider financial advice to be a trustworthy sector. But that number very nearly doubles (to 88.1 per cent) among consumers who receive ongoing advice and increases by more than a third (to 61.7 per cent) among consumers who receive financial advice periodically.

This gives weight to the idea that the benefits, value and trustworthiness of financial advice aren’t fully appreciated by consumers until their advice needs have been met by a competent and authentic financial adviser. The trick, as we all know, is to help more people realise they have advice needs and to remove the barriers to them going to talk to an adviser.

The good news in ASIC’s 2021-25 Corporate Plan is that meeting Australians’ unmet advice needs is one of the regulator’s priorities. ASIC says it will “engage with industry on impediments to industry’s ability to deliver good quality and affordable personal advice”, and it will “take appropriate regulatory action to address these impediments, to the extent permitted by ASIC’s regulatory powers and resources”.

The “to the extent permitted” bit is something of a caveat, but overall it’s a welcome objective, and we wait to see how it plays out. For the advice industry, provided its traits of competence and authenticity continue to be strong, and as long as it follows what ASIC deems to be positive behaviour, we can reasonably expect people who seek advice to quickly come to trust their adviser and to gain from the clear benefits of advice.

Leave a Comment

You must be logged in to post a comment.