It’s curious to hear Deborah Ralston describe herself as not politically motivated, considering she’s recently been appointed chair of the SMSF Association at a critical time in the political cycle, when the rules defining the country’s retirement savings system are again being hotly debated.

“I work in evidence-based policy, that’s what I do and what I have done for a long time,” says Ralston, whose time as chair will officially begin at the group’s national conference in Melbourne in late February. A professor with the Department of Banking and Finance at Monash University and a former member of the CIPR (comprehensive income products for retirement) industry advisory group, Ralston prefers to wait to be drawn specifically on her views around politics, rather than allowing herself to meander onto the topic.

“I find it actually quite distressing to see the level of politics on the issue of retirement policy,” she says.

“I make the point repeatedly that we [the SMSF Association] are not political players. We work with both sides of government, we have a strong advocacy arm but we have a responsibility to speak up and draw attention to facts,” she comments.

Deborah Ralston will open the SMSF Association’s National conference in Melbourne on Wednesday where the Labor Party’s position on franking credits will be a hot topic of discussion.

PARTISAN BYPASS

As much as Ralston wants to remain apolitical, she knows her allegiances with government are already stitched into the country’s ideological fabric, especially on the matters she has spent her professional career dissecting.

It was, of course, the Keating Labor government in the early 1990s that came up with the compulsory employer superannuation guarantee (SG) contribution scheme, a radical extension at the time of the Prices and Incomes Accord, struck a decade earlier by the trade unions.

Enthusiasm for the original plan to increase the level of SG contributions, along with the idea of compulsory employee contributions, has waxed and waned over the years, depending on whether a Liberal or Labor leader’s hand has been on the tiller. This to and fro show seems unlikely to abate any time soon.

Liberal Party faithfuls will probably expect their preferred government to implement Productivity Commission recommendations and put on hold any increase to the SG until a further inquiry into the broader system’s flaws is carried out. Labor backers, on the other hand, would want to see Keating’s original timeline for SG increases reinstated.

Meanwhile, the “compare the pair” industry-fund advertising campaign, the product of the backlash from the Howard Liberal government’s Choice of Super policy, continues, it seems, to get more flagrant and direct in its messaging as every year goes by.

It’s obvious to everyone, including Ralston, where self-directed retirees and the advisers and service providers who support the SMSF industry land on the political spectrum. People who have SMSFs tend to be more on the right than those with the stronger union connections, Ralston observes.

“To many SMSFs, super isn’t something that’s compulsory, it’s something they are making a choice to be in; whereas, for many people in institutional funds, super is a payment made for them,” she says. Evidence-based observations start leading Ralston deeper into what begins to resemble partisan territory.

“Freedom of choice and self-reliance in retirement are very much aligned with the right side of the political spectrum,” she explains. “When the Labor Party attacks SMSFs, they know the people they are attacking are not their constituency…It comes back to culture, these people tend to be people who have come out of small business. They’re looking after themselves, they are self-reliant.”

BEYOND KITCHEN TABLES

Based on the numbers, Labor’s focus on its traditional industry-fund base looks justified.

