It’s been a challenging time for investment markets since the third quarter of 2015. This period marked the point where investors became increasingly worried about the start and trajectory of US rate hikes, the deceleration in Chinese growth as well as the potentially related collapse of commodity prices. Despite relief rallies in the past few months, most risk assets (equities, credit, commodities) are at levels well below their 2015 peaks and volatility remains above levels that investors have become accustomed to.

Amid the market gyrations, it’s important that investors not become distracted by market noise and remain focused on fundamentals and remember they should be investing for the long term.

As Warren Buffett’s mentor, Benjamin Graham, is famously quoted as saying: “In the short run, the market is a voting machine but in the long run, it is a weighing machine”. In other words, sentiment may rule in the short term but fundamentals come through in the long term.

To this point, volatility can present opportunities for those investors with the tolerance to withstand short-term noise.

Markets can become dislocated

While markets present selective opportunities through the cycle, in times of stress entire markets can become dislocated and fundamentally mispriced.

There are no doubt a multitude of such opportunities in current markets. Zenith believes that one such example may be the high-yield fixed income market. For those less familiar with this market, high yield is a generic term used to define bonds that are rated below a specific level by the major credit ratings agencies, such as Standard and Poor’s (S&P) and Moody’s. A bond assigned a rating of below “BBB” by S&P and “Baa” by Moody’s is deemed to be below investment grade, and as such is classified as high yield.

The high-yield market came to prominence in the 1980s, in a large part through the efforts of famed investment bank Drexel Burnham Lambert and its star trader, Michael Milken. After this period and the collapse of Drexel Burnham Lambert in 1990, the market became tarnished with the moniker of “junk bonds”. However, since this time the market has matured considerably and since the global financial crisis, the size of the high-yield market has grown as companies have sought to take advantage of the low interest rate cycle and favourable borrowing conditions. For example, in the US, the high-yield market has grown from $944 billion in 2009 to $1.8 trillion as at June 30, 2015. If we include high-yield floating rate loans, the high-yield market accounts for over 30 per cent of all US corporate debt issued. Thus, in relative terms, the market continues to grow in size and prominence.

The key attraction

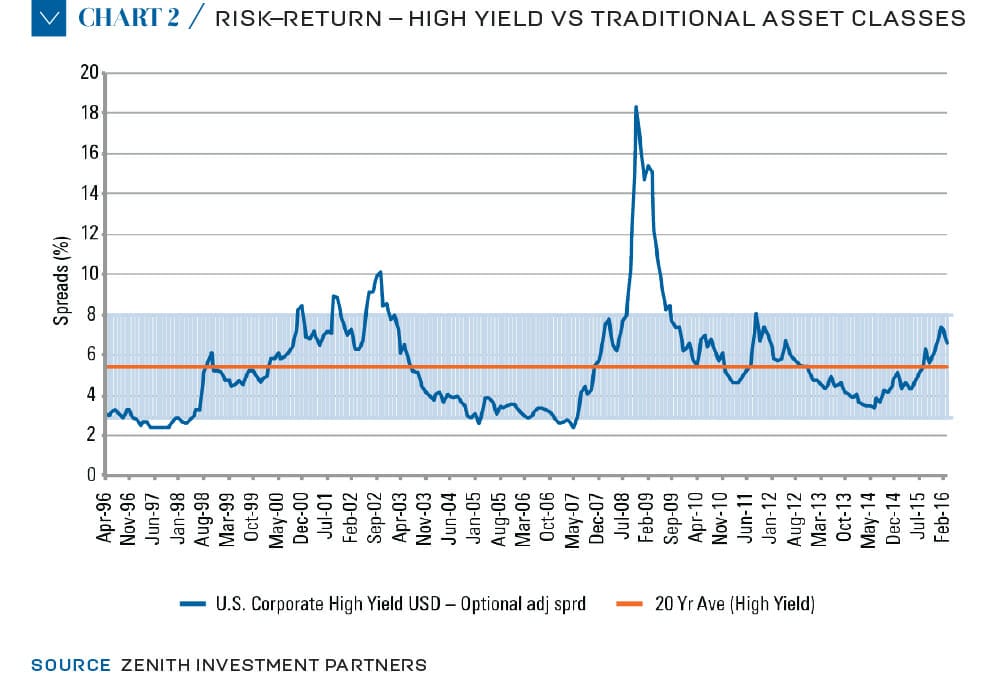

The key attraction to investing in high yield is the additional yield that can be achieved, relative to securities rated investment grade and above. The yield pick-up (spread) varies depending on the environment for credit and the market’s perception of the default cycle; however, generally speaking it has averaged between 150 basis points and 300 basis points over time. Chart 1 compares the spread of US high-yield bonds over US treasuries for the period Jan 1, 2000 to March 31, 2015.

