As an industry we generally tell people what their retirement will look like on average; this is known as deterministic modelling. Typically, we provide little information around the range of retirement outcomes which may be experienced, known as stochastic modelling.

Deterministic modelling is used widely across the superannuation and wealth management industry, through the software that underpins the advice process to the tools attached to platforms and superannuation fund web portals and everything in between. Stochastic modelling is not.

Effectively we tell people what to expect but we haven’t coached them for what may occur. We leave consumers unaware and uneducated. This is all fine when markets are performing well, but what happens during the tough times? Most likely, people will experience a worse retirement than the one communicated to them. But it goes further than that: people don’t know the size of the impairment to their retirement plans, and they will likely have reduced confidence in any updated guidance provided to them. Hardly the platform to spend with confidence in retirement.

It would be understandable if people felt that they have lost control of their retirement. Can anyone blame people for feeling anxious in such a situation? No wonder panic-led decisions are made in areas such as switching.

As an industry we are part of the problem.

Where’s the guidance?

Advice and guidance are both failing when it comes to communicating the range of possible retirement outcomes.

Guidance is the collection of general information and interactive tools provided to consumers. Examples include retirement income estimates provided on annual super statements, and interactive projection tools.

This is a collective industry problem. Even ASIC’s moneysmart retirement planner, which is better than most retirement calculators provided by super funds, provides deterministic guidance.

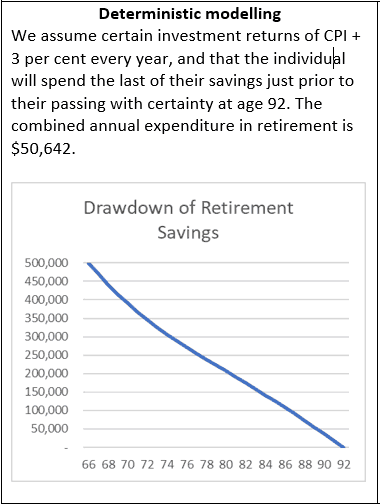

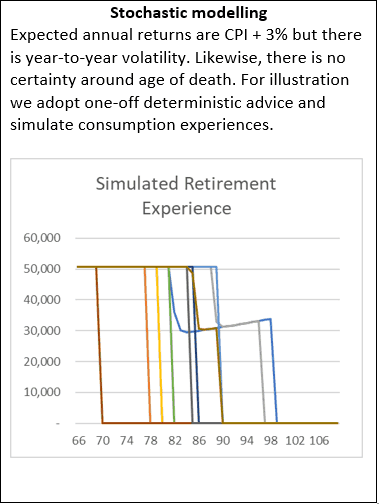

A brief explanation of deterministic & stochastic modelling

Consider a single male homeowner who is about to retire aged 67 with a superannuation balance of $500,000. This example already accounts for the age pension.

The flaws of deterministic guidance have been known for many years. Some firms have been looking to implement better advice and guidance solutions, but it is hard to name with certainty any group which has implemented better practices.

The opportunities are great.

Consider the advice message: “As a household you face an uncertain retirement. We work to assess those sources of variability and account for them in the plan we have designed for you. These are the range of retirement outcomes that we see as possible. Are you comfortable? Let’s consider some of the bad outcomes and work through the impact on you. If necessary we can modify the financial plan.”

So why does the status quo, deterministic advice, persist?

When it comes to retirement we can do so much more for consumers. Why don’t we?

There are many possible reasons but two carry the most weight. One is cost.

Complex models are expensive to develop, particularly in the Australian market where the means-tested age pension adds to modelling complexity. The financial services industry has experienced much structural change over the last decade; perhaps this upgrade to advice modelling has continually been ‘parked’.

The other issue is more concerning. Sometimes I wonder if we, the wealth management and superannuation industry, are complexity-averse. I don’t mean complexity for the sake of it. I mean solving complex problems and then tackling the associated challenge of being able to communicate effectively with consumers.

Does the medical industry not develop new treatments? Are new energy technologies not explored? Does the motor industry not introduce new safety features? Each of those industries embraces the challenge of solving a problem and explaining the benefits in consumer-friendly language.

I hope our industry is one which embraces the complex challenges.

I’m sure some industry participants will raise the regulatory environment as an additional obstacle. I’m sure our regulators are looking to be enablers rather than roadblocks, and that there is an opportunity to consult.

Advice and guidance provided to consumers is one area where I’ll be looking to make a positive impact with The Conexus Institute, leading to better outcomes and less anxiety for Australians.

Leave a Comment

You must be logged in to post a comment.