This article published in the May print edition of Professional Planner was produced in partnership with Allianz Retire+

The shortcomings of advice for individuals addressing their financial preparedness in retirement is one of the big revelations to come out of the COVID-19 market shocks of recent months.

For those nearing retirement, it’s the realisation that the value of their savings might not be what they expected in the wake of an asset price correction and continued financial market volatility.

For others – those who might not have even thought about their financial preparedness for retirement until now – it’s learning the impact of the removal of a relatively small amount of money, leading to much larger financial ramifications for retirement savings efforts much further down the track.

Since the government announced emergency measures in late March for early access superannuation, the Australian Tax Office has fielded hundreds of thousands of applications, meanwhile many funds have received unprecedented enquiries relating to how they’re navigating through the crisis. Groups such as Super Consumers Australia and The Actuaries’ Institute have since produced guidance on what impact early access to super will have on future retirement savings balances.

Much of the uncertainty relating to individual retirement savings outcomes stem from the industry’s tendency to rely on averages instead of outlining worst case scenarios, according to Jacqui Lennon, Allianz Retire Plus’s head of customer experience and product (pictured).

In particular, averages can fall short when it comes to measuring variable such as life expectancy, vitality of individuals at certain ages, size of retirement balances resulting from income during working years and returns, as well as the coincidence of large market drawdowns happening planned retirement year, Lennon notes.

“At a time when we are having a lot of conversations about policy and statistics and numbers, it’s really important to reflect on the humans at the end of that and to really focus on the people we are trying to solve problems for,” Lennon says, drawing on research relating to biological verses chronological age, health and life expectancy in different countries, high correlations between income and longevity, and probability of significant market events coinciding with segments of the population’s retirement age.

SPEAKING OF AVERAGES

Averages were a hot topic of discussion at Professional Planner and Investment Magazine’s Retirement Conference in late March, particularly among researchers and actuaries including the Grattan Institute’s John Daley and Mercer’s David Knox as part of the ongoing conversation relating to the Super Guarantee and other superannuation policy settings.

Daley builds a case for the government to encourage people to keep more of their working age incomes in the future instead of contributing to super because incomes will likely be lower on average as will economic growth. “History tells us unemployment will be sticky, so unemployment will be high for a long time,” Daley says, suggesting people will be less likely in this environment to contribute to mandatory retirement savings.

Meanwhile, Knox points out that Grattan’s modelling, which averages the level of real income over from age 67 to age 92, undermines the Institute’s assumption that retirement income should increase with price inflation.

The result of its modelling is that the real value of the retiree’s income gradually increases from age 67 to age 92, where the model stops, Knox highlights. Meanwhile he says Grattan is suggesting the age pension will continue to increase with wages, which normally rise faster than prices, Knox says.

“Grattan averages the level of real income over these 25 years and shows that most individuals will receive an average replacement rate of more than 70 per cent during retirement. However, it is well below 70 per cent for most income earners in the early years of retirement and then increases later. Indeed the OECD calculates that the net replacement for an average income earner in the first year of retirement is only 39 per cent,” Knox highlights.

FLAW OF AVERAGES

While averages are commonly drawn on by the superannuation industry to determine policy settings and to identify overall funding adequacies and short falls, Lennon says that doesn’t mean averages should be relied on to advise individuals on their circumstances.

Portfolio returns are an area where advisers have over-relied on averages to help individuals plan for their retirement, Lennon says.

“We need to stop talking about averages and start talking about worst cases, because an average portfolio will have a 50/50 chance of lasting the time it’s supposed to,” she says.

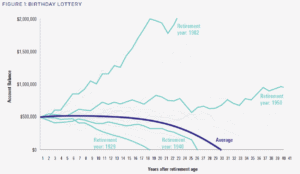

“Depending on when you retire the outcome can be very different… Retirees are desperately worried their portfolios will act like a 1929 or 1950s portfolio, who know what they’re thinking about a 2020 portfolio,” she says.

Indeed, the superannuation industry is generally good at telling people what their retirement will look like on average, but it provides little information around the range of retirement outcomes which may be experienced, says David Bell, former Mine Super chief investment officer and executive director of the Conexus Institute.

Telling people what their retirement will look like on average is part of a deterministic modelling approach, while providing a range of outcomes is known as stochastic modelling, Bell explains.

“Effectively we tell people what to expect but we haven’t coached them for what may occur,” Bell notes.

“We leave consumers unaware and uneducated. This is all fine when markets are performing well, but what happens during the tough times? Most likely, people will experience a worse retirement than the one communicated to them,” he says.

“But it goes further than that: people don’t know the size of the impairment to their retirement plans, and they will likely have reduced confidence in any updated guidance provided to them. Hardly the platform to spend with confidence in retirement,” Bell says.

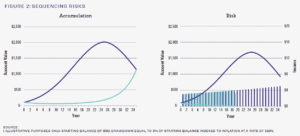

Whether you have the good years or the bad years at the start or the end [of your investing timeframe] doesn’t matter so much in an accumulation portfolio, but it does in a decumulation portfolio,” Lennon notes, pointing out that flipping the order of a market fall and gain can have a significant impact on the retiree’s balance at the end of the day.

Leave a Comment

You must be logged in to post a comment.