Being the most stupid person in the room isn’t unusual, it happens often enough to be something that is now unremarkable. But even by historical standards, the issue was taken to new heights (or perhaps depths?) at the Investment Management Research (IMR) Program Conference in Sydney on September 28 and 29.

It seemed like such a good idea: hear some leading academics speaking about the latest research in the field, and listen to them assess the contribution of academic research to the finance industry.

The IMR Program, staged in conjunction with University of Technology Sydney (UTS) and Graham Rich’s PortfolioConstruction Forum, isn’t for the faint-hearted; it’s for the hardcore investment pros and pointy-heads. It underlines – as if we need to be reminded – that the theory informing the practical task of managing other people’s money is complicated. It’s a rich field of research, one in which new and exciting things are being discovered regularly.

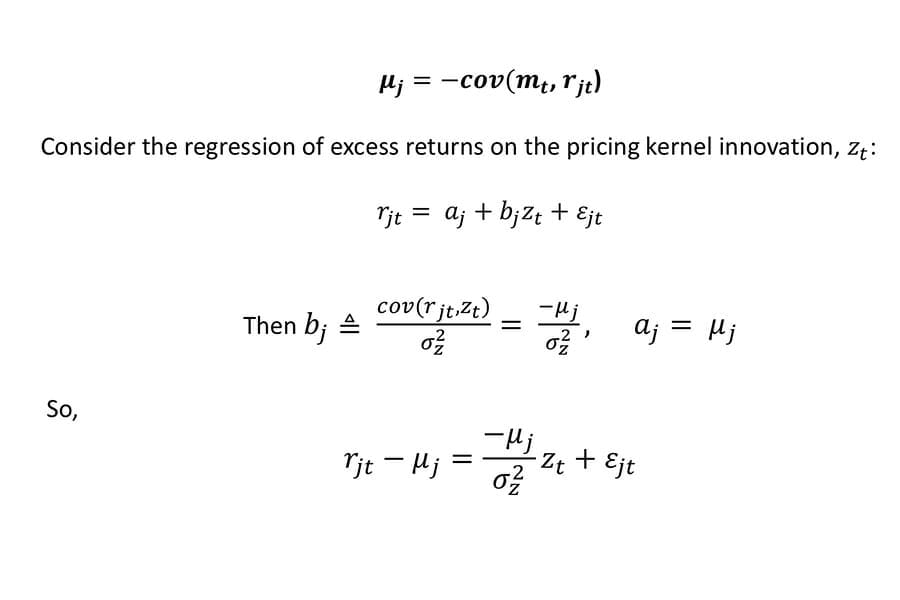

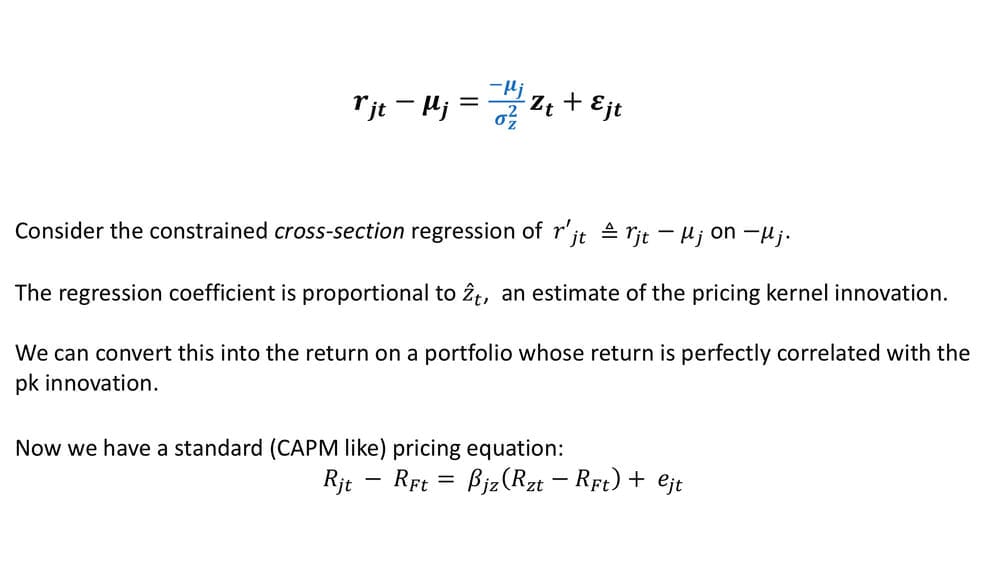

Michael Brennan looks like a harmless enough bloke, but when the professor emeritus at UCLA Anderson School of Business is in full flight, he’s fairly terrifying. He does things like challenge the whole notion of the capital asset pricing model (CAPM). That’s the financial model that describes the relationship between the risk of an asset, such as a share, and the expected return from it.

Mostly CAPM works pretty well, but Brennan has been thinking about alternative pricing models for markets where it doesn’t work as well. Here are a couple of his PowerPoint slides:

These were slides nine and 10 of 42; it was about 10 minutes into his presentation and it had already veered into the incomprehensible. And that’s exactly as it should be. Feeling like the most stupid person in the room is often a good sign that the people you’re listening to are at the top of their game. After all, if pricing assets and combining them efficiently in portfolios were easy, then we’d all be doing it.

And this is something that’s starting to become of greater concern as managed accounts in their various forms and shapes begin to gain real momentum – we are all doing it. Or at least many more are than before.

The Institute of Managed Account Professionals’ (IMAP) latest census of the industry puts the value of assets held in managed accounts at a shade under $50 billion. That’s a lot of money being managed in portfolios constructed by financial planners. And those portfolios might be, well, let’s just say “not built as robustly as they could be”. There’s considerably more to building a portfolio than meets the eye, as a vast body of academic research makes abundantly clear. But that’s all just fancy book learnin’, isn’t it? What’s wrong with picking a few banks, some resources, a couple of retailers? Or knocking together a few ETFs or a collection of top-rated managed funds?

Portfolios advisers produce can, undoubtedly, be well constructed, with smart security selection decisions based on a thorough and well-reasoned process with input provided by qualified investment experts and built with transparency of process and the full accountability of all involved. Some advisers will conduct a full look-through analysis and understand the risks and expected characteristics of the securities they’ve so assembled. Their portfolios aren’t the ones we need to worry about so much.

Of greater concern are the portfolios built in the small, serviced offices across the country by the one- and two-person advice practices with little expert investment input or, potentially worse, with ad-hoc input from whichever fund manager’s business development manager or practice development manager happens to be visiting on the day.

Brennan and his colleagues at the IMR Program Conference didn’t put it in so many words, but their presentations eloquently illustrated why investing is a discipline that requires much expertise and understanding, and a firm grasp of the theory before the practice can be mastered. That’s not to say it can’t be mastered, only that mastering it is a full-time occupation – and that’s fine, if it’s your full-time occupation.

But financial planners aren’t full-time investment professionals, so while the growth of managed account services is impressive and understandable, in a business context, if it means the job of investing is being taken out of the hands of the experts, it could be only a matter of time before it ends in a large shower of sparks and recriminations.

Leave a Comment

You must be logged in to post a comment.