A year to the day since Kenneth Hayne published his first missive outlining recommendations from the Royal Commission and the advice industry has never and will never be the same.

Since that day at the end of September when the interim report was handed down, all four banks have confirmed they’ve walked away from owning advice; the largest wealth manager in the country, AMP, has announced its plans to morph into a “boutique” and billions of dollars has been earmarked to be paid to clients of financial advisers in the form of reparations. There is no sign that the shape of the advice industry will stop moving any time soon.

But how far the parameters defining advice are likely to move still remains uncertain, despite the clarity with which the government has laid out its plans to implement all 76 of Hayne’s recommendations and, in some cases, move beyond Hayne’s brief.

Changes likely to have the largest impact on advisers and their businesses remain untested or at least under researched at this stage, the government’s implementation roadmap and ASIC’s list of priorities in its corporate plan reveal.

In particular, Hayne’s recommendation 2.1 – which specifies that advisers need to tell clients clearly what fees they will pay and what services they will receive in advance, and that fees should be renewed annually and no longer be deducted from client accounts without express written authority – will likely find its way into policy before the consequences of the change are fully understood.

While ongoing service arrangements are still allowed under the Corporations Act (2001), legislative adjustments in this area will be prioritised by government, despite unfinished reviews in this area.

Many industry participants are describing the annual opt-in and fee renewal requirements as one of the most significant changes suggested by Hayne and supported by the government to date.

“It seems inevitable that the annual [renewal] process will result in gaps in this advice relationship, as more clients choose to pay on demand,” says Nathan Jacobsen, managing director at Sydney-headquartered dealer group, Paragem.

Jacobsen adds that while he’s not suggesting the annual opt in isn’t appropriate, he encourages more debate around how to ensure the change is well thought-through and that the “unknown unknowns” don’t create future problems for consumers and advisers.

“If circumstances change during those gaps that invalidates prior advice and detrimentally affects the client, it also seems inevitable that the risk of confusion around accountability will see an uptick in disputes and complaints,” Jacobsen says.

30 YEARS OF CHANGE

The annual opt-in change isn’t the only piece of legislation policy makers will usher in without being fully aware of the consequences and it is unlikely to be the last in this tranche of proposed changes, which Senator Jane Hume, the newly appointed Assistant Minister for Superannuation, Financial Services and Financial Technology, describes as the largest and most comprehensive financial services law reforms the country has seen in more than 30 years.

“Over the next 18 months these reforms will dominate Treasury’s legislative program,” Hume told delegates at the Financial Services Council Annual Summit in Sydney in late August. The work required by Treasury to pass these reforms will represent around three quarters of its current priorities, she added.

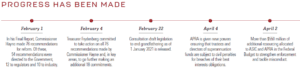

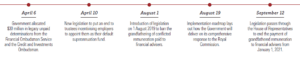

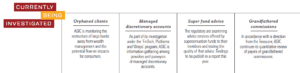

The banning of grandfathered commissions was the first legislative priority to be pursued by the government, even before its successful bid to stay in power after the May Federal Election. Legislation has since been passed ensuring grandfathered commissions will be banned from January 2021.

But while the legislation ensuring commissions enshrined by previous attempts at curtailing conflicts of interest in the industry are banned, it’s apparent that the impact of the removal of these commissions is not been fully considered.

“We had done earlier work, which wasn’t as comprehensive,” Joanna Bird, ASIC’s executive director of wealth management, told a Parliamentary Joint Committee inquiry into ASIC’s oversight in mid-September.

Bird was responding to a line of questioning by Coalition MP Bert van Manen asserting that the regulator wasn’t aware of the impact a commission ban would have on advisers when it made its recommendation to the royal commission that the grandfathering of commissions should cease “as soon as reasonably practicable” back in April last year.

It wasn’t until earlier this year when ASIC was directed by Treasurer Josh Frydenberg to undertake an investigation into the removal of grandfathered commissions did ASIC start taking a more comprehensive look.

According to the regulator’s response to questions from Senator John Williams at a Senate Economics hearing in May 2018, ASIC had not undertaken any assessment of the level of grandfathered commissions across the industry at that time.

ALL ABOUT INTENT

Government has a balancing act on its hands according to Pamela Hanrahan, a professor of commercial law and regulation at UNSW.

On the one hand regulators want an advice industry that’s compliant and professional, but at the same time they don’t want the compliance burden to make businesses too expensive run, thereby taking the service out of the reach of every day Australians.

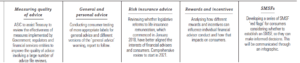

This balancing act is front on mind for both politicians and regulators, evidenced by the work ASIC is doing on client expectations for advice and the ‘orphaned clients’ investigation it is currently conducting following the banks’ departure from owning advice, as revealed in its corporate plan.

Senator Hume has also spoken to this balancing act at the public forums she has addressed in recent months, openly empathising with the demands on advisers’ time given new professional standards legislation and transitioning business models.

“We know it’s important to strike the right balance between the need to improve the professional standards of the advisers operating in the industry, but also recognising that many of these advisers need to balance their work, run their businesses [while managing] studying and their family commitments. The government is listening to those concerns and is carefully considering the right way to proceed,” Hume said in Sydney recently.

Following Hume’s remarks the government announced a one-year extension to the deadline for advisers to complete the FASEA exam, as well as a two-year extension on the deadline to meet FASEA’s qualification requirements.

How well the government manages this balancing act will in large part depend on industry’s approach to lobbying and its ability to adapt to the legislative intent, Hanrahan reckons. She points out that the advice industry has been successful in the past lobbying against reform by citing the interests of an under-advised population and doing so on behalf of thousands of small businesses.

“Industry can look at it in one of two ways,” Hanrahan says. “The first way is as we have traditionally looked at reform which is ‘what’s the minimum damage we can do to the existing business models to accommodate the changes and allow the government to tick a box and say ‘yes we implemented those recommendations’.”

“The other way is actually thinking about what advice should look like in five years from now and work your way back from there. I’m not sure you arrive at the same outcome if you come at it from the two different ways,” she says. Hanrahan’s research was used as background by Hayne during his royal commission recommendation deliberations.

Hume, a former private banking executive and senior policy adviser at AustralianSuper, has called for the industry to start taking control of its own destiny.

“I’ve had a lot of meetings with stakeholders in the superannuation sector in particular since taking up this portfolio… But it really is only now, with the writing on the wall, where it looks like there are the numbers to pass [legislation] that will illuminate unnecessary insurance that a number of industry players are saying ‘we kind of knew something had to be done about this’,” she says. “To which I say, where have you been?”

Leave a Comment

You must be logged in to post a comment.