On January 1 this year, the government turned down the tap on the number of new advisers flowing into the financial advice industry. It didn’t turn off the flow completely, but it ensured that for the foreseeable future new advisers will only trickle in.

Before the end of 2018, though, there was a flood of new names onto the Australian Securities and Investments Commission (ASIC) financial advisers register (FAR). CoreData’s analysis of the FAR shows that more than 5000 new names were added in the December quarter; at the same time around 1000 names came off it, for a net gain of just over 4000 ARs in the three months to December 31.

Not every one of the new names was necessarily a new adviser, however. In some cases licensees who predominantly offer advice only to high-net worth “sophisticated” clients added their advisers to the register, as a defensive measure against them potentially being treated as “new entrants” to the industry at some point in the future.

It’s understandable why they’d want their existing advisers to avoid being classified in future as new entrants. New entrants to the industry after January 1 this year must comply from day-one with the full gamut of new education, professional and ethical standards, administered by the Financial Adviser Standards and Ethics Authority (FASEA). That means unless they hold a FASEA-approved university degree, and approved graduate diploma, or an approved masters degree, they can’t get in. Hence the rush to get names onto the register before the gates closed.

But whatever the mix of new entrants to the FAR, and the reasons for them entering, what we can be fairly sure of is that for the next few years the flow of new entrants to the industry will be diminished significantly, and this creates some interesting challenges for all licensees.

But whatever the mix of new entrants to the FAR, and the reasons for them entering, what we can be fairly sure of is that for the next few years the flow of new entrants to the industry will be diminished significantly, and this creates some interesting challenges for all licensees.

Talk to almost any licensee and they’ll tell you they plan to increase adviser numbers. And most of them will also tell you they’ll only take on advisers who “fit the family picture”. In a market with few barriers – get RG146 compliant and that’s about it – that attitude was fine.

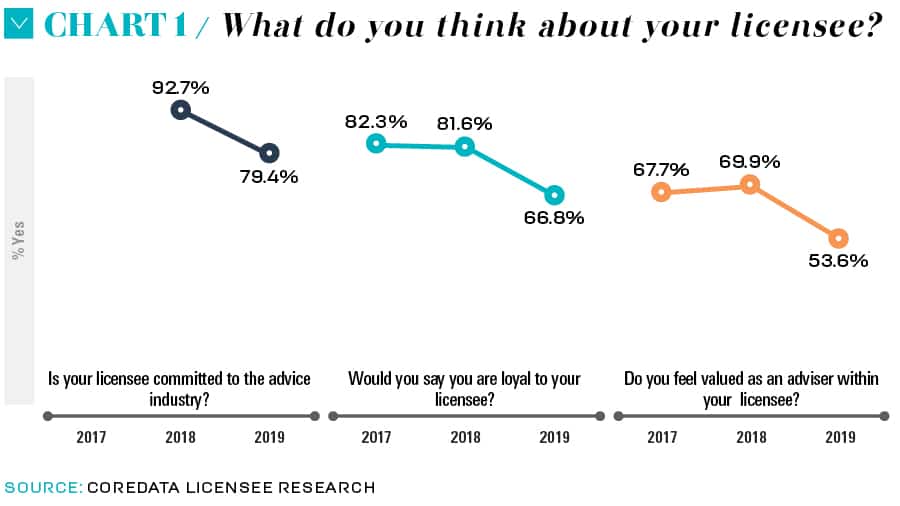

That’s why some of the findings of the 2019 CoreData Licensee Research are so worrying. Across the board, advisers are reporting that they feel abandoned by their licensee, that their licensee is more interested in its internal compliance systems and that executives are looking after themselves first and foremost. Advisers feel significantly less valued within their advice networks than in previous years. They are increasingly questioning their licensee’s commitment to the advice industry, and feeling significantly less loyal to their licensee in return.

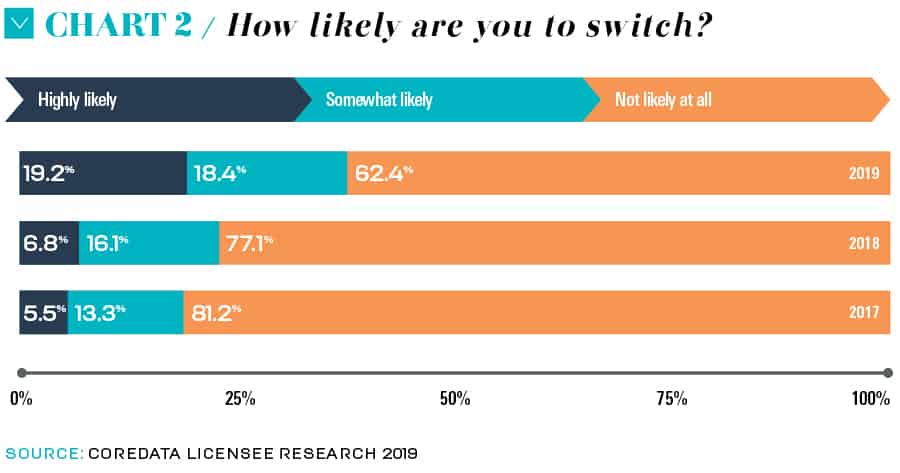

Compared to previous years the number of advisers likely to switch licensees in the next 12 months has almost trebled – one in five say they’re “highly likely” to switch, and another 18 per cent say they are somewhat likely (this is broadly consistent with last year but up slightly on 2017).

Compared to previous years the number of advisers likely to switch licensees in the next 12 months has almost trebled – one in five say they’re “highly likely” to switch, and another 18 per cent say they are somewhat likely (this is broadly consistent with last year but up slightly on 2017).

It’s a portent of pain ahead for those licensees who face the real prospect of advisers breaking camp and striking out for new territory. Good advisers – whose characteristics include clean compliance track records, good, robust businesses and an offer of high-level ongoing service to a loyal client base – will find themselves in the box seat when it comes to licensee options. For the foreseeable period ahead, all licensees will be fishing in the same evaporating pond of advisers. Clearly, not all of them will be able to hit their stated or budgeted growth targets.

We expect the number of advisers in the pond to dwindle for a number of reasons. As conflicted grandfathered remuneration is eliminated (notwithstanding a mooted High Court challenge to the constitutionality of banning it), some advice practices will fail to replace the lost revenue and go out of business. And some advisers will simply opt not to comply with the new FASEA standards, and will leave the industry. There’s also natural attrition, as older advisers reach retirement.

Faced with increasing competition for talent, licensees have some choices to make. They could lower their standards, and essentially take on any adviser who knocks on their door. We’ve seen this particular movie before, though, and we know how it ends. They could compete on cost, offering cheap licensing and practice support services. That’s kind of a sequel to the original movie, and if anything, licensees are generally moving to increase fees, not reduce them, to cover their own costs of service, and risks. Or licensees could simply review growth targets and accept that for the time being, focusing on retaining the good advisers they have may be as valuable a strategy for the long term as attracting new ones.

Leave a Comment

You must be logged in to post a comment.