The economics of traditional financial advice models are becoming increasingly unsustainable, according to new analysis from consulting firm A.T. Kearney.

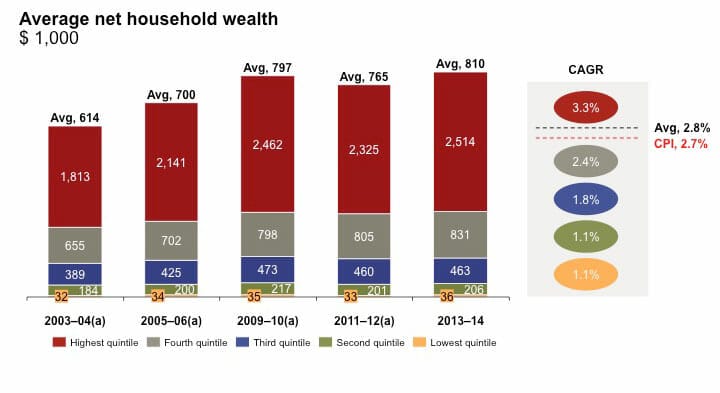

The research combines in-house and Australian Bureau of Statistics data, and indicates only 20 per cent of households are wealthier now than a decade ago (figure 1).

It also shows that only clients in this top quintile have substantial liquidity, in the form of superannuation or other assets, with wealth equalling property for around 80 per cent of Australians.

This highlights the need for cost-effective advice solutions – such as robo advice – which are appropriate for clients in lower and mid-tier income brackets.

“Financial planners would be the real beneficiaries of robo advice, because it allows them to extend their reach into customers they don’t traditionally touch – at a much lower cost fashion.

“So financial planners can complement themselves, clearly, down at that end in a much lower cost fashion,” says Peter Munro, partner, A.T. Kearney Australia.

This is a message the firm has been emphasising in its discussions with Australia’s banks and financial services institutions, which have their own aligned planner networks.

“How can you help your aligned team move up [into robo advice] and what can you offer them to take the costs out of that?

“Mostly, they agree with the direction, then it comes down to how aggressively you want to pursue it, how much investment you want to make to really facilitate it versus waiting for the planners to demand it.

“I think most of the institutions tend to [have a] sort of push–pull with their planner groups. They’ve got to push them on some topics, and they’ve got to wait for them to ask for services and support on others, so they don’t invest ahead of really needing to,” Munro says.

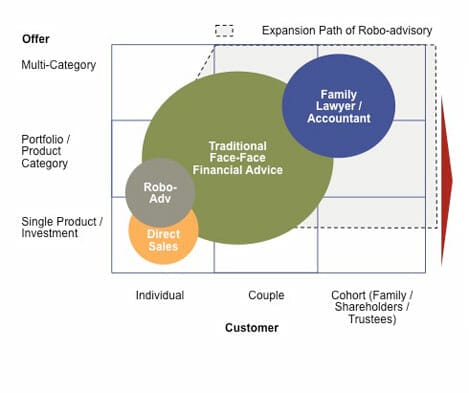

“If you then think about the kinds of advice – am I advising an individual, a couple or a family or trustee group et cetera … the advice gets more complicated as they go from a person to many people.”

Another level of complexity is added in determining what type of product they are advising on, such as equities or fixed interest, a portfolio, or multiple portfolios combining property, shares or other international exposures.

“Where is robo currently positioned? It’s largely in the product category and at the individual person, and so that’s quite cheap,” Munro says.

Leave a Comment

You must be logged in to post a comment.