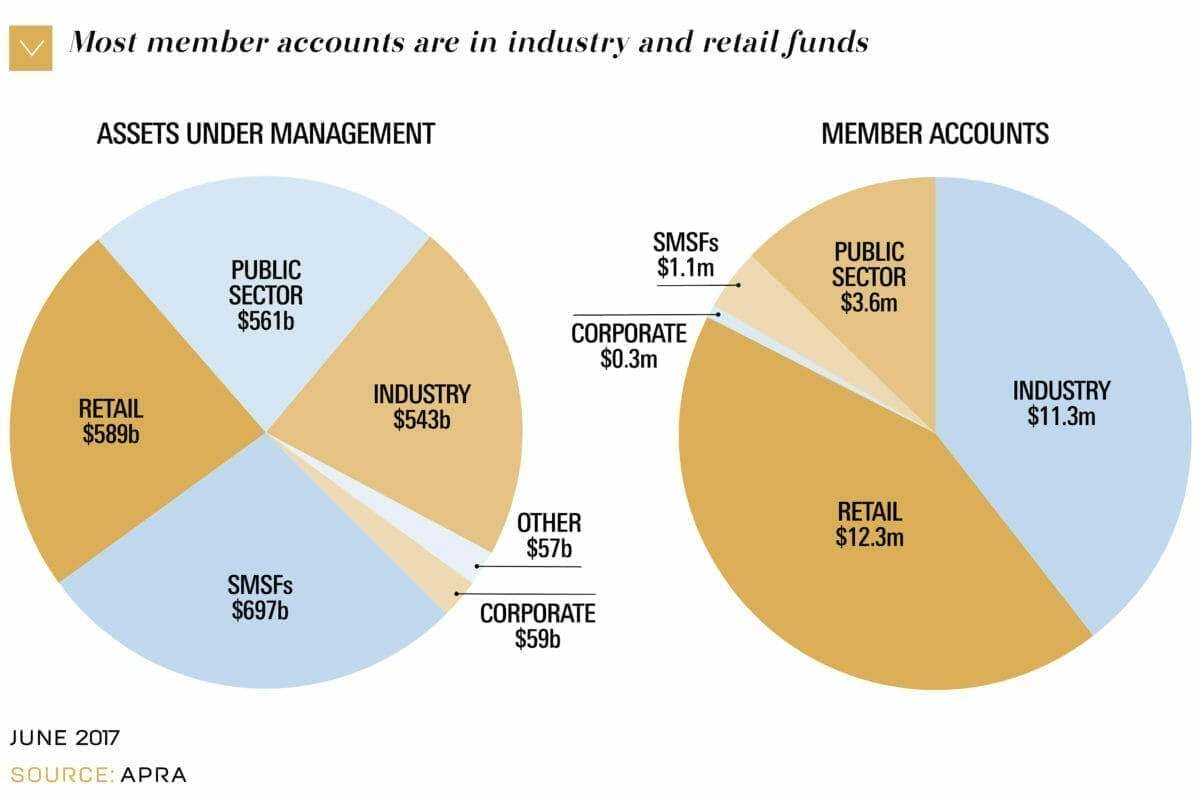

All told, industry funds, public sector and corporate superannuation member accounts total 15.2 million, quite a large number compared with the 1.1 million SMSF accounts in existence. Add this to the 12.3 million retail fund members who should also theoretically be ideologically aligned to a progressive compulsory employer contribution scheme, and the pooled super member cohort accounts for the majority of the voters in the country.

Trying to gauge the influence of the SMSF sector based on the number of accounts is obviously fraught with danger.

Dollar for dollar, the SMSF segment is the largest in the country, accounting for about $700 billion, more than $100 billion larger than the retail, public sector or industry fund segments. With a pool of money this size, SMSFs will have supporters in places well beyond the kitchen tables and suburban accounting offices where many of them are run.

The swift rebuke on the front pages of the daily business newspapers to the Labor Party’s policy to stop SMSFs from receiving tax refunds for franking credits – led by fund managers including Wilson Asset Management chair and CIO Geoff Wilson – is an example of the support for the SMSF segment.

While the growth of the SMSF segment has tapered in recent years, assets in SMSFs have been growing at a compound annual rate of 12 per cent to 2017, averaged out over the last decade, compared with 8 per cent for the APRA-regulated funds, the latest PC report highlights.

CRITICISM HAS SHIFTED

Throughout the meteoric rise of SMSFs – particularly ever since prime minister John Howard and treasurer Peter Costello changed the rules to allow people to contribute up to $1 million in un-deducted contributions for a period – SMSF trustees and the professional services industry that has grown up around SMSFs have had plenty of opportunities to defend against suggestions the structure is a proxy tax haven for the wealthy.

More recently, though, criticism levelled at the segment has begun to relate more to whether members and trustees are, in fact, making the correct and fully informed choice when they sign up to take on the responsibility of managing their own fund.

The suggestion funds are poorly diversified and dangerously leveraged came through strongly last year as lenders started cutting off the segment as part of the clean-up banks have been undertaking on their residential property books.

Pick up Professional Planner’s February print edition to read the rest of this feature article and much more.

Leave a Comment

You must be logged in to post a comment.