The theme of the recent PortfolioConstruction Forum Strategies Conference in Sydney was ‘It all adds up’. The premise was that client outcomes could be improved through potentially small but incremental insights. Investors often focus on specific, bottom-up ways to achieve this value-add, such as picking the right stocks, exchange-traded funds, managed funds, etc. However, what’s often forgotten in this quest for returns is that individual investments are only part of the picture. How they are combined and interact, i.e. portfolio construction, can affect client outcomes.

Taking a holistic and multi-dimensional approach to portfolio construction can increase an investor’s chance of meeting a client’s long-term performance objectives.

At this point, you may be thinking that I’m referencing the often-espoused adage that more than 90% of the variability of portfolio returns are determined by asset allocation. This statement is based on a seminal 1986 paper by Gary Brinson, Randolph Hood, and Gilbert Beebower titled “Determinants of Portfolio Performance”, which sought to explain the effects of asset allocation policy on US pension plan returns. However, it’s important to stress that the authors were referring to the volatility of returns and not the actual quantum of returns. Nevertheless, intuitively, if you have a portfolio of just long-only equities, then the largest determinant of performance is likely to be how broad equity markets perform. Before launching into any more technical aspects, the easiest way to improve the chances of better portfolio outcomes is to diversify not only across asset classes but within asset classes and across strategies.

The idea that diversification is the only free lunch in investing was popularised by the Nobel prize-winning economist Harry Markowitz in the 1950s, so has been well broadcast by investment professionals for a long time. However, in the Markowitz framework, it’s a means to reduce overall portfolio risk (as measured by volatility). While we will address this below, diversification also means that you’re not overly reliant on a single or a few outcomes to drive portfolio returns. While everyone enjoys opining on and forecasting the future, the reality is that events are unpredictable. You only need to think back to the decision by the UK to exit the European Union in June 2016 or Trump’s victory in the US elections in November 2016; and the markets’ initial and subsequent reactions to these events to realise this. This isn’t to suggest that it’s all too difficult and you shouldn’t have a view but rather be cognisant that there are a range of possible outcomes and that you should incorporate multiple ways of winning in portfolio.

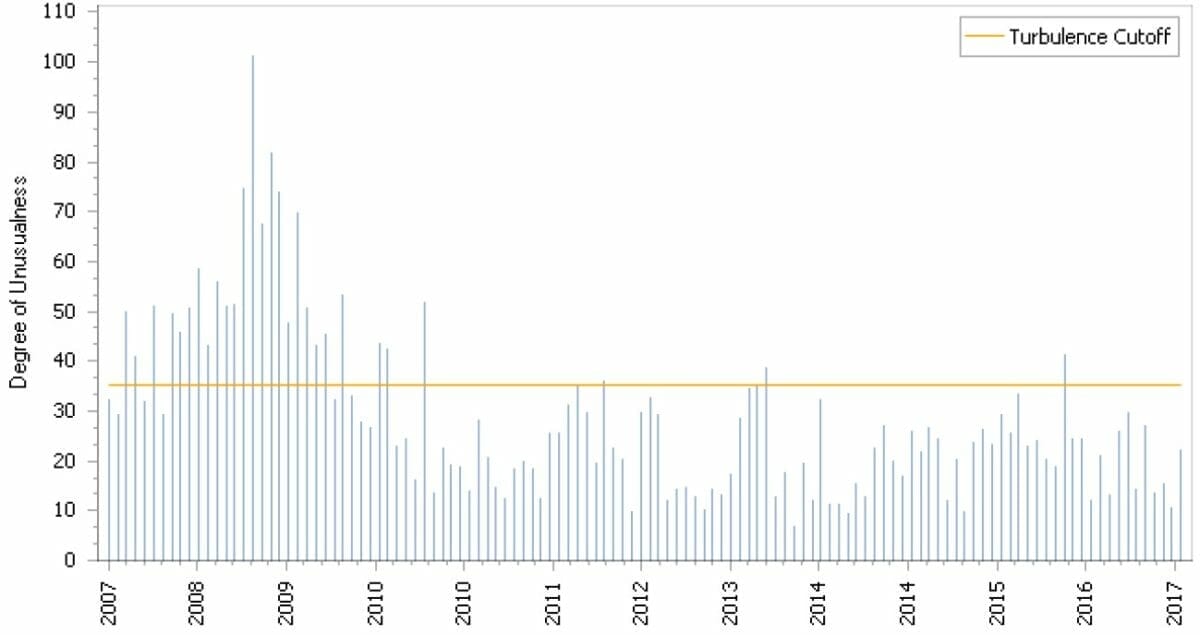

Now, to address the more quantitative component of portfolio construction and why making sure you’re appropriately diversified is important. Obviously here we’re referring to the benefits of correlation, or hopefully lack of, between assets i.e. asset classes perform differently. This means that a mix of assets that don’t have perfectly related (i.e. less than 1 to -1) performance will have lower overall volatility than a single asset. The obvious retort here is that correlations aren’t constant and generally increase in times of stress. However, while this is true, assuming you have the appropriate tools or aptitude, you can stress diversified portfolios during more extreme historical periods to see how they would have behaved in these scenarios. Chart 1, below, is an extract from Windham Labs optimiser, which breaks periods into turbulent and quiet periods and then allows users to optimise portfolios under conditions of these different environments.

