For the last seven years, James Dakin, principal of Sydney-based independent financial advice outfit Park Street Group, has signed up all clients to managed discretionary accounts (MDAs). Dakin also wants to transfer long-term clients to MDAs.

But he’s holding off because he’s worried about fallout from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

“We don’t want to tell clients to move to MDAs, only to find out that, with a stroke of the regulatory pen, you can no longer do it,” he says.

Dakin is among many advisers who are increasingly using managed accounts to service clients but are concerned about their future, given regulatory uncertainty. Advisers do need to be bracing for what will come after the royal commission, particularly in terms of managing conflicts of interest.

“Of course, they can keep using them,” the chairman of Sydney-based financial services law specialist The Fold Legal, Claire Wivell Plater, says.

“But they need to be confident that the way they use them is compliant and effectively manages the conflicts.”

If the royal commission banned vertical integration, it would be a severe blow to managed accounts. But that is unlikely to happen and their growth can be expected to continue to surge because they are delivering strong outcomes for advisers and their clients. The royal commission’s final report is due at the end of February next year.

“The nice thing about managed accounts is it’s a solution that benefits everyone,” Investment Trends research director Recep Peker says.

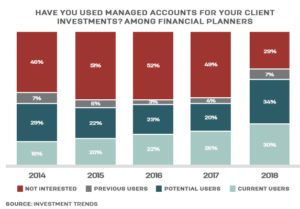

Managed accounts have long promised to be the next big thing. That promise has finally started coming to fruition. Investment Trends data in an MLC white paper released in October states that the proportion of new client inflows via managed accounts was just 4 per cent in 2006. Adoption remained relatively flat, at that level, from 2006 to 2015. “But since 2016, their adoption has surged,” Peker says. At the beginning of 2018, 10 per cent of new business was going to managed accounts.

About 30 per cent of advisers are now recommending the structure, up from 18 per cent in 2014. That growing popularity is also shown by the Institute of Managed Account Professionals (IMAP) and Milliman, which found that at June 30, 2018, funds under management in managed accounts surged 30 per cent over the previous 12 months, to $62.4 billion.

About 30 per cent of advisers are now recommending the structure, up from 18 per cent in 2014. That growing popularity is also shown by the Institute of Managed Account Professionals (IMAP) and Milliman, which found that at June 30, 2018, funds under management in managed accounts surged 30 per cent over the previous 12 months, to $62.4 billion.

A number of factors are driving the greater adoption of managed accounts. Peker says that after the GFC and Future of Financial Advice legislation, many advisers moved into stock picking, in response to client demand for greater transparency and a shift away from managed funds. But they quickly realised that portfolio management and the associated administrative burden were overwhelming and kept them from spending time with clients.

NEXT LEVEL

Mat Walker, head of product for platform business, Praemium, says integrated managed accounts platforms are the next stage of platform evolution beyond wrap account platforms.

“Wraps initially provided investor benefits and adviser efficiencies; however, with the advent of adviser and dealer model portfolio functionality, they ultimately pushed administration and portfolio management work out to advisers, due in part to the need to obtain individual client consent for portfolio changes,” Walker says.

Managed account structures, like separately managed accounts with outsourced professional portfolio management, are more scalable than wraps because they don’t require client consent for changes.

Walker says they also provide investors and their advisers with far greater transparency because, unlike with managed funds on a platform, with a managed account, clients can get a professionally managed portfolio of listed investments, and see all of the underlying holdings in their portfolio 24/7.

Investment Trends’ Peker says another key driver of the growth of managed accounts is they have become more available on platforms. In 2006, just one platform offered them; by 2018, 14 platforms had made managed accounts available, meaning 52 per cent of planners now have access to managed accounts on their preferred platform.

From Dakin’s perspective, the power of managed accounts is they remove the need to have a record of advice or SoA when he makes a change to investments. His firm services 80 families.

“You can’t ring 80 people at the same time. By the time you get to client 75, investment opportunities have usually well and truly past,” Dakin says.

Managed accounts are also helping his firm overcome clients’ behavioural bias towards buying high and selling low.

“It’s often difficult to convince clients to buy after markets have had a big fall because they’re feeling uneasy,” he says. “Under the MDA licence, we can go ahead, as long as we’re operating within the agreed upon mandate.”

But amid this strong growth, the Hayne royal commission has cast doubt on the regulatory future of managed accounts and may be having an impact on adoption and inflows.

While data from IMAP/Milliman shows strong growth in the last 12 months, inflows into managed accounts over the last six months have slowed when investment performance is excluded. FUM in managed accounts rose $5.39 billion in the six months to June 30, 2018. About $2.99 billion was due to inflows of funds, rather than rising investment values, compared with $3.37 billion in the previous six months.

IMAP chair Toby Potter says that while growth is strong overall and the structural shift to managed accounts remains, “the likely impact on advice business models arising from any royal commission recommendations may affect the way in which managed accounts are offered”.

The major concern is that managed accounts will be caught up in a move to ban or restrict vertical integration.

“MDAs by their very nature are a vertically integrated service/product,” The Fold Legal’s Wivell Plater says. “What everyone is worried about is, will vertical integration be banned?”

But Wivell Plater says she is advising clients that the royal commission is unlikely to recommend banning vertical integration. “My view is that the answer will be no, because it would require a structural separation of advice and product, which isn’t really feasible.”

Instead, she argues, the royal commission will “focus on managing the conflicts of interest that arise out of vertically integrated models where advice and investment product are provided within one business”.

One of the most searing moments of the royal commission was the implosion of celebrity adviser Sam Henderson. Along with other issues, the commission highlighted Henderson’s use of MDAs that charged excessive fees.

