The rapid shift in financial advice from being dominated by the larger institutions to being flush with smaller and mid-size licensees has drastically reduced the amount of capital backing in the industry and placed undue risk at the feet of consumers, according to the head of researcher CoreData.

Andrew Inwood says the retreat of ‘tier one’ licensees like the big four banks and AMP has left a massive hole in industry’s funding and its ability to meet compliance benchmarks, while the lower tiers aren’t being monitored closely enough by the corporate regulator.

“For almost half the industry there is almost no capital keel, the risk sits with the consumer,” Inwood says. “Smaller businesses can’t afford the compliance costs or have that capital buffer if something goes wrong.”

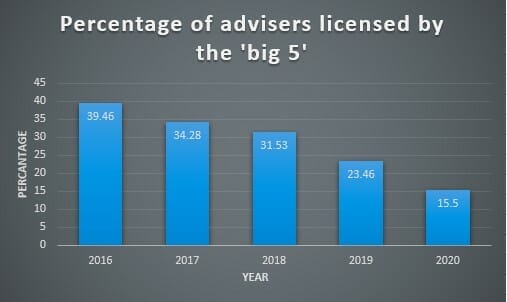

Recent data from the Professional Planner 2020 Licensee Owners List shows the percentage of advisers licensed by the traditional ‘big five’ (CBA, ANZ, Westpac, NAB and AMP) shrinking from around 40 per cent to 15 per cent over the last five years.

Inwood says the advice industry is “completely fractured” now, and is more aptly described as being separated into four industries.

“You’ve got a handful of tier one licensees that have over 500 advisers each, there’s 6928 in that cohort in total. Then you have tier two with between 100 and 499 advisers that have a total of 6023,” he explains. “Next is tier three, which is 10 to 99 reps and has 5600 advisers, and lastly you have the tier four with only 1 to 9 advisers and that entails about 2500 businesses.”

Inwood will speak at the Professional Planner Digital Licensee Summit on Tuesday.

The researcher founder believes the tier one group, which now includes AMP, IOOF, NAB, the NTAA, Easton Investments and Synchron, get all the regulator’s attention. The others on the list are under far less scrutiny, which is dangerous considering the disparity in resources.

“Everybody else is effectively operating in an unobserved environment because the regulator doesn’t have the capacity,” he says. “It’s far from a flat playing field.”

Professional indemnity insurance can’t necessarily be relied upon as a safety net for consumers when things go wrong, according to Inwood. Like any insurance, there is a risk that claims won’t be paid out.

A low capital bar

As it stands, the financial requirements of AFSL holders set out in ASIC’s Regulatory Guide 166 sets a relatively friendly benchmark.

Essentially, entities must have enough money to provide the service and meet cash flow needs, have adequate risk management systems, be solvent and have assets that exceed liabilities.

“The financial resources you have must be enough to cover any risks your business faces that may affect your cash position and that it is reasonable for you to plan to manage,” RG 166 states.

While this is a reasonable baseline, there is no requirement for a significant capital reserve.

Section 912B of the Corporations Act deigns that licensees “must have arrangements” to compensate consumers that suffer as a result of a breach by their representative, but those arrangements aren’t prescribed in the Act.

This could still be of use to consumers in cases where a dispute is taken to AFCA, for example, yet it doesn’t assist if the AFSL holder goes belly-up.

Policymakers acknowledged this issue with the proposal for a Compensation Scheme of Last Resort (CSLR), which is designed to compensate consumers from a pool of funds when a licensed entity has become insolvent.

If the proposal is approved later this year, the CSLR will likely come under the oversight of the Australian Financial Complaints Authority and be funded ex-ante by AFSL holders.

No incentive to grow

Inwood believes that without cash being injected into the industry, there is not much impetus for smaller businesses to grow and build the kind of cash buffers needed to shore up the books in case something goes wrong.

“There’s a bunch of small businesses with one to nine advisers that are really good,” he says. “But they have no scale and satisfaction is gained from running the business rather than growing.”

These businesses generally do well, he says, which actually hampers their chances of growth.

“The thing with smaller advice businesses is that they’re generally doing fine, they’re making money and they’re profitable,” he says. “But in every one of these, fine is the enemy of great. If they don’t have that opportunity to grow then they don’t have the chance to grow their capital.”

Leave a Comment

You must be logged in to post a comment.