Self-funded retirees have missed out on the financial support other sectors have received during the coronavirus crisis and the government should “get creative” in finding a way to help support pensioners, according to the National Seniors Association.

While the government has implemented a range of assistance programs including stimulus payments for aged pensioners and the unemployed, ‘jobkeeper’ subsidies for employees and increased asset write-offs for businesses, Henschke says the fate of self-funded retirees has been ignored.

“Older Australians who are self-funded have a difficult road ahead because of the new and weird world of COVID-19,” says Ian Henschke, chief advocate at the NSA. “There’s talk of bank shares paying minimal dividends, if any, then there’s record low interest rates and the steep fall on returns in super funds.”

He suggests the government could assist self-funded retirees and part pensioners in one of three ways, with the most obvious way being to fix the “broken” taper rate used to determine age pension accessibility.

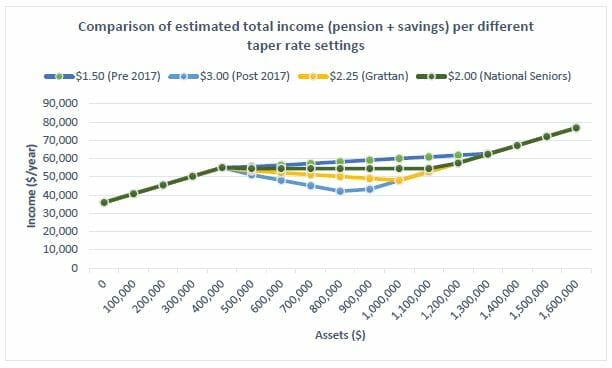

The taper rate has been a particular bone of contention for retirees since it was changed in 2017 from $1.50 to $3.00 for every $1000 of assets over the relevant threshold. The change meant more people got the full pension, but part pensions were reduced more dramatically.

Moreover, modelling showed the taper rate actually reduced total income for retirees with balances between $400,000 and around $800,000, depending on the data and the variables.

The taper rate ‘dip’ is an anomaly financial advisers are acutely aware of, and one actuary Rice Warner described as “punitive” in their recent retirement income review submission.

“The taper rate has distorted the retirement income system,” Henschke says. “It’s created a perverse incentive in the retirement income system whereby the ones that have saved more are actually getting less.”

It’s an issue Henschke says compounds the woes of part pensioners who’ve had the value of their savings slashed during COVID-19. Now is the time to switch the rate back to “$1.50 or $2.00”, he says, and equalise the income disparity for pensioners “stuck in no man’s land”.

Deeper cuts required

Henschke says the NSA has received a flood of correspondence from members asking the representative body to plead their case in Canberra since the crisis started.

“Again, self-funded retirees are ‘dumped’ by the Government,” one pensioner stated.

An alternative measure the NSA advocates is cutting the deeming rate back to the cash rate.

The government reduced the deeming rate – used to calculate the estimated earnings on investments – twice already this month by a total of 75 basis points to a rate of 2.25 per cent. Henschke says it’s still too high with the official cash rate at 0.25 per cent and term deposits rarely reaching 2 per cent.

“People are not getting that kind of return on their investments at the moment,” he says.

The third measure the NSA is advocating for self and partly funded retirees is an amendment to the interest rate on the government’s pension loan scheme, which gives Australian citizens of pension age the ability to borrow against their home.

The rate for the scheme was reduced recently from 5.25 per cent to 4.5 per cent, which Henschke again says is not effective enough to make it palatable for older Australians.

“The government should look at halving the rate and making it less unfair,” he says, noting that the government can hardly ask the banks to follow cuts in the official cash rate for home loans when they’re only taking half-measures themselves. “4.5 per cent is still too high,” he says.

What this will mean for retirees, Henschke explains, is that self-funded retirees can halve their pension drawdown – as per the government’s recent policy change – and supplement their income with loan payments instead of selling assets required to fund a full pension drawdown when market returns are poor.

“Then when they come out the other side they can go back onto their 5 per cent drawdown,” he says.

Leave a Comment

You must be logged in to post a comment.