Wivell Plater acknowledges that there are conflict-of-interest issues around managed accounts.

“Arguably, it is as much in an adviser’s interest as the clients’ to put them into a managed account service, because it’s more efficient for the adviser in running their practice,” she says.

Other potential conflicts arise, Wivell Plater says, because many advisers charge an additional fee for managing the investment, which would otherwise go to a fund manager. And the adviser has a conflict of interest in potentially recommending its own inhouse product or service.

Dakin agrees that 99 per cent of problems are conflict of interest, particularly if advisers have their own managed account service and are using it as a way to take a margin by “clipping the ticket” on the way through. To avoid that, Park Street Group ensures that the fees it charges clients are the same for MDAs. “We don’t make any more or less money if clients choose to participate in or take advantage of our own MDA as a service.”

MANAGING CONFLICTS

Outside the royal commission, moves are afoot to deal with conflicts of interest that Wivell Plater says will go a long way towards dealing with the problem. As a response to the Financial System Inquiry the government has proposed new design and distribution obligations as part of a Treasury Laws Amendment bill.

The laws, which have been released for consultation, would require advisers and product providers to form a view about whom a product is suitable for, and recommend it only to those types of clients. “People will have to be much more rigorous about defining the criteria [for selecting] clients for whom their products (and services) are suitable.” The proposed new laws are awaiting their introduction to Parliament.

Wivell Plater says the royal commission will probably recommend those laws be implemented and encourage ASIC to be more rigorous about policing conflicts of interest.

Advisers who use managed accounts need to be prepared to adjust. The key for advisers is to recommend their managed account service only when it’s in the best interests of the client.

“They need to be much more rigorous in the way they assess that and manage that on an ongoing basis. That’s what will come out of the royal commission,” Wivell Plater says.

That means making it clear to clients if advisers provide only a managed account solution; i.e., if they don’t offer alternative ways of managing the client’s investments.

“They need to make sure the client understands the implications of giving them discretion to manage their investments and are comfortable with it,” Wivell Plater says. Ultimately, the royal commission concerns and conflict-of-interest issues play into the broader debate about whether clients or advisers benefit from managed accounts.

“First and foremost, the client benefits the most,” IMAP’s Potter says. “Clients benefit because they end up with portfolios that are better constructed and generally more appropriate for their specific circumstances and I think, generally, at lower cost.”

Dakin says clients benefit, but he doesn’t hide from the fact his practice also benefits from using managed accounts. “One of the headline things required by ASIC/corporations law – you must run an efficient, honest and fair business,” he says. “It’s not very efficient if you are spending hours and days preparing written recommendations, which most clients who have been with you for a while and trust you are going to say yes to anyway.

“I genuinely think it’s in clients’ interest, and yes it makes our business more efficient, which I also strongly believe is in clients’ interest. Do you want to be advised by someone who is inefficient?”

Wivell Plater and Investment Trends’ Peker agree there are benefits to advisers and clients. Wivell Plater says managed accounts can deliver good client outcomes, which means any regulatory ban would be controversial.

Peker adds: “It’s all centred around making the adviser more effective and efficient, with the added benefits to the client as well.”

Investment Trends data in the MLC white paper states that the average planner saves more than 12.4 hours a week on portfolio management and related tasks as a result of using managed accounts.

“That translates to 60 per cent believing their practice profitability has improved as a result of using managed accounts,” Peker says.

Peker notes his firm’s research has found that what clients like most about managed accounts is transparency, “They can see what’s in a portfolio.”

And three-quarters of planners say their clients’ financial outcomes have improved as a result of managed accounts.

Indeed managed accounts are expected to continue to grow, assuming vertical integration isn’t banned, because they do deliver a better outcome – and not just for the adviser. Investment Trends found that planners expect new client inflows to managed accounts to double to 22 per cent by 2021. In 2018, about 34 per cent of advisers say they are potential users of managed accounts, up 14 percentage points on the prior year.

WHEN UNCERTAINTY CLEARS

Praemium’s Walker says his is still seeing strong growth and expects that to continue. “Our flows into our SMAs under custody and our other non-custodial services are still very strong,” he says. “We see no reason why that won’t continue.”

Walker notes that Morgan Stanley forecast back in 2016 that managed accounts’ FUM would be $60 billion by 2020. IMAP/Milliman data shows that number has been exceeded already: “Managed accounts have been growing at about 30 per cent year on year. We’re expecting that trend to continue strongly over the next few years. That number could be 2-3 times that by 2020.”

The royal commission has obviously brought about some uncertainty for advice groups in terms of how they might need to be structured going forward, Walker says, but he notes many groups were already contemplating this after FoFA, well before the royal commission.

Indeed, Walker says the royal commission could be an opportunity, not a threat, for managed accounts because they complement some of the themes and potential outcomes of the inquiry, including greater transparency of investments, and often lower costs for transacting, administration and investment management and outsourcing of portfolio management.

“That enables advisers to spend far more time engaging with their clients with a focus on quality and the provision of ongoing service that their clients may be paying for,” Walker says. Potter, too, is optimistic. “We’re going to see clarification of the expectations of advice businesses in respect of MAs,” Potter says.

“The key drivers for the adoption of managed accounts – which are better outcomes for clients, better practices for advice businesses and better use of technology – those things are going to be unaffected as a result of the royal commission or ASIC’s views.”

Park Street Group’s Dakin has for the moment stopped moving long-term clients to MDAs but he still plans to use them as long as he can. “We genuinely think it’s in all clients’ interest,” Dakin says. “We expect, over the coming years, to move the majority of clients over to MDAs as long as regulatory requirements don’t make it impractical.”

Leave a Comment

You must be logged in to post a comment.