One of the hardest things for some financial advisers to do, it seems, is to explain simply and clearly to a client, whether existing or prospective, exactly why financial advice is valuable, and what’s in it for the client.

In part, it’s because there are certain things advisers take for granted – like their advice is valuable. But it’s also partly an historical issue stemming from the fact that for many years, advisers didn’t have to articulate much of a value proposition at all, beyond being competent at picking investment products.

It was possible to run a (financially) successful advice business by attracting people with money to invest, selecting a few managed funds, and being paid a commission for the products sold. Life got a little tougher when commissions were banned, so the focus shifted to charging a “fee” based on assets under management (with, in some cases, an associated managed portfolio service), but the basic proposition remained the same.

And that’s in large part where a common perception came from that you have to have money to invest before it’s worth going to see a financial adviser.

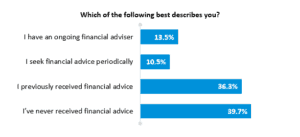

CoreData’s latest trust research shows that around four in 10 people have never had a financial adviser, ever. A broadly similar proportion have previously had an adviser, but don’t anymore. That leaves about a quarter of people with either an ongoing advice relationship or a relationship based on seeking advice periodically. That’s broadly in-line with the received wisdom that between two and three in 10 Australians have an advice relationship.

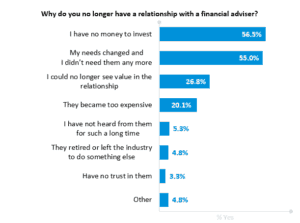

More than half of the people who previously had an adviser but don’t any more say the relationship ended because they had no money to invest, and/or because their needs changed and they no longer needed advice. Again, the perception that the value of an adviser pertains only to the investment is the dominant factor.

About a quarter of people said they’d stopped using an adviser because they no longer perceived value in the relationship, and about one in five said it had become too expensive. Only 3.3 per cent said they’d terminated their relationship because they’d lost trust in the adviser.

These findings underline the need for advisers to transition away from an investment focus, and to break the perception that you have to have money to invest before it’s worth seeking advice. It illustrates why advisers must be able to plainly and clearly explain the value of advice, well beyond an investment proposition. But to do that, advisers themselves must understand the value they offer, and be able to explain it.

When clients do get an adviser’s value proposition, they tend to stick around. Almost half (47.4 per cent) of people who have an ongoing relationship with an adviser have been in it for 10 years or longer. Around one in five have been in the relationship for five to seven years.

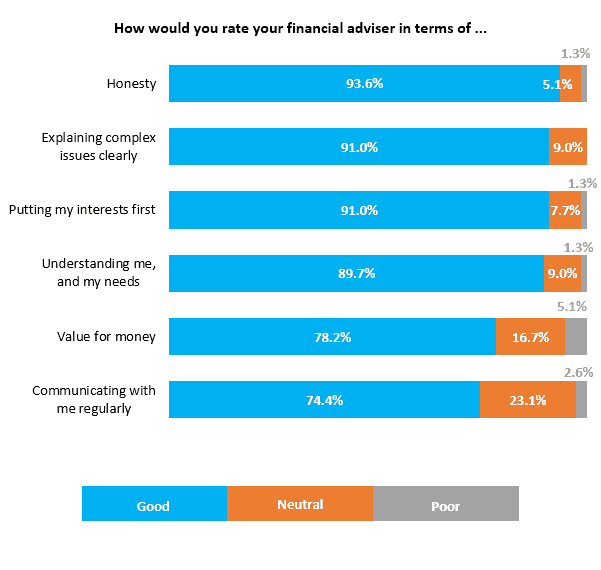

Clients in an ongoing advice relationship rate their advisers very highly on issues of honesty, explaining things clearly, putting the client’s interests first and understanding the client’s needs. They rate their adviser slightly lower – but still pretty highly – on value for money, and for communicating with them regularly.

All of these issues underpin a relationship of trust, reflected in another research finding that around nine out of 10 (89.7 per cent) clients of advisers are extremely likely to recommend their adviser to family or friends.

Once a client has fallen into the embrace of an adviser, they’re clearly pretty happy with what they get, but the fact remains that around three quarters of people have never had an adviser or have had one but stopped seeing them.

The issue, therefore, seems to be not that advisers have trouble retaining clients once a relationship is established but that the industry overall struggles to attract new clients, which may be due to the perception that unless there’s an investment issue to solve, an adviser is of little value. But there may be slightly more to it than that, because the research also shows that if an individual received $1 million on cash today and were to invest it, more would invest directly in property (40.8 per cent) than seek financial advice (33.7 per cent). But in good news, more would seek financial advice than just stick it in the bank (12.4 per cent).

Without wishing to sound like a broken record, the financial advice industry continues to grapple with the issue of being trusted. Our most recent research shows that trust in financial advice rose for the second quarter in a row in Q3 2019. There’s nothing to get carried away with just yet – it’s only two quarters – but at 41.3 per cent it’s at its highest level since the end of Q2 2018, when trust went off a cliff as the royal commission got stuck into the industry and some of its practices.

Trust is a nuanced issue. There are different ways to describe it, we think of it as having four components: Benevolence, competence, control and authenticity.

In a nutshell, you create a relationship of trust if you consistently act in another’s interests; if you’re good at what you do; if you control the things within your power to control and are clear on what things you cannot control; and if you do what you say you’re going to do, at the time you say you’re going to do it.

If you think about the impact of the royal commission, you can see how some of its findings undermined trust in the advice industry, because they pertained to one or more of those underlying factors.

And if you think about an advice proposition based on investing, essentially you’re claiming to be able to control something (investment performance) that is in fact outside your ability to control. Inevitably, when it disappoints the client, it’s too late to say, well, sorry, but that’s not my fault.

But if you develop a relationship with a client by showing you understand their goals and aspirations, map out strategies to help them get to those goals (which may involve an investment solution, but are not predicated on it), and help them stay on-track along the way, then you’re on track yourself to developing trust.

And as a bonus, you’ll have developed a value proposition that gets around the problem of people thinking there’s no point coming to see you because they do not have enough money to invest.

Leave a Comment

You must be logged in to post a comment.