As can be observed, the market started to experience stress in late 2014, as the oil price started to falter. This put pressure on oil-related issuers, who form a significant portion of the common high-yield indices. After a brief recovery in early 2015, collapsing oil prices, renewed concerns over global growth and outflows caused spreads to widen considerably across the high-yield landscape, not just in the energy sector. While spreads peaked at 7.34 per cent on

January 31, 2016, as at March 31, 2016 the market was trading at a spread of 6.56 per cent above treasuries.

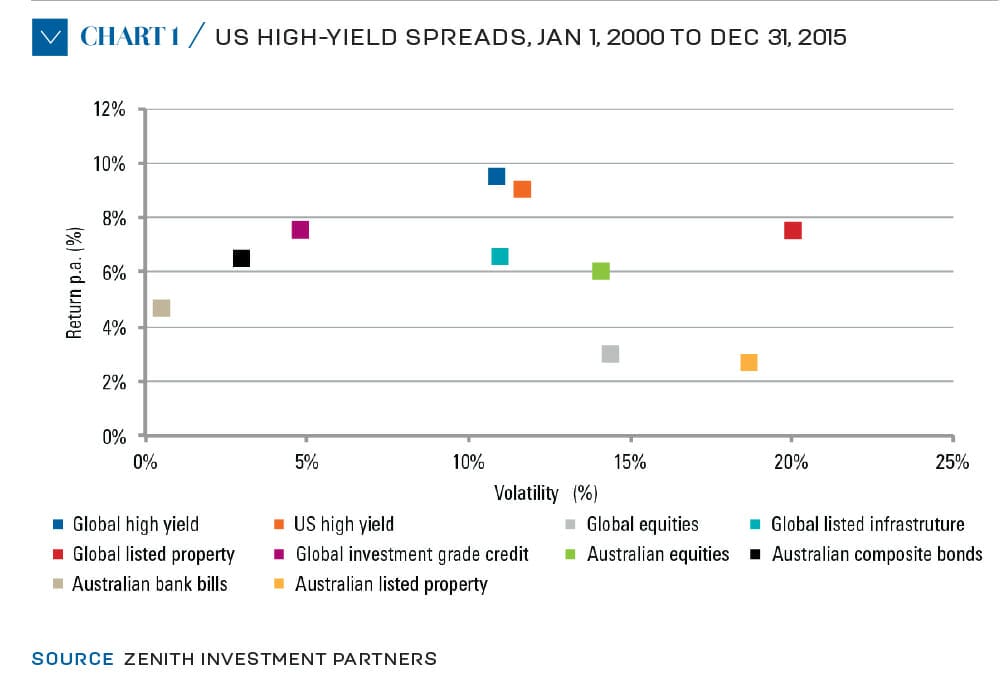

Historically, the global high-yield market has returned 10 per cent per annum with volatility of 11 per cent per annum in Australian dollar terms over the January 1, 2000 to December 31, 2015 period. This compares favourably to other asset classes (see chart 2).

Given current spreads are higher than the historical average, this should bode well for future returns. This holds true as long as one believes that investors are being adequately compensated for defaults. According to Deutsche Bank’s annual study of defaults, high-yield default rates have

been below the long-term average for 12 of the past 13 years. Between 1983 and 2002 the average default rate was 6.9 per cent and since then has averaged 1.5 per cent a year. Although the market expects defaults to increase in 2016, they aren’t anticipated to rise much above 3 per cent.

How to enact this view

So, if an investor makes the assessment that the high-yield market is attractive at its current level, how could they enact this view? There are two main access points to the high-yield sector: investing via an actively managed, diversified or unconstrained fixed-interest fund that maintains a core and/or tactical allocation to high yield, or via a specialist, standalone high-yield fund. Examples of these more dedicated funds are:

• AllianceBernstein Global High Income Fund

• Bentham Wholesale Syndicated Loan Fund

• Invesco Wholesale Senior Secured Income Fund.

Zenith notes that investors can also access the sector through passive investment vehicles, such as exchange-traded funds. However, Zenith believes consistent excess returns can be generated from active management in the sector.

It’s important to recognise that the above discussion only makes an assessment of the high-yield market relative to its history and doesn’t take into account the implications for portfolios of including of high yield in an investor’s asset mix. Furthermore, this is only intended to be an example of a potential opportunity in the current volatile market environment. The key point of the above is to remind investors that volatility can often present wholesale opportunities if they look through the short-term noise and remain focused on the longer term.