Even without these tools, intuitively, there are asset classes or strategies that you can have a fair degree of confidence will perform in an equity sell-offs. A potential asset class example is fixed income, specifically government bonds. Now, to be sure, the scope for these to perform well is less than historically, given starting yields, but bonds remain the “go to” safe assets and there is still some scope for rates to fall, albeit limited. Another specific example in the Alternatives asset class is managed futures, which are trend-following strategies at their most basic form, and consequently only require a sustained directional trend to perform, irrespective of directionality.

Another way of looking at portfolios that has been gaining more interest in recent times has been factor exposures. At their simplest form, factors are variables that can help explain investment returns and risk. While factors can be applied across whole portfolios, we will restrict the discussion to equities. It’s important to stress that factor-based investing is not new, Dimensional is an example of a well-established factor investor. It is simply a different perspective of looking at return drivers that, in many cases, have been well-known for decades.

In general, portfolio (or fund) performance can be decomposed into market-related (Beta), factors and alpha (idiosyncratic skill), as per the following formula:

Market (β) + Factors + Alpha (idiosyncratic skill) = Portfolio Returns

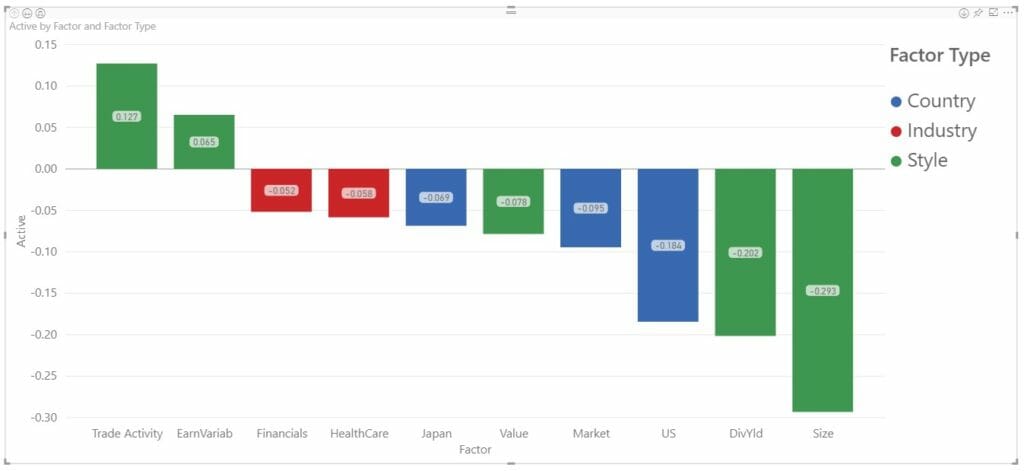

These days, there are a plethora of factors, which can be decomposed into broad or very granular factors. If we restrict the discussion to a very high level, the factors that can help explain portfolios are style (e.g. value and growth), industry and country (for global equities). Chart 2, below, is an extract from Bloomberg Port that decomposes an international equities portfolio into granular factors that fall under these three categories.

Without going into intricate details, this chart measures the sensitivity of the portfolio to the factors. Under the “Style” category, the biggest tilts that can be observed are to small caps (negative size) and not surprisingly, as a consequence, away from dividend yield. Another apparent style tilt is away from value.

Other than helping to potentially explain performance, how can this analysis help construct better portfolios? It’s well established that there are certain factors that are compensated above market returns over the longer-term, e.g. size and value. Consequently, you can construct a portfolio that’s deliberately tilted to these factors to capture these long-term return premiums. Conversely, when constructing a portfolio of active funds, the analysis can help to ensure you’re not overexposed to non-compensated factors or diversifying away compensated factor bets.

There’s a caveat to the above analysis – it’s based on individual stock holdings. As the macro-environment can affect the output, the analysis needs to be run on a regular and ongoing basis to ensure consistency. Additionally, returns-based analysis can be used to corroborate the output.

Much of the above material re-iterates and expands on well-known investment principals with the addition of the more contemporary factor analysis. However, in the rush to add value to client portfolios, it’s easy to forget the first steps to ensuring successful outcomes starts at the top, through robust portfolio construction. To build such portfolios, investors should use a multi-dimensional approach, in recognition that the future is uncertain and no single approach or strategy can take into account the myriad possibilities.

Leave a Comment

You must be logged in to post